Global| Nov 08 2016

Global| Nov 08 2016German IP Steps Back in September and Does Not Enjoy the View

Summary

To and fro with output gains and losses The nearly 2% step back in German output in September follows an even stronger gain of 3% in August. But that has followed a sizeable drop in July and the see-saw patterned extends farther back. [...]

To and fro with output gains and losses

To and fro with output gains and losses

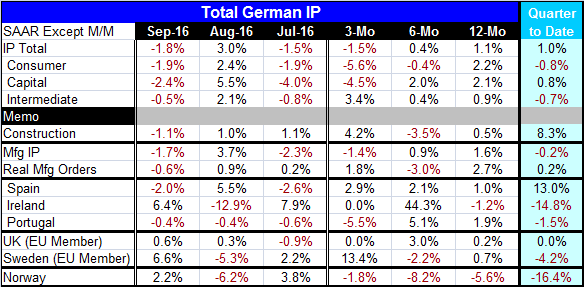

The nearly 2% step back in German output in September follows an even stronger gain of 3% in August. But that has followed a sizeable drop in July and the see-saw patterned extends farther back. German IP has been down then up month-to-month since March. But the up-down string by month or by clusters of months has been going on for much longer. This Mexican jumping bean pattern makes it hard to nail down a trend. German IP growth still is positive and it appears to have made some improvement, but the degree of improvement is narrow and hard to be sure of due to the extreme volatility.

Growth trends are not reassuring

Sequential growth rates show IP growth is steadily weaker on shorter horizons from 12-monht to six-month to three-month. IP is falling over three months at a 1.5% annual rate. Output is also falling in two of three sectors with losses over three months in consumer goods and capital goods that are only partly offset by an increase in intermediate goods output.

Construction

Construction output fell in September like the other three sectors, but it shows a net gain (at a 4.2% annualized rate) over three months.

Manufacturing

Manufacturing IP is off over three months and decelerating in its annualized growth rates from 12-month to six-month to three-month. This is contrary to the manufacturing PMI pick up.

Real orders

Real manufacturing orders fell in September, but are up over three months and have no clear pattern in their sequential growth rates.

German output growth in Q3

In the just completed Q3 (quarter-to-date column), overall German output is up at a 1% pace in the quarter but manufacturing output is lower falling at a -0.2% annual rate with construction sector output flying as it is gaining at an 8.3% annual rate. Real manufacturing orders are up at just a 0.2% annual rate in Q3. On balance, German growth is not terrifically strong. The trends are poor, but year-over-year growth rates are consistently positive.

IP in other early reports in EU

There are six other early reporting EU or EU/EMU members. Among these, Spain and Portugal show output declines in September while Ireland, Sweden, Norway and the U.K. show output increases-and most of these month-to-month increases are fairly sizeable. All of the monthly changes by these countries represent reversals from the previous month except for the U.K. which has posted back-to-back monthly gains. Over three months, output in Portugal and Norway is lower in balance, in the U.K. and Ireland it is unchanged, and in Spain and Sweden output is higher on balance. Sequential growth rates from 12-month to six-month to three-month show output is accelerating in Spain alone. It is showing no clear decelerating trend in any other of these countries, but output is contracting on all horizons in Norway. Norway has fallout as weak energy prices take their toll on this oil producing country (North Sea oil). In the third quarter, output is falling on balance in four of these six nations with output unchanged in the U.K. Output is higher in Q3 only in Spain where it has posted an outsized 13% annual rate gain.

Broader trends/overview

Overall the Markit manufacturing gauges have been showing some improvement and the trend increase in German IP is more or less on board with that. In news today, China reported out weaker exports than expected, sending a continuing chill up the spine of those looking for global growth to pick up its pace. However, in Japan the leading economic index for September was less weak than expected while back in Europe the U.K. continues to report out gains in permanent job placements as well as an unexpected pick-up in same store sales (like-for-like sales, in U.K. parlance). For every 'yes' there is a 'but' and vice versa. In the U.S. today, the NFIB small business index (formally a survey of 'independent businesses') ticked higher but still remains weak. There is no evidence of any growth breakout anywhere. And neither is there any real backsliding. Growth simply seems to keep on keepin' on everywhere and that's about it. Markets are braced for the Fed to hike rates in December. And for now they are even keeling in the wake on the newest U.S. FBI position that clears Hillary Clinton ahead of the U.S. elections (today!). Despite relatively modest margins in the polls, the odds of a Clinton win are overwhelming put by one service at 90% just today. There seems to be little uncertainty about who will win, but a lot of uncertainty about what will happen next in the U.S., abroad, in geopolitics, in economics and with fiscal policies and monetary policies as well -as monetary policy manipulation seems to have come to the end of its rope. There is little that we are really sure of at the moment. Is this the calm in markets before the storm? We shall soon find out.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief