Global| Oct 08 2008

Global| Oct 08 2008German IP Shows Some Bounce

Summary

German New Orders and retail sales rose unexpectedly in August. So the August rise in IP of 3.4% is less of a surprise than it otherwise would be. There is a growing consensus that the timing of holidays has had a lot to do with the [...]

German New Orders and retail sales rose unexpectedly in

August. So the August rise in IP of 3.4% is less of a surprise than it

otherwise would be. There is a growing consensus that the timing of

holidays has had a lot to do with the false strength being recorded in

August. It is hard to find anyone who wants to take these signs of

strength to heart.

Still IP trends do not yet look as weak as the dwindling

(pre-August) trends in orders and in retailing (see the current orders

trends in the table above). At 1.7% 12-month IP growth is firm. Over

six months IP is off by 0.6%. But over three months it is up at a

whopping 7.7% pace. Still, quarter-to-date IP is off at a 2.2% annual

rate.

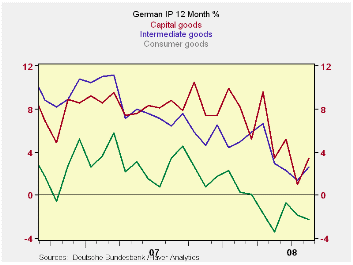

The patterns in IP also mark most of the major categories. A

minor exception is for quarter-to-date growth. There, the negative

growth in the quarter is all due to severe weakness in capital goods

output. Consumer goods and intermediate goods output each still are

advancing in the quarter but at a near crawl, a 0.5% annual rate for

both.

| Total German IP | |||||||

|---|---|---|---|---|---|---|---|

| Saar except m/m | Aug-08 | Jul-08 | Jun-08 | 3-mo | 6-mo | 12-mo | Quarter-to-Date |

| IP total | 3.4% | -1.6% | 0.2% | 7.7% | -0.5% | 1.7% | -2.2% |

| Consumer Goods | 3.0% | -1.6% | 0.5% | 7.7% | -1.2% | -2.3% | 0.5% |

| Capital Goods | 3.9% | -3.1% | 1.7% | 9.7% | -1.0% | 3.4% | -6.4% |

| Intermediary Goods | 2.6% | -0.6% | -0.5% | 6.4% | 1.6% | 2.6% | 0.4% |

| Memo | |||||||

| Construction | 5.5% | -2.6% | -2.4% | 1.0% | -19.2% | 0.5% | -3.8% |

| MFG IP | 3.2% | -1.8% | 0.6% | 8.0% | 0.0% | 2.0% | -2.4% |

| MFG Orders | 3.6% | -1.3% | -2.6% | -1.2% | -7.3% | -1.3% | -7.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief