Global| Dec 04 2020

Global| Dec 04 2020German Orders Continue Their Hot Streak

Summary

German orders (presented in real terms) have risen month-to-month for six months in a row and now for the first time in that stretch orders also are higher on balance over 12 months. Orders were last higher over 12 months back in [...]

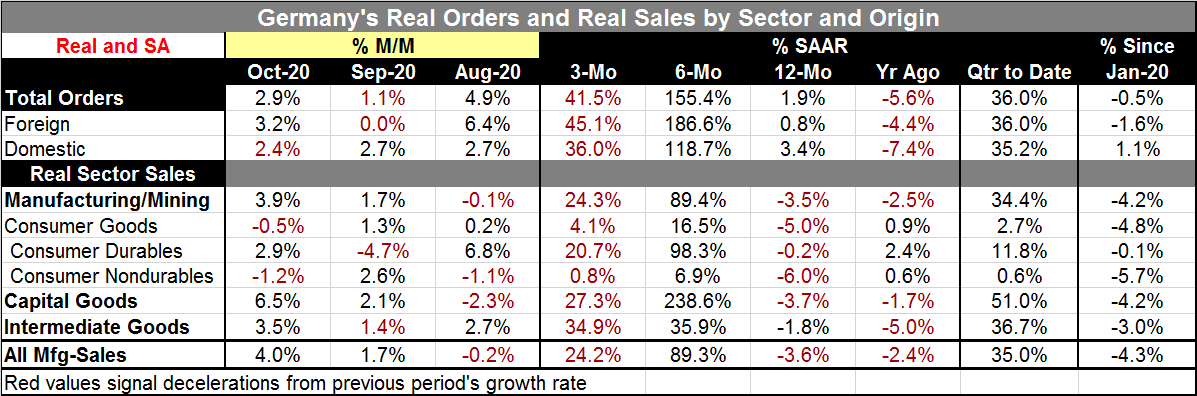

German orders (presented in real terms) have risen month-to-month for six months in a row and now for the first time in that stretch orders also are higher on balance over 12 months. Orders were last higher over 12 months back in February, but that gain was isolated and aberrant. Year-on-year order gains have not been a consistent reality for Germany since March 2018 and earlier.

German orders (presented in real terms) have risen month-to-month for six months in a row and now for the first time in that stretch orders also are higher on balance over 12 months. Orders were last higher over 12 months back in February, but that gain was isolated and aberrant. Year-on-year order gains have not been a consistent reality for Germany since March 2018 and earlier.

As of October, real orders are higher over 12 months for total orders, domestic orders, and foreign orders. On the horizons in the table, the largest gains for all three series are over six months, but the annualized gains over three months are also impressive. Still, over three months total orders are up at a 41.5% annualized rate, strong but they do not rival the 155.4% annualized gain over six months.

Quarter-to-date gains are on the order of a 35% annual rate gain or so for both domestic and foreign orders – those are strong results.

However, compared to January, just before the virus hit Europe, Germany total orders are lower by 0.5%, foreign orders are lower by 1.6%, and domestic orders are higher by 1.1%.

Sector sales are up for capital goods and intermediate goods but show a decline for consumers on the back of weakness in nondurables purchases.

Real manufacturing sector sales have a gain of 35% in the quarter-to-date, essentially the same as for orders. But compared to January, manufacturing sales are lower by 4.3%, a bit weaker than for overall orders. Sequentially the six-month growth rate is at a nearly 90% annual rate, strong, but substantially less than order growth over six months. And over three months, the rate of sector sales, while also strong at a 24.2% annual rate, is nearly half the growth rate of orders.

On balance, the German manufacturing sector shows strong signs of turning around and the growth on year-to-date basis suggests that the phase of impairment may be over for German manufacturing. Most impressive is the way sales and orders have fared through October although we know that November will bring a sterner test as various restrictions slowed much of Europe as well as the German economy itself. While a second wave of infection might take manufacturing down, it still looks to have recovered pretty fully from its outsized first wave setback. The November PMIs point to more weakness coming to manufacturing and especially to the services industry. That is not just for Germany but also importantly for Europe. For now Asia, or at least China, appears to be the most virus resistant.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief