Global| Mar 05 2021

Global| Mar 05 2021German Order Growth Gets Back in Gear Despite the Headwinds

Summary

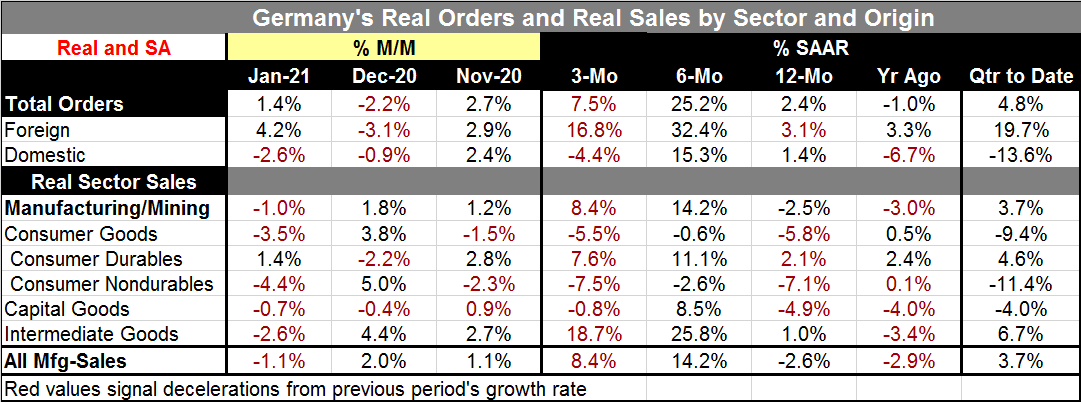

German order growth is back in gear with total orders rising by 1.4% month-to-month in January. The gain, however, is generated wholly by foreign orders that surged by 4.2% in January after dropping by 3.1% month-to-month in December. [...]

German order growth is back in gear with total orders rising by 1.4% month-to-month in January. The gain, however, is generated wholly by foreign orders that surged by 4.2% in January after dropping by 3.1% month-to-month in December. Still, German domestic orders fell by a sharp 2.6% in January, a figure made large by the fact that domestic orders also fell by 0.9% in the previous month.

German order growth is back in gear with total orders rising by 1.4% month-to-month in January. The gain, however, is generated wholly by foreign orders that surged by 4.2% in January after dropping by 3.1% month-to-month in December. Still, German domestic orders fell by a sharp 2.6% in January, a figure made large by the fact that domestic orders also fell by 0.9% in the previous month.

Unevenness in German order growth

German orders (seasonally adjusted, real orders with growth rates presented at an annualized rate) are rising at a pace of 7.5% over three months. This is down from its 25.2% pace over six months but up from its 2.4% gain over 12 months. Foreign orders are up at a 16.8% pace over three months but similarly slow from their six-month pace and exceed their 12-month gain. German domestic orders are different; they fall at a 4.4% pace over three months and also are weaker than their 15.3% six-month pace, but they are additionally weaker than their 1.4% year-on-year gain. German domestic orders are still below their level of January 2020 just before the virus struck, unlike foreign orders. In the quarter-to-date, German orders are rising at a 4.8% annualized rate, the result of a 19.7% pace for foreign orders dominating a -13.6% pace of decline for domestic orders.

Real sales in January

Real sales by sector in Germany show weakness that is widespread in January. Mining and manufacturing sales combined fell by 1%. Manufacturing sales fell by 1.1%. Consumer goods sales fell by 3.5%, capital good sales fell by 0.7% and intermediate goods sales fell by 2.6% - all in January. Within consumer goods, durables sales rose by 1.4% as nondurables sales fell by a large 4.4%. Sales also decelerated broadly in January compared to December.

Real sector sales momentum

German manufacturing does not seem to be gaining a lot of momentum. Over three months, manufacturing sales are rising at an 8.4% annualized pace, stronger than the 7.5% pace for orders overall. Orders are not pulling sales higher; sales are outpacing orders. Manufacturing sales are slower over three months than over six months just like orders and they also show stronger growth over three months than over 12 months. In fact, real sales decline over 12 months, falling by 2.6%. Consumer goods and capital goods sales both decline over 12 months as only intermediate goods sales are higher, rising by 1%. This is where orders lead sales as orders are stronger over 12 months, a time span over which real sales are falling.

Quarter-to-date sales

Quarter-to-date real sector sales for manufacturing rise by 3.7%. Consumer goods sales fall at a 9.4% pace and capital goods sales fall at a 4%pace; but intermediate goods sales are rising at a 6.7% pace.

Virus impact

Germany imposed restrictions to control the virus especially with the new more infectious strain in circulation. Restrictions were kept in place through late-February; then were extended. From December onward the incidence of infection in Germany declined, but it has since plateaued and even begun to creep higher again in early-March. Deaths by virus peaked at the end of December but were still not far off that peak in mid-January since then the daily death-rate has fallen but it is still above the peak pace of April 2020. So while there is progress being made, there is still a high level of virus circulating compared to what Germany had experienced earlier.

Virus plans

Angela Merkel had extended the virus restrictions but now seeks to ease the curbs on activity by next week. Germany has been in some sort of partial lock down since November. Hairdressers were recently allowed to re-open. Next flower shops, bookstores and garden centers will be allowed to open. However, most other shops including restaurants and sporting facilities are expected to have an order invoked to remain shut until March 28 (Source here). Germany is still in the midst of fighting off this new more durable virus strain. Fortunately, Germany’s factory sector has been able to do relatively well even in the grip of the virus. PMI data up-to-date through February show a manufacturing diffusion value at 60.7 which is quite strong. But that is juxtaposed to a services diffusion reading of 45.7 that shows services in a state of contraction and quite weak. Such is the impact of the virus on the German economy. The way forward is still trying, but progress is being made.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief