Global| Mar 06 2015

Global| Mar 06 2015German IP Shows Some Upside

Summary

German industrial production shows signs of stabilizing and reasserting growth in the January report. The chart of year-over-year growth rates shows that by sector the year-over-year trends have stopped falling and that capital goods [...]

German industrial production shows signs of stabilizing and reasserting growth in the January report. The chart of year-over-year growth rates shows that by sector the year-over-year trends have stopped falling and that capital goods in particular are showing a bounce to a higher rate of growth.

German industrial production shows signs of stabilizing and reasserting growth in the January report. The chart of year-over-year growth rates shows that by sector the year-over-year trends have stopped falling and that capital goods in particular are showing a bounce to a higher rate of growth.

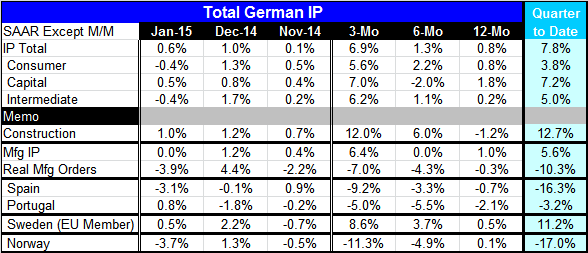

Inside one year the table shows sequential growth rates from 12 months to six months to three months all annualized are showing a near universal tendency to higher rates of growth. Over three months, all sector growth rates for consumer goods, capital goods and intermediate goods exceed 5.5%. Since IP data are inflation-adjusted, these all are substantial rates of expansion.

The German construction sector also is showing a substantial lift, posting a three-month annualized rate of growth at 12%.

Manufacturing growth has picked up to 6.4% at an annual rate over three months but real manufacturing orders are showing a tendency toward deceleration. Weak orders are the one fly in the ointment for Germany in this report.

In the quarter-to-date, German IP and its three main sectors are all sporting solid-to-strong rates of growth. Manufacturing has a 5.6% pace of growth in the quarter-to-date; that is countermanded by a 10.3% rate of decline in German real manufacturing orders.

Elsewhere among the early reporting EU/EMU members, we find a preponderance of quarter-to-date weakness. Only Sweden shows a gain in industrial production on a quarter-to-date basis. Over three months, Spain, Portugal and Norway each show IP declines with Sweden posting the lone increase. Still, this sample of countries is too small and disparate to have much meaning for all of Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief