Global| Aug 07 2007

Global| Aug 07 2007German IP Weakens as Orders Surge

Summary

For the full quarter total German IP is up by 0.3%. Construction is off by 31% at an annual rate in Q2, accounting for much of the drag. But MFG is up by 0.8% roughly the same as for consumer goods, intermediate goods and capital [...]

For the full quarter total German IP is up by 0.3%. Construction is off by 31% at an annual rate in Q2, accounting for much of the drag. But MFG is up by 0.8% roughly the same as for consumer goods, intermediate goods and capital goods output. Of course in Q2 2007 German orders are up at a spectacular 17.6% annual rate.

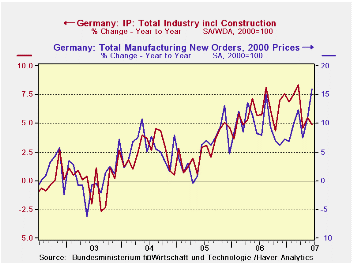

The accompanying graph shows that orders often peak at the same time or before industrial output (note that that is a two-scale chart). In that sense the ongoing rise in orders is reassuring. From Nov 2006 through Jan 2007 orders growth did slip below the pace of growth for output. This event is coincident with the year-end/new year period when the VAT hike was initiated and that tax accounted for some uncertainty at the time. Uncertainty seems to have interrupted the flow of new orders more than of output because what we see is that the flow of orders was interrupted at that time but the growth of output was not. Now however there is a lull in output in Q2 as orders have sped ahead. The reasonable question to ask is whether this is some sort of catch up in orders after that year-end lull when IP was stronger than orders – since that is an unusual configuration for these two series, to have output stronger than orders. Or is the new spurt in orders entirely of a different cause and does it point to even stronger gains in IP for the period ahead?

At this time most Europeans are very upbeat and no end of laudatory statements have been made about Euro-growth and growth prospects. But the fact remains that some Euro area members are not doing so well and that even for Germany much of this strength in orders comes from cross-border transactions. The latter trend seems to imply that the spurt in orders is for real and reflects some new demand phenomenon. But the UK has also turned in some hot/cold signals recently and Italy is showing a protracted period of anemia. France benefited from elections and post-election euphoria and it is not clear that it will continue to have so much good news to buoy its spirits in the period ahead. Sarkozy can only keep pointing his finger at others as the source of the problem for so long until one day he steps in front of a mirror.

I think the series of German reports from the Zew and IFO indexes peaking to the flap about IP in Germany to some irregular signals from the UK as well as ongoing weakness in Italy point to some real world problems creeping into the Euro area. Europe still does not have a flexible economy. The US is still clearly the leader on that score. The raft of mini-problems or question marks arising in Europe I believe will prove to have some real causes behind them.

| SAAR except M/M | Jun-07 | May-07 | Apr-07 | 3-month | 6-month | 12-month |

| IP total | -0.4% | 1.9% | -1.5% | 0.0% | 2.8% | 4.9% |

| Consumer Goods | -2.5% | 1.3% | -0.9% | -8.2% | -1.5% | 1.9% |

| Capital Goods | -0.9% | 2.1% | -1.1% | 0.3% | 6.7% | 7.1% |

| Intermediate Goods | 0.8% | 2.1% | -2.1% | 3.0% | 4.5% | 7.5% |

| Memo: Construction | -2.1% | 0.2% | -5.6% | -26.5% | -17.0% | -3.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief