Global| Aug 08 2016

Global| Aug 08 2016German IP Rebounds But Drops in Quarter

Summary

The chart and table offer a pretty good perspective on German industrial trends. Overall German industrial production is still struggling. Despite a strong gain in June, it still leaves industrial output net lower over two months and [...]

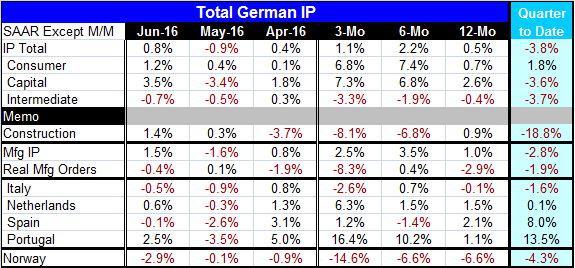

The chart and table offer a pretty good perspective on German industrial trends. Overall German industrial production is still struggling. Despite a strong gain in June, it still leaves industrial output net lower over two months and falling in the just-completed second quarter. Year-on-year trends (see Chart) show deteriorating trends for intermediate and consumer goods output but with capital goods reviving. Capital goods remain the brightest spot in IP with consistent gains in place even over one year. Intermediate goods show declines in output on all horizons and with overall deepening drops. Consumer goods output has built momentum, but it is still weak over 12 months with a gain of less than 1%.

The chart and table offer a pretty good perspective on German industrial trends. Overall German industrial production is still struggling. Despite a strong gain in June, it still leaves industrial output net lower over two months and falling in the just-completed second quarter. Year-on-year trends (see Chart) show deteriorating trends for intermediate and consumer goods output but with capital goods reviving. Capital goods remain the brightest spot in IP with consistent gains in place even over one year. Intermediate goods show declines in output on all horizons and with overall deepening drops. Consumer goods output has built momentum, but it is still weak over 12 months with a gain of less than 1%.

Construction has picked up with a very strong 1.4% rise in June, but in the wake of a 3.7% plunge in April, construction output is still collapsing over three months and down at nearly a 20% annual rate in Q2.

Manufacturing orders do not brighten the picture for German prospects either. Orders are lower in two of the most recent three months and are falling at a 1.9% pace in Q2 and at an 8.3% annual rate pace over the last three months. It's hard to tell too bright of a story from this set of data. Germany appears to be growing but not prospering and taking nothing for granted.

Other European countries reporting IP through June are Italy, the Netherlands, Spain, Portugal and Norway. Only the Dutch and Portuguese have output rising in June although over three months Spain joins them with output rising as well.

The Dutch and Portuguese show steady and accelerating growth progressing from 12-month to six- month to three-month. Spain's output on this sequence of dates is moderate and oscillating between up and down. Italy shows a year-on-year drop as well as a current month drop and drop over three months as well as in the second quarter as a whole. Norway shows output declines on all horizons with a worsening trend to boot. Not all Europeans are on the same page when it comes to the industrial sector.

These data seem to make the case that the ECB has been arguing, that global growth risks remain. In a weekend exchange, Jens Weidmann held that there is no reason for any change in ECB policy because the Brexit risk has been so well handled by markets. But in an ECB statement, the point is made that Brexit aside there is still weak global growth and risk. The Bundesbank seems again to be flexing its muscle to oppose any more ECB easing. Meanwhile, recent stress tests have highlighted the problems at Italian banks and with the new `bail-in' rules that is certainly a policy conundrum for Italy and for the ECB and policy in general.

Germany seems ready to pack up the stimulus game and prepared for the onset of normalcy despite its own uneven progress. Is that really the road we are on? Or is the Bundesbank being a bit pre-mature with its drive to invoke normalcy? This will bear watching.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief