Global| Jul 06 2020

Global| Jul 06 2020German Orders Bounce Sharply Higher After a Devastating Run of Weakness

Summary

Germany's orders rebounded sharply in May after a devastating run of extreme weakness in March and April. Still over the last 24 months, there have only been eight monthly increases as there has been a period of weakness that preceded [...]

Germany's orders rebounded sharply in May after a devastating run of extreme weakness in March and April. Still over the last 24 months, there have only been eight monthly increases as there has been a period of weakness that preceded the impact of the coronavirus. Even with the sharp rebound of orders in May, the trends remain astonishingly weak.

Germany's orders rebounded sharply in May after a devastating run of extreme weakness in March and April. Still over the last 24 months, there have only been eight monthly increases as there has been a period of weakness that preceded the impact of the coronavirus. Even with the sharp rebound of orders in May, the trends remain astonishingly weak.

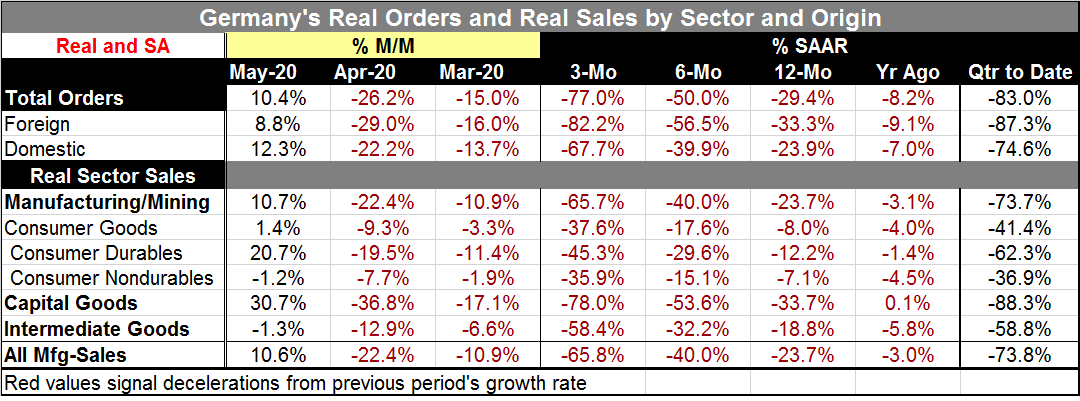

Concerns over world trade in the midst of the U.S.-China dispute as well as a still unresolved situation between the U.K. and EU over post-Brexit trade relations have hammered German trade and industrial orders. The drop in German orders loaded a 26.2% decline in April on top of a 15.0% drop in March. May brings a sharp rebound with a gain of 10.4% in overall orders as foreign orders gain 8.8% with domestic orders gaining back 12.3%. Still, it is not enough to revive the trend.

Orders overall are falling by over 20% to over 30% over 12 months overall and across categories. And this is after orders have fallen by 7% to 9% over the previous 12 months.

The economic shutdown in Germany and globally has hit German industry hard. Germany depends importantly on international trade. That has been drying up as the U.S.-China trade war raged and then as the reactions to the coronavirus added a more lethal and much sharper downtrend to the muddy trends already in place.

However, the Baltic dry goods index, an important indicator of global trade volumes, shows a significant counterpoint that demonstrates a revival in world trade patterns. And while the gain looks large on the daily chart, it is in fact still a small and gradual recovery that is progressing. But it is a recovery and it is progressing.

However, the Baltic dry goods index, an important indicator of global trade volumes, shows a significant counterpoint that demonstrates a revival in world trade patterns. And while the gain looks large on the daily chart, it is in fact still a small and gradual recovery that is progressing. But it is a recovery and it is progressing.

German orders and sales both have imploded and both show a May rebound that still leaves the implosion in gear. For example, despite a really substantial 30.7% increase in real sales of capital goods in May, sales of capital goods are deflating at a 78.0% annual rate over three months, a 53.6% annual rate over six-months and by 33.7% over 12 months. The rebound in May, substantial as it is, remains dominated by the past weakness. Two months into the new quarter, the quarter-to-date sales are still extremely weak.

The Germany economy remains in a deep hole. But it is clearly in the process of digging out. Still, the dig out looks like it will take a good deal of time. The virus continues to hover and it has come back in some regions as all of this makes it unclear just how completely and how fast economies can return to their former state of existence. Policy-makers remain wary and are not exuding optimism but rather promoting a cautious step-by-step increase in output and approach to recovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief