Global| Apr 06 2017

Global| Apr 06 2017German Orders Bounce Back in February

Summary

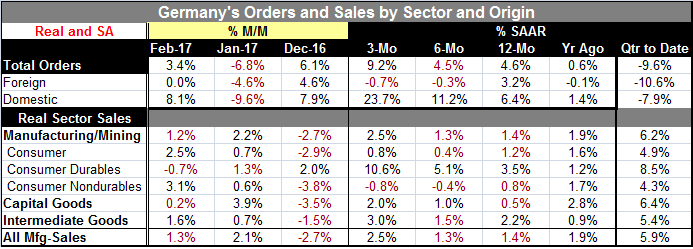

Total orders in Germany rose by 3.4% in February, rebounding from a 6.8% drop that followed a monthly rise of 6.1%. Over the past five months, German orders have been chopping up and down month-to-month as orders oscillated between [...]

Total orders in Germany rose by 3.4% in February, rebounding from a 6.8% drop that followed a monthly rise of 6.1%. Over the past five months, German orders have been chopping up and down month-to-month as orders oscillated between rising and falling. This sort of volatility makes it very hard to pin down the trend. However, the February gain boosts the three-month growth rate to a 9.2% annual rate but leaves the six-month and 12-month growth rates more or less the same at about a 4.5% pace. In the quarter-to-date, orders still are falling at a 9.6% annualized rate. So the February gain has not restored Q1 order growth to normalcy - and the recent pattern calls for an orders drop in March if it holds up.

Total orders in Germany rose by 3.4% in February, rebounding from a 6.8% drop that followed a monthly rise of 6.1%. Over the past five months, German orders have been chopping up and down month-to-month as orders oscillated between rising and falling. This sort of volatility makes it very hard to pin down the trend. However, the February gain boosts the three-month growth rate to a 9.2% annual rate but leaves the six-month and 12-month growth rates more or less the same at about a 4.5% pace. In the quarter-to-date, orders still are falling at a 9.6% annualized rate. So the February gain has not restored Q1 order growth to normalcy - and the recent pattern calls for an orders drop in March if it holds up.

Patterns of order growth

Domestic orders drive activity for now. Domestic orders rose by 8.1% in February as foreign orders were flat. And from 12-month to six-month to three-month, domestic orders are accelerating from a pace of 6.4% to 11.2% to 23.7, respectively. On that same time interval, foreign orders are decelerating as growth slips from a pace of 3.2% to -0.3% to -0.7%, respectively.

Dissecting the foreign sector

Foreign sector order growth shows that the greater weakness at the moment is within the euro area. Despite some reports that suggest that activity is heating up, German orders do not confirm this notion. Orders from within the euro area are up by 4.2% over 12 months but falling at an annual rate of 2% over six months and falling at a 1.3% pace over three months. Conditions are not progressively deteriorating, but order volumes are dwindling. For foreign orders outside the euro area, there is a 12-month gain of 2.6%, but that slows to a 1% pace over six months and further to a 0.5% annualized pace over three months. The foreign sector right now is not promising in terms of actual orders despite the pick-up that the PMI data have been promoting.

Sales patterns

Sales patterns

The chart shows that sales growth has gradually been dissipating. Over 12 months real manufacturing sales are up at a 1.4% pace; that is slower than their growth over 12 months for a year earlier when the pace was 1.9%. Over six months the sales pace is roughly unchanged at 1.3%, but that picks up to 2.5% (annualized) over three months. None of the big-three categories (consumer goods, capital goods and intermediate goods) shows steady sales acceleration or deceleration. But within consumer goods, durable goods sales are accelerating while nondurable sales are decelerating.

Sales in the quarter

With two months data in-hand, the quarter-to-date sales are solid with an overall pace of 6% in manufacturing and sector paces that lies between annualized rates of 4.3% and 8.5%.

German round up

The manufacturing order/sales conditions are solid with a hint of order weakness despite the rebound this month. If the monthly pattern stays on track next month, it will bring a decline in orders and that will leave the quarterly result even weaker. However, sales are relatively firm and even strong in the quarter-to-date. But their year-on-year pattern also shows some decay. On balance, the German orders and sales data are yet another set of accounting reports that fails to backstop the more buoyant message being spread by soft data surveys like the Markit PMI gauges.

Hard data soft data: what's-a-matter?

On that note, PMI gauges for China's manufacturing sector showed weaker activity in March. Hong Kong's PMI improved, but that jurisdiction still showed an overall net decline in its private sector. In India, the private sector improved as the central bank notched up its reverse repo rate. Germany did log a stronger PMI survey reading for its construction sector in March. Global conditions seem to remain in flux. Central bankers are itchy to make the transition to more normal polices. But today Mario Draghi said that ECB policies were not up for a review. In the U.S., various Fed officials still seek a policy of accelerating rate hikes and the newest wrinkle from yesterday's Fed meeting minutes was that Fed officials are planning to start scaling back the balance sheet and think that they may begin that task around the end of the year. If they do that, the pace of rate hikes will have to slow since balance sheet shrinking will swamp growth in somewhat the same manner as rate hikes, but with more uncertainty about the result. Even as we head for normalcy, we prepare to take another plunge into the unknown.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief