Global| Oct 06 2020

Global| Oct 06 2020German Orders Continue to Surge...Still They Lag Below February Level

Summary

German orders are up strongly for four months in a row. Orders surged in May as they broke out from their April pit in the wake of lifted restrictions on the economy. Then orders spurted in June as the get-back-to-work phase deepened. [...]

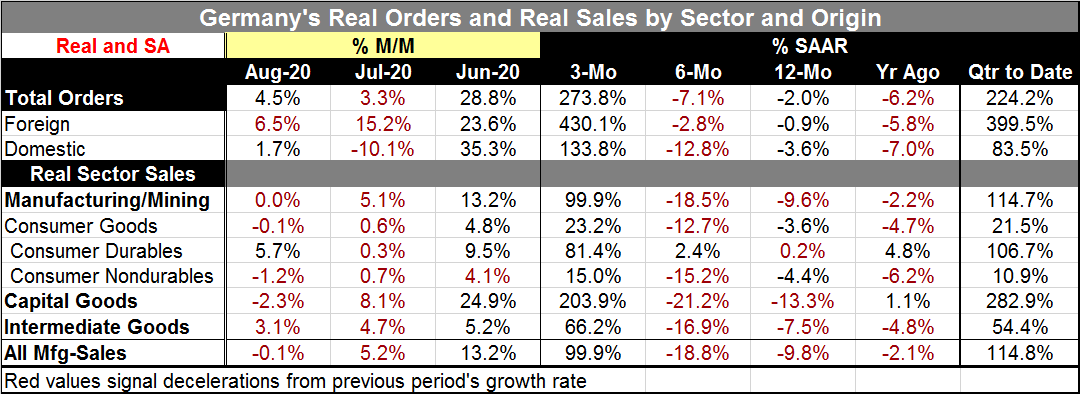

German orders are up strongly for four months in a row. Orders surged in May as they broke out from their April pit in the wake of lifted restrictions on the economy. Then orders spurted in June as the get-back-to-work phase deepened. Orders rose by 3.3% in July and now by 4.5% in August. And yet with all this surging and spiking and growing, orders are still 3.6% below their level of February of this year just before the virus struck. Foreign orders are 1.4% below their February level while domestic orders in Germany are 6.6% below their February level.

German orders are up strongly for four months in a row. Orders surged in May as they broke out from their April pit in the wake of lifted restrictions on the economy. Then orders spurted in June as the get-back-to-work phase deepened. Orders rose by 3.3% in July and now by 4.5% in August. And yet with all this surging and spiking and growing, orders are still 3.6% below their level of February of this year just before the virus struck. Foreign orders are 1.4% below their February level while domestic orders in Germany are 6.6% below their February level.

A familiar story from order growth

Sequential growth rates tell a familiar story. Over 12 months orders fall by 2%. Over six months they drop at a 7.1% annual rate. Over three months orders are jumping wildly at a 273.8% annualized rate. Foreign and domestic orders echo these patterns with different rates of growth, of course.

QTD growth rates are stupendous

Two months into Q3, the quarter-to-date growth rates show a 224.2% annualized growth in overall orders lead with a nearly 400% rate splurge in foreign orders and an 83.5% pace in domestic orders. The growth rate and growth patterns are still too erratic to try to extract a real trend, but recovery is still afoot.

Sales by sector are recovering

Real sales by sector are bit more grounded as they require actual production and physical shipping not just orders on paper. Even so, they manage some strong growth rates especially over three months. Total manufacturing and mining sales fall by 9.6% over 12 months and fall again at an 18.5% annual rate over six months. Over three months sales surged at a 100% annual rate. In the quarter-to-date, sales are advancing at a 114.7% annual rate. And despite all this growth, sales are still nearly 10% below their February level. Among the sectors only durable consumer goods have real sales above their February level (1.2% higher). Sales of capital goods lag their February level the most (by 11.2%). But then capital goods are posting the strongest growth rate over three months at 204%, annualized.

...but sales by sector are slowing too

However, sector sales are decelerating broadly across all sectors over the last two months. The only exception is a pick-up in the sales of consumer durables in August. So despite all the growing and surging and advancing and the support of very strong orders in the background, real sector sales are not building momentum. Sales overall were flat in August and falling in two of the three major sectors (consumer goods, capital goods and intermediate goods) as well as declining slightly in manufacturing overall.

And the outlook is guarded

Of course, no discussion of momentum or trend or the future is complete these days without a mention of the virus. And there the news is bad and there is some further spreading and countermeasures taken to slow the spread that also impedes growth. As of October 5, German infections were still rising and up to 3,100 per day. This compares to a low of 16 back in June. German infections are still not all that high by the standards of other countries, but they are rising and they are at about 45% of their past peak in late-March. It would appear that Germany will be fighting this ‘rear guard’ action against rising infections for a while longer--and that damps the outlook despite a strong trend in orders and in the presence of a weakening trend in sales.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief