Global| Mar 09 2020

Global| Mar 09 2020German IP Shows Some Life in January; The Eye of the Storm: Post Trade Wars Pre-Corona

Summary

Arguably Germany's industrial production finds itself in the eye of the storm. There is some January rebound as U.S. China tensions ratcheted down with the year-end Phase-One trade deal. With that, markets began to breathe a sigh of [...]

Arguably Germany's industrial production finds itself in the eye of the storm. There is some January rebound as U.S. China tensions ratcheted down with the year-end Phase-One trade deal. With that, markets began to breathe a sigh of relief even as the U.S. and China had a lot of work to do. That modest deal seems to have lifted a pall from markets and spurred some activity. Still, the 'pause-that-refreshes' effect has not apparent in the Baltic dry goods trade volume index that has remained weak with only a modest rebound.

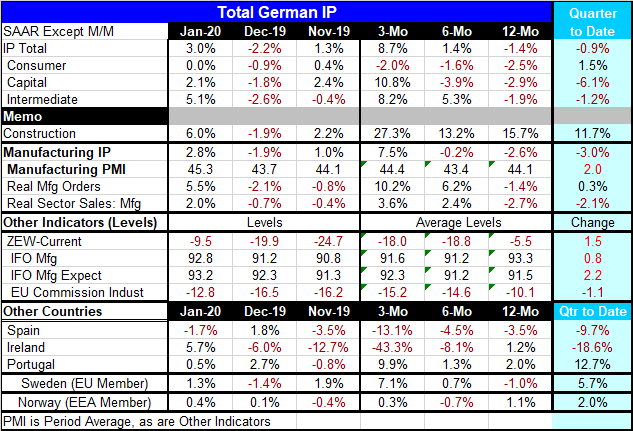

German IP trends largely signal rebound

Still, German manufacturing has seen output rise by 3% in January after a 2.2% drop in December. The 12-month to six-month to three-month sequence of growth rates has been accelerating overall, for intermediate goods and for manufacturing. However, consumer goods and capital goods as well as construction all show a stronger 3-month growth rate than their respective 12-month growth rates. Even when a rebound is not sequential, its evolution is clear.

German indicator trends are contrary

In contrast, indicators have mostly been slipping on this same timeline sequence. Those that are not sequentially weak at least have weaker readings over three months than over 12 months. The Baltic dry index has stopped falling, but it does not show much rebound at this time. The indicators give the opposite signals that a rebound is not in fact on its way.

And now, of course, there is the global pandemic coronavirus that is spreading like wildfire.

Market reactions

Stock prices are in free-fall and OPEC as a result of an internal tussle has opened the spigot to flood the markets with oil driving prices lower even as demand has gone slack. Prior to the Saudi action to increase output the Saudis and Russia were trying to come to an agreement on how to cut back output further to support prices. In the end, Russia was unwilling to cut back its output anymore and would only agree to extend existing output moderation. The Saudis were not willing to bear the brunt of the output reductions to support prices. In response, the Saudis opted to 'blow it all up' by flooding the market with oil and forcing Russia and others back into negotiations.

The impact on confidence

This complicates the global picture. As oil prices plunge, they will drag lower other commodity prices too. Also this will worsen the outlook for oil production and spread the pain especially to the oil and gas and fracking industry in the U.S. as well as globally. The coronavirus meanwhile is spreading and economic growth is slipping. Confidence is being undercut as no one has a clear idea how bad this will get or how long it will go on.

Other Europe

Spain and Ireland are showing increased decay rates of IP as the profile of output falls. But Portugal and Sweden show output on an upswing. Norway has no clear pattern but seems to lean more toward weakness. The Baltic dry shipment index remains weak and is not showing another jolt lower.

Summing up

On balance, it is hard to take the German IP bounce at face value and to think it is a harbinger of any sort. The impact of the virus on activity and on expectations is severe, but the virus only spreads a particular strain of the flu. It is only really lethal to old and older people and to those who have pre-existing illnesses. The last I read no one under the age of 30 had died from the coronavirus. So the danger of the virus is somewhat limited or at least compartmentalized. After the global economy gets through the scare-phase, the flu may continue to spread. But with the right fiscal policy response, the damage of the downturn can be limited. I don't think monetary policy will be able to have much effect here either on the reality of the situation or on affecting expectations or bolstering confidence. How does it help confidence for the Fed (that still can cut rates) to cut rates to dead zero, use up all its ammunition, have nothing potent left to do, and have no impact on the economic situation? For the BOJ, ECB or BOE to do likewise raises the same questions: Why? For what good? To what end? This is not a problem on the plates of the central banks except for them to provide sufficient liquidity. Central banks and regulators may have to provide some dedicated credit facilities but cutting rates is not the way to go.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief