Global| May 07 2018

Global| May 07 2018German Orders Contract Again on Foreign Order Weakness

Summary

Germany's inflation adjusted orders jumped in December of last year but they were not off to the races. That gain fully unwound and then some the very next month with further declines logged in February and March. The third straight [...]

Germany's inflation adjusted orders jumped in December of last year but they were not off to the races. That gain fully unwound and then some the very next month with further declines logged in February and March. The third straight drop in German orders was not expected for March but that what was posted today as German real orders fell by 0.9%.

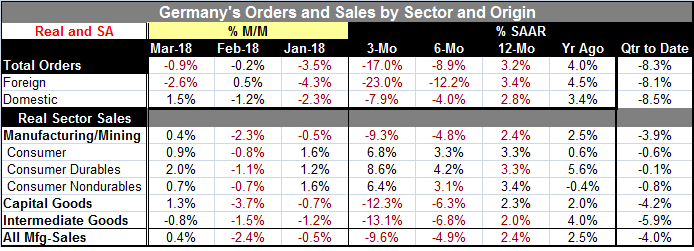

The chart on the left shows a clear drop off in real foreign and domestic orders as 2018 begins. The table memorializes the growth rates. For both foreign and domestic orders, the sequential rates of growth from 12-month to six-months to three-month are showing progressively more weakness.

The chart on the right plots the German manufacturing PMI against the German manufacturing industrial production. Both series, after accelerating from end-2016, are now engaged in a relatively sharp pullback. Globally, the manufacturing PMIs have been pulling back and the service sector PMIs have showed more weakness.

German real sales trends showed gains in March with manufacturing sales up by 0.4%. But sequential manufacturing sales are also showing progressive weakness on the same time as used above as growth rates for real sales rise by 2.4% over 12 months then slow and drop at a -4.9% pace over six months and log a decline at a 9.6% annual rate over three months. Mining and manufacturing combined run very similar trends.

By sector, real sales are doing well for consumer goods with both consumer goods categories, durables and nondurables, show sales accelerating over the 12-month to three-month span. The weakness in capital goods and intermediate goods is a marked contrast. Those two sectors with growth of real sales in the 2% to 2.5% range over 12 months both show significant declines in real sales over six months where growth rates are negative and morph into double-digit annual rate declines over three months.

It is encouraging, if somewhat baffling, to see gains in consumer goods real sector sales especially because other metrics from Germany and the EMU area have shown retail sales to be uneven and weakening. The consumer is the ultimate driver of all growth. Germany is an economy very much plugged into the global trading matrix. Many of its sales are still within Europe and come under the rubric of the single currency. German exports are nonetheless some 50% of German GDP; thus, making it clear that foreign demand has a great deal to do with German sales and output trends.

From a business cycle point of view, it is time for firms to invest as capital expansion should be planning ahead with growth in gear and the unemployment rate so low. But it is unclear whether businesses have the optimism to continue investing. There is still a great deal of 'foreign' competition and there may be questions about the available supply of labor as well. The weakness in capital goods at this juncture is a bit of a surprise, just as the strength reported in German real sector consumer goods sales is a surprise given consumer spending trends in Germany and in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief