Global| May 07 2021

Global| May 07 2021German IP Rises Strongly in March After a Period of Weakness

Summary

German industrial production was up in March after two months that showcased severe declines; that had followed four months that had brought quite strong gains. These are statistics from the original post-virus recovery period, the [...]

German industrial production was up in March after two months that showcased severe declines; that had followed four months that had brought quite strong gains. These are statistics from the original post-virus recovery period, the relapse, and now the next recovery. The future remains as hard to know as the past was to forecast.

German industrial production was up in March after two months that showcased severe declines; that had followed four months that had brought quite strong gains. These are statistics from the original post-virus recovery period, the relapse, and now the next recovery. The future remains as hard to know as the past was to forecast.

An isolated strong output gain

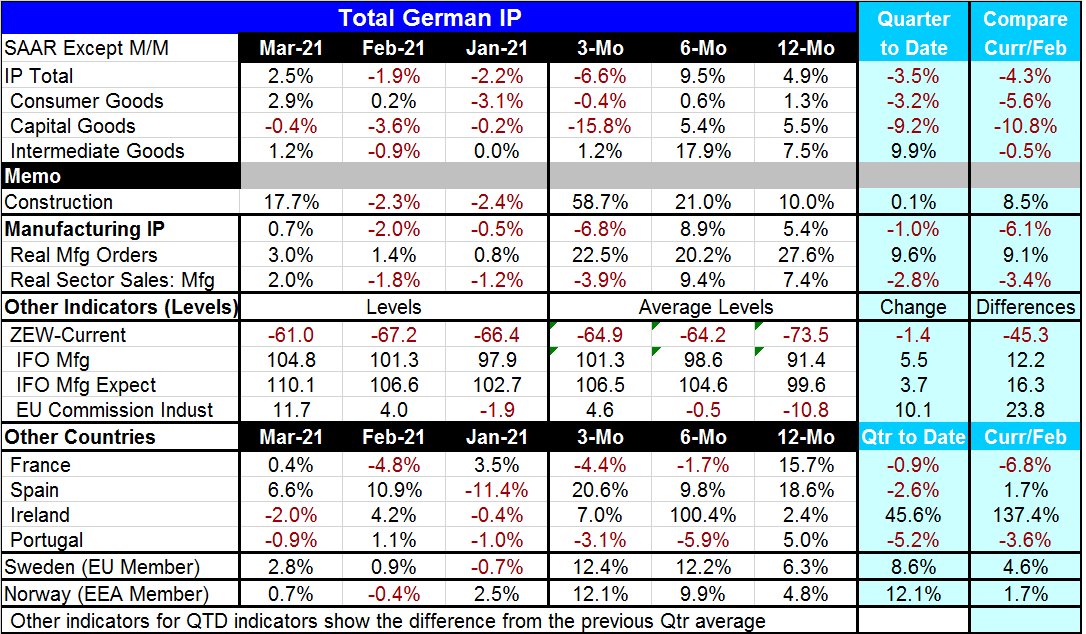

The strong output gain in March of 2.5% is not enough to turn the three-month growth rate positive (it is in fact -6.6% annualized); it is not enough to boost the quarter-to-date change to a positive result (it is -3.5% annualized). And industrial output compared to February of last year after this hot-and-cold behavior is still lower by 4.3% overall.

Manufacturing struggles

Manufacturing output overall and by sector has no clear trend. It is not ramping up the way real manufacturing orders are, for example. Orders are out there running hot well ahead of trends in output. Output trends are either mixed by sector or contracting.

Surveys

In terms of other economic surveys and gauges, the ZEW overall gauge is still a net negative reading and it has not improved by much. The IFO manufacturing gauge shows ongoing progress but in very measured steps; the same is true of IFO manufacturing expectations. The EU commission industrial index shows somewhat stronger steps and gains from 12-months to six-months to three-month with a further large step made monthly in March.

Virus distortion

For the time being, the virus seems to be still playing with the trends. Expectations and orders economic survey series, gauges for things that are really untethered formally to current activity are the sorts of indicators where we see the most ‘strength’. Where there are feet on the ground, the responses are generally more muted.

Beyond Germany

At the bottom of the table results for four EMU members are shown as well as for two other European economies Sweden and Norway. Three of these six show quarter-to-date declines in output and all three of the negatives come from EMU members (France, Spain and Portugal). However, over three months, three countries show double-digit (annualized) growth rates – one of these is an EMU country (Spain); Portugal and France still show output declines over three months. France and Portugal show output declines over three months and six months. And among this group of six, only France and Portugal have output below its February 2020 level in March. The EMU has been held back.

Summing up

These data are less upbeat than the recent economic observations for the U.S. where the virus has met with relatively more vaccination. Europe not only has had less vaccination and more outbreaks but because of the low vaccination rate it remains more at risk looking ahead. Still, vaccination rates are improving and that is a good background. But I think the chaos playing out in India after what had seemed to be a benign first wave of infection has put many more people on notice if not on edge. This not a virus we know so much as a virus that continues to surprise us in many unpleasant and threatening ways.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief