Global| Apr 09 2015

Global| Apr 09 2015German IP Steps Up in February Despite Downward Revisions and 12-Month Drop

Summary

German economic data have become a bit more confused recently. Yesterday German orders data were decisively downbeat with what leadership there was coming from an unexpected source, the consumer sector. In today's industrial output [...]

German economic data have become a bit more confused recently. Yesterday German orders data were decisively downbeat with what leadership there was coming from an unexpected source, the consumer sector. In today's industrial output report, we see German industrial production revised lower so that it is now down year-over-year. While the monthly data show a rebound, trends in orders compared to trends in output do not look they are reporting on the same economy.

German economic data have become a bit more confused recently. Yesterday German orders data were decisively downbeat with what leadership there was coming from an unexpected source, the consumer sector. In today's industrial output report, we see German industrial production revised lower so that it is now down year-over-year. While the monthly data show a rebound, trends in orders compared to trends in output do not look they are reporting on the same economy.

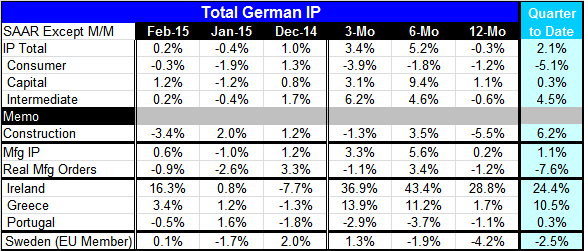

In February, output is gaining traction. February output is up mostly on the strength of capital goods where output has jumped by 1.2% after falling by the same 1.2% in January. Intermediate goods output is up by 0.2%, also reversing part of a decline in January. Consumer sector output is lower by 0.3% in February.

Sequential growth rates show output in the capital goods sector up over all horizons, but it is intermediate goods output that is accelerating the most clearly. Output in the consumer sector is declining on all horizons and showing sequential deceleration. This is in stark contrast to the strength reported in the orders for consumer goods in yesterday's report. Also there is a contrast with the growth in capital goods output to the lagging orders for capital goods reported yesterday.

The picture of the German economy simply does not want to resolve itself along clear cut lines. However, in a companion report released today, German trade figures confirm the ongoing strength in German exports through February but also give a bit of a mixed picture on capital goods export trends even as capital goods imports are consistently strong.

The chart, memorializing the year-over-year trends, shows still decelerating tends in play for the output of consumer goods and intermediate goods. Capital goods output growth rates have softened but still hover in positive territory. This is the more or less traditional picture of the German economy being `propped up' by its capital goods sector. That view is more or less in play on the shorter horizon output data too (3-month, 6-month and 12-month) and this is what is different from the picture we get from German factory orders where the consumer sector is doing the propping.

Despite some irregularity and prevarication in the data, we continue to hold an upbeat assessment. We know recent euro area reports have been a bit more solid and we also know that the euro exchange rate has been on a broad weakening trend, a factor that should breathe life into German orders, output and exports. To the extent that these reports are not so clearly on board with the expected strength, we tend to chalk that up to data irregularities and weather effects, but we are also open-minded about the potential for disappointment.

Of course, economic reports in the United States have swung from unexpectedly strong to unexpectedly weak. So what Germany is experiencing is not in isolation. And this is just another reason to be careful to not dismiss reports of unexpected weakness out of hand. The world's major economies are experiencing a good deal of irregularity. China has slowed and is struggling. Japan, having gotten a boost from QE, is still staggering under the backlash from its consumption tax hike. The U.S., an important energy producer, is feeling the downside of lower energy prices on its supply side as well as the blowback from the stronger dollar. In this environment, it is naturel to look for Europe with ongoing currency weakness to get a boost from that. But it is also important to bear in mind that the global economy is still weak and that it may still be a difficult environment in which to sustain strength in output and exports.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.