Global| Mar 07 2008

Global| Mar 07 2008German IP Sees Huge Lift From Capital Goods

Summary

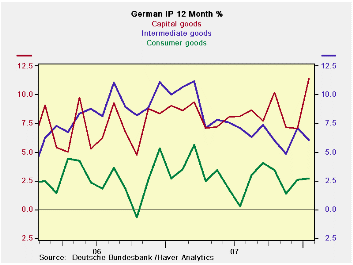

German IP was a breath of fresh air in January. But it may not have been made in the best of circumstances. Capital goods output surged by 6.2% m/m possibly a result of special rules favoring investment that are phasing out. [...]

German IP was a breath of fresh air in January. But it may not have been made in the best of circumstances. Capital goods output surged by 6.2% m/m possibly a result of special rules favoring investment that are phasing out. Construction output skyrocketed by 11.7% m/m on what obviously was a beneficial weather effect that will not just go away but will unwind in the months ahead and suck growth out of IP. As a result, in the new quarter construction is advancing at 111% pace and capital goods output at a 40.2% annual rate - eye popping numbers. These are two special cases. Meanwhile, consumer goods output tailed in the month falling by 0.6% m/m. and intermediate goods output fell by 1% m/m. Still MFG IP rose by 1.9% in January and is up at a 19.6% pace in the new quarter. The IP numbers are in sharp contrast to the 1.5% drop in January orders and the 7.6% drop in orders in Q1.

So Germany has some cross-currents. Currently the strength is lodged in areas that look be temporary or related to expiring stimulus. The more important, lasting, force of consumer spending continues to lag. Germans looking for better times in 2008 were uniformly pinning hopes on the consumer. Consumer is now a clear laggard. The IP figure tells us the same thing other retail reports have been saying about the consumer. Moreover, the weakness in orders tell us that the surge in output is not likely to last.

| Total German IP Quarter | |||||||

|---|---|---|---|---|---|---|---|

| SAAR except m/m | Jan-08 | Dec-07 | Nov-07 | 3-mo | 6-mo | 12-mo | Quarter-to-Date |

| IP total | 1.8% | 1.5% | -0.3% | 13.2% | 10.1% | 7.0% | 18.0% |

| Consumer | -0.6% | 2.7% | -1.2% | 3.5% | 8.5% | 2.7% | 4.9% |

| Capital | 6.2% | -0.8% | 0.2% | 24.7% | 17.5% | 11.4% | 40.2% |

| Intermediate | -1.0% | 3.8% | -0.2% | 10.6% | 7.1% | 6.0% | 8.7% |

| Memo | |||||||

| Construction | 11.7% | 2.2% | -0.2% | 68.5% | 30.8% | 4.5% | 111.3% |

| MFG IP | 1.9% | 1.7% | -0.2% | 14.8% | 11.4% | 7.5% | 19.6% |

| MFG Orders | -1.5% | -1.1% | 3.0% | 1.2% | 9.3% | 9.6% | -7.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief