Global| May 08 2008

Global| May 08 2008German Order Trends are Mostly Cycling Lower

Summary

German orders have taken some time to weaken since the euro began climbing strongly. Arguably it is now a plethora of factors that are dogging the trend including the strong euro but also the fallout from the financial turmoil and the [...]

German orders have taken some time to weaken since the euro began climbing strongly. Arguably it is now a plethora of factors that are dogging the trend including the strong euro but also the fallout from the financial turmoil and the transmission of weakness from faltering growth in the US and elsewhere – to extent that theses things are different.

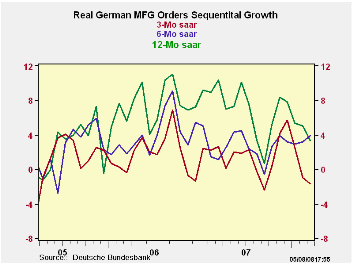

Orders both domestic and foreign have eased their pace from their year ago growth rate and also sequentially through six-month and three-month growth rates as well. Both domestic and foreign orders have decelerated their pace. The quarterly readings show negative growth rates for both domestic and foreign orders in 2008-Q1.

But this slowing has yet to hit the pace of sales. Sales growth rates are still largely rising except for consumer goods –long the Achilles Heel of this expansion. Capital goods sales have slowed but are still strong in the Q1 period. Intermediate goods sales remain relatively robust.

On balance the orders figure that tend to lead the cycle show that he boom days in MFG are coming to a close. Since they are slowing sharply and since growth rates have turned negative, they hint that the slowdown could be severe.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Mar-08 | Feb-08 | Jan-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | QTR-2-Date | |

| Total Orders | -0.6% | -0.6% | -0.7% | -7.2% | -3.6% | 5.1% | 11.5% | -5.3% |

| Foreign | -0.4% | -1.1% | -0.4% | -7.6% | -3.9% | 6.8% | 12.7% | -9.6% |

| Domestic | -0.9% | 0.0% | -0.9% | -6.6% | -3.4% | 3.3% | 10.4% | -0.2% |

| Sector Sales | ||||||||

| MFG/Mining | -0.5% | -0.2% | 2.1% | 5.9% | 2.9% | 4.6% | 9.3% | 9.2% |

| Consumer Goods | 0.2% | -1.8% | 1.0% | -2.3% | -1.1% | -0.7% | 5.6% | -1.0% |

| Consumer Durables | -0.9% | -0.3% | 0.8% | -1.6% | -0.8% | 0.4% | 5.1% | 4.3% |

| Consumer Nondurables | 0.4% | -2.0% | 1.1% | -2.2% | -1.1% | -0.9% | 5.9% | -2.0% |

| Capital Goods | -2.7% | -0.8% | 4.2% | 2.7% | 1.3% | 5.4% | 9.7% | 10.9% |

| Intermediate Goods | 1.9% | 1.6% | 0.2% | 15.5% | 7.5% | 6.7% | 11.2% | 13.2% |

| All Manufacturing Sales | -0.5% | -0.2% | 2.1% | 5.7% | 2.8% | 4.1% | 9.3% | 9.1% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.