Global| Feb 07 2017

Global| Feb 07 2017German IP Unexpectedly Rolls Over in December

Summary

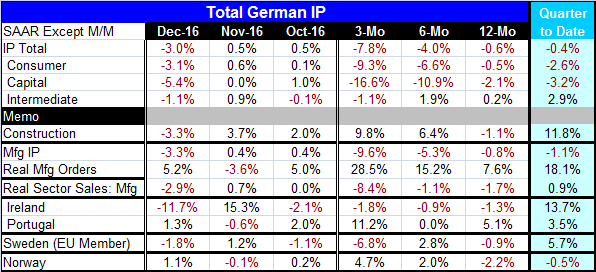

German industrial output fell sharply and unexpectedly at the end of 2016 as output declined by 3% month-to-month in December. Both construction and manufacturing output fell by 3% or more in December. Widespread declines There were [...]

German industrial output fell sharply and unexpectedly at the end of 2016 as output declined by 3% month-to-month in December. Both construction and manufacturing output fell by 3% or more in December.

German industrial output fell sharply and unexpectedly at the end of 2016 as output declined by 3% month-to-month in December. Both construction and manufacturing output fell by 3% or more in December.

Widespread declines

There were declines in all three major categories: consumer goods, capital equipment and intermediate goods. These declines were all the more surprising because other surveys like the PMI survey from Markit and the IFO survey had been upbeat and, of course, real orders released just yesterday were so strong. But IP is about what is happening now and orders are about future demand.

Reason for sustained optimism?

There is a relatively strong year-over-year correlation between real orders and IP and also with real sales. Currently IP and sales are weak (IP and real sales both are decelerating steadily on growth rates from 12-month to six-month to three- month). But orders have moved up very strongly as have other well-regarded surveys of German and EMU economic activity.

All is not well in Euroland: something old

Still, the latest spat is between Mario Draghi and those that want a very narrow definition of inflation and want the ECB reacting to energy prices and hiking rates very soon because of that. Draghi is telling us that it is too soon to withdraw the euro-stimulus. The Bundesbank has a long history of fighting inflation from out front. It wants the ECB to stay in that tradition. So far, Draghi holds the cards, but we could be headed for a euro-standoff.

Something new

Most German data, apart from this IP report, have been looking strong because the German economy has done so well. Germany has the lowest unemployment rate in the EMU and the lowest rate since Germany was reunified. This could put Germany on the cutting edge of the flash point for inflation and it was there one month ago, but that development recently has shifted. In terms of the freshest PPI data, Germany is still somewhat inflation resistant. Obviously, inflation transmission developments as oil prices rise are going to be organic developments we will have to watch. No immutable rules say that inflation has to rise more slowly in Germany, especially as long as Germany has the lowest unemployment rate in the EMU.

Too much borrowed

In addition, old problems are yet to be put to bed. In a report today, the IMF mentioned that Greek debt levels have been declared as not sustainable. There are two ways to look at that: one is that since they are not sustainable, we do not have to worry about sustaining them. The second is that if these levels are not sustainable, how are they going to be made so that they are? Does Greece need more austerity (more blood-letting please)? Will Greece have another financial crisis? Will Europe have to have a round of debt forgiveness? The IMF has made it clear that it is not forgiving debt. The rest of Europe has been play the 'rolling loan carries no loss' game. And while that one is fun while it lasts, that's the one that the IMF implicates in saying that Greece's debt is not sustainable. Europe needs to find a solution which will end with debt forgiveness. Until Europe confronts reality, Greece will be on a never-ending short leash of new austerity programs and Europe will keep giving Greece new tranches of credit so it can draw them and 'repay' is outstanding debt. Can you say Ponzi scheme? I ask this because that is what it is beginning to look like. Obviously, with elections in Europe, particularly in Italy and France, Europe does not want to parade around another Greek bailout and whip up more anti euro-area animal spirits in the midst of elections that already suffer from a populist backlash. And if it did that, how would Spain and Portugal react to that sort of favored treatment for Greece, treatment to which they would have to contribute?

The European blues

Draghi is right about Europe being better off but still having a way to go. Germany recognizes nothing except today is the first day of the rest of your life so it is the right time to start to do the right thing. That attitude at the end of the financial crisis is a good part of the reason that Europe is in the fix it's in. I realize that good financial behavior is a bit like dieting and it's always better to start a diet tomorrow than today. But sometimes there are extenuating circumstances. The German method has gotten a lot of adjustment in place in Spain and Portugal, some in Italy and even in Greece. But this progress has come at a cost; the price has been the alienation of the people who have suffered. Having said that, know that Greece is still a basket case living in a borrowed basket. Europe has some big challenges to face. And uneven growth or an uneven inflation pass-through could make the job that much tougher. A good performing German economy may not make things better and may even make them worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief