Global| Apr 08 2009

Global| Apr 08 2009German New Orders Decline

Summary

The growth rates for German industrial orders are not getting progressively worse, but they still are bad and the three-month growth rate still is worse than the six month growth rate. There may be a hint or whiff of slowing down the [...]

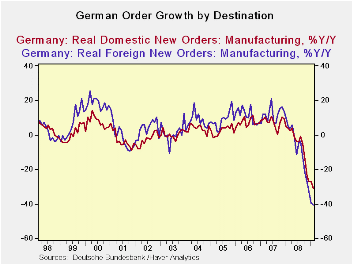

The growth rates for German industrial orders are not getting

progressively worse, but they still are bad and the three-month growth

rate still is worse than the six month growth rate. There may be a hint

or whiff of slowing down the pace of the order decline, but it’s a

vague hint. Over THREE MONTHS the pace of order decline in real terms

is -51.5% led by a 60.2% pace of decline in foreign orders and a lesser

but still severe 39.3% pace of decline in new domestic orders.

The growth rates for German industrial orders are not getting

progressively worse, but they still are bad and the three-month growth

rate still is worse than the six month growth rate. There may be a hint

or whiff of slowing down the pace of the order decline, but it’s a

vague hint. Over THREE MONTHS the pace of order decline in real terms

is -51.5% led by a 60.2% pace of decline in foreign orders and a lesser

but still severe 39.3% pace of decline in new domestic orders.

The pace of order decline in the current quarter annualized is

just about the same as the pace in 2008-Q4. Meanwhile real sector sales

continue to drop at a steadily accelerating pace. Capital goods

declines lead the parade over three-months, six months and twelve

months.

These sorts of declines cannot go on for very long without

bringing disaster. It is reasonable to think we are on the cusp of

seeing a slowdown in the rate of unravel. There are some stimulus

programs afoot in Europe. But just as clearly the Euro-view and the ECB

view has been to be less helpful than the view from the authorities in

the US. In global terms these ‘guys’ are intending to piggy-back a bit

on US generated stimulus.

I was shocked to see how blasé Europe really is when Juergen

Stark of the ECB was disapproving of the extension of IMF credit. We

are in the middle of a real financial and growth problem. And Stark was

not pleased to get some help that would be channeled to the neediest.

Without this help, recession would hit less developed and smaller

nations harder; they would have to wait for the larger economies to

pick up in order to benefit. Europe is not doing that every quickly, as

we just observed, above. In the case of Europe the biggest risk is in

Eastern Europe and there the EU has taken some special steps to provide

assistance. This recession has been a good case study in how nations

‘take care of their own’. But the IMF money which is less that way and

is geared more toward need without bilateral strings attached is very

helpful and timely. I do not share the Stark/ECB reluctance.

For now the German data on industrial orders tell us that

Europe is weakening at a rapid pace. German domestic demand may be

faring a tad better as it spins off the vaguest hint of slowing its

descent. But for foreign orders the assessment for German data remains

quite bleak.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Feb-09 | Jan-09 | Dec-08 | 3-MO | 6-Mo | 12-Mo | Yr Ago | QTR-2-Date | |

| Total Orders | -3.5% | -6.7% | -7.3% | -51.5% | -30.4% | -36.3% | 4.4% | -54.5% |

| Foreign | -1.3% | -10.9% | -9.7% | -60.2% | -36.9% | -40.7% | 4.7% | -63.7% |

| Domestic | -5.7% | -1.8% | -4.6% | -39.3% | -22.1% | -30.9% | 3.9% | -41.2% |

| Real Sector Sales | ||||||||

| MFG/Mining | -4.2% | -6.6% | -5.5% | -49.0% | -28.6% | -23.2% | 5.1% | -49.7% |

| Consumer | -3.2% | -6.0% | 3.4% | -21.7% | -11.5% | -11.2% | -0.6% | -27.4% |

| Cons Durables | -7.9% | -2.2% | -5.3% | -47.0% | -27.2% | -22.3% | -0.6% | -41.3% |

| Cons Non-Durable | -2.5% | -6.6% | 4.9% | -16.6% | -8.7% | -9.3% | -0.5% | -24.6% |

| Capital Gds | -4.8% | -9.4% | -8.4% | -61.0% | -37.5% | -29.2% | 9.2% | -61.3% |

| Intermediate Gds | -3.5% | -4.6% | -7.5% | -47.5% | -27.5% | -24.2% | 3.9% | -48.5% |

| All MFG-Sales | -4.3% | -6.6% | -5.8% | -49.7% | -29.1% | -23.4% | 5.1% | -50.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief