Global| Dec 07 2016

Global| Dec 07 2016German IP Rises - A Mixed to Weak View from the Rest of Europe

Summary

Germany's industrial production has come through another period of relative turbulence. IP rose by 3.0% in August, fell by 1.6% in September, and expanded by a modest 0.3% in October. The upshot of these turbulent rates of growth is a [...]

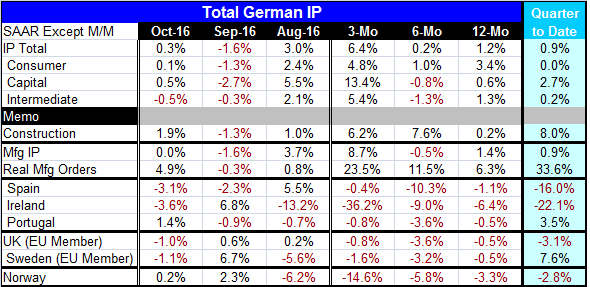

Germany's industrial production has come through another period of relative turbulence. IP rose by 3.0% in August, fell by 1.6% in September, and expanded by a modest 0.3% in October. The upshot of these turbulent rates of growth is a three-month growth rate of 6.4% annualized and a 0.2% gain over six months at an annual rate. The gain from 12 months ago is a modest 1.2%. There is much more volatility in these data than there is acceleration. German IP appears to be still expanding. Three-month growth rates are strong mostly for the same reason as the headline itself is strong: an outsized rise in August that dominates the drop in September followed by a modest October. Still, over six months all three sectors show modest or declining growth and over 12 months only consumer goods output is 'strong.'

Germany's industrial production has come through another period of relative turbulence. IP rose by 3.0% in August, fell by 1.6% in September, and expanded by a modest 0.3% in October. The upshot of these turbulent rates of growth is a three-month growth rate of 6.4% annualized and a 0.2% gain over six months at an annual rate. The gain from 12 months ago is a modest 1.2%. There is much more volatility in these data than there is acceleration. German IP appears to be still expanding. Three-month growth rates are strong mostly for the same reason as the headline itself is strong: an outsized rise in August that dominates the drop in September followed by a modest October. Still, over six months all three sectors show modest or declining growth and over 12 months only consumer goods output is 'strong.'

The pattern of growth rates helps to depress the calculation for growth in Q4. The strong August gain is the middle month of Q2 putting the September decline into the third month of Q3 so that the October gain comes from a recessed position within Q3 and leaves the level of IP at a weak position early in Q4 compared to the Q3 average. Overall IP growth is up at less than a 1% pace in the quarter to date in Q4 as a result of this timing. There is weakness in consumer goods where output is flat and in intermediate goods where output rises at just a 0.2% annual rate.

Still, German construction output is strong and real manufacturing orders are extremely strong underpinning the sector and the outlook.

Early-reporting Europe

Other European countries that have reported IP early are showing mixed-to-much-weaker results. The patterns for IP in the rest of Europe do not exhibit the patterns ingrained in German overall IP and sector trends. That means there is likely nothing regional or weather-related to explain the German results. Spain and Ireland show IP sharply lower in October while milder losses are suffered in the U.K. and Sweden. Portugal shows a solid gain after two months of IP declines and in Norway output ticks higher on the month. It's not an impressive scorecard for growth. Moreover growth rates for all six of these countries show declines over three-month, six-month and 12-month. However, only Ireland and Norway (an oil producer) show troubling declines that steadily are accelerating. The unexpected drop in U.K. output this month has an oil story as oil sector maintenance dropped output in that sector. If you are an oil producer with prices low, it is a good time to do some maintenance.

Summing up

On balance, German growth is pushing ahead and seems like it will maintain solid momentum based on the order-flow in the pipeline. Yesterdays' German order data revealed that the growth in orders was from outside countries of the European Monetary Union. Today, we find trends in IP among fellow European countries are and have been weak. The solid-portrayal of German IP and trends is not a harbinger for most early-reporting European countries. Recent PMI data have showed some improvement in European data. PMI data are up-to-date through November; today we have October industrial output reports. Still, the PMI 'indicators' and many of the actual industrial sector output reports seem to be at odds with one another. It may be too soon to brand Europe as out of the woods.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief