Global| Apr 07 2020

Global| Apr 07 2020German IP Moves Higher But What Happens Next Is Another Matter

Summary

We are clearly in a mode of watching numbers and waiting for another shoe to drop. Data through February for the most part are still normal economic data with the usual monthly ebb and flow of trend. There is even a touch of rebound [...]

We are clearly in a mode of watching numbers and waiting for another shoe to drop. Data through February for the most part are still normal economic data with the usual monthly ebb and flow of trend. There is even a touch of rebound in February in many reports; the German IP report is one of those.

We are clearly in a mode of watching numbers and waiting for another shoe to drop. Data through February for the most part are still normal economic data with the usual monthly ebb and flow of trend. There is even a touch of rebound in February in many reports; the German IP report is one of those.

Still, Germany has several challenges ahead as does the rest of the global economy. The Federation of German Industry (BDI) has warned of the risk of a sharp decline in GDP. BDI warns that GDP is likely to fall 3% to 6% this year if economic activity is interrupted for a maximum of six weeks. BDI anticipates a 3% fall in global GDP, faster than the 1.7% drop in 2009.

In the meantime look for the monthly reports to come in, knowing that when topical reports finally do come in for the period of the lock-down, the assessments of current activity are going to shrivel up. So we look at the incoming reports more as the pulse of the economy and less to try to discern the trend since we know what the future will hold for the next month or so.

German IP shows some revival

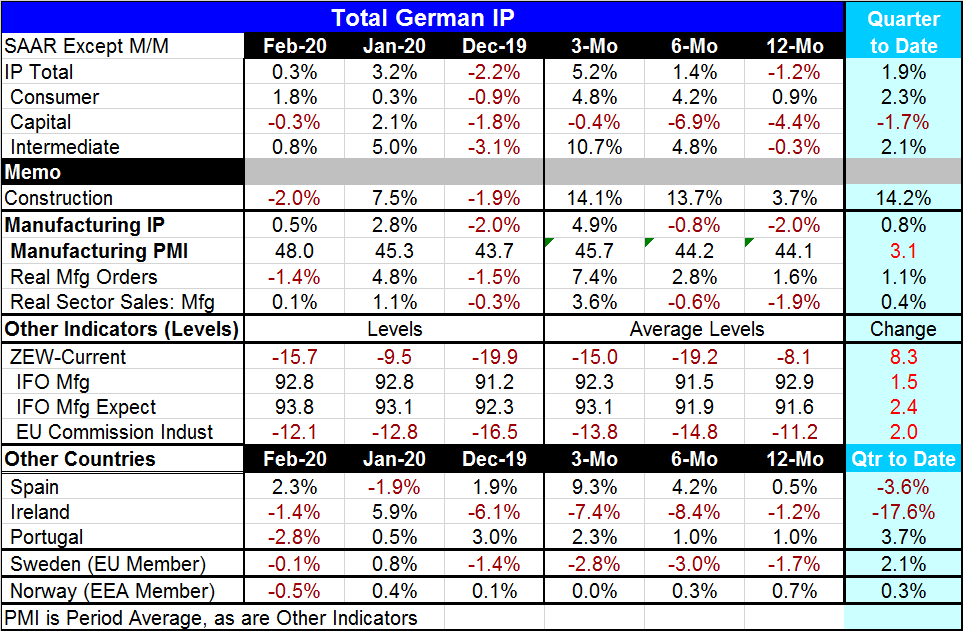

The German IP report does establish some revival in output and even acceleration for overall output from three-months to six-months to 12-months. Manufacturing IP echoes that result. All three major sectors also show some sense of ongoing improvement over the past year, but even so capital goods output continues to fall on all three timelines. Consumer goods output has been firm to strong over three months and six months. Intermediate goods output has moved up sharply. It does not matter. There is still a brick wall in the future.

Real manufacturing orders and important leading indicators have continued to rise and accelerate and real sector sales retuned to growth over the recent three months. Still, both of those series have slowed considerably in February compared to their January results. The usual harbingers are no more.

The Brick Wall: March indicators are grim

The indicators through February have been mixed with only the ZEW index showing a sharply degraded picture. The ZEW gauge is up-to-date through March and its March reading has fallen very sharply for current conditions as well as expectations. The IFO gauge also is available for March; it points to a sharp decline in current conditions and a sharp reduction in expectations. Similarly, the March reading on the EU Commission indexes showed striking March weakness in Germany and weakness spread across the expanse of Europe. Winter is coming…

There is really no chance that the improved trend in German output means anything at all since it is about to get snuffed out. And even with these early looks at surveys, we do not have a clear picture of how much output eventually will drop.

Economists in Wonderland...

Economists usually are forecasting growth and we look for signs of a shift in trends or in a variable that importantly affects other variables. We know a lot about economic and market interactions. But in this case, activity is being stopped in its tracks by a government policy to stop the economy in its tracks. The reason is to stop the spread of the coronavirus. The approach that is endorsed is curtailing social interaction on a very broad front allowing only essential services and workers to carry on. Such an approach will reduce not just growth but the levels of activity in many sectors and these are such striking reductions that they are outside of the realm of usual economic analysis.

Mitigating the Mitigators

While policy globally has been set to do this in Germany and most countries, there are also mitigation policies to mitigate the impact of virus mitigation on the economy itself. The objective of the government and central bank programs is not to boost economic activity since policy is to curtail economic interactions and activity but to support people and businesses while this curtailment is in progress. It is tricky business for stimulus and it is far outside of the scope of what governments have tried to do in the past.

The delicate endgame

Despite a great deal of intervention by central banks and fiscal spending by governments, growth is slowing and no one is quite sure how the recovery phase will eventually progress. China is progressing to unlock Wuhan as new infections in China, we are told, have stopped. Spain, Germany and Austria have been hoping that they were past the worst and are planning to begin to ease restrictions. But, just today, both Germany and Spain logged an increase in infections. Restarting growth will be tricky business. WHO is warning countries not to try to normalize too-fully or too-fast.

How do you handicap recovery from a manmade recession?

So the downturn is the result of an artificially induced program and apparently the recovery will be artificial and controlled as well. The recession is expected to be extremely severe and yet it is hoped that the economic fabric remains intact. There is no way to know because despite all the monies being spent it is hard to make everyone whole. It is also impossible to control consumer confidence. Once scared by the virus and made to hang out in some sort of containment, how quickly will or should normal activity resume? How confident will people be? How quickly will they go back to activities currently deemed too dangerous – even simple things like meeting a group or friends, playing sports, going to the movies or going out to eat? How fully will these things recover? And how quickly? No one knows. And no one knows how fully firms will remain locked in globalized businesses now that globalization seems to be more risky.

What does the pandemic mean for globalism?

Should we trust China in the future? Has it told us the truth about everything that happened there? Is it telling us the truth about its numbers now? What will this mean for globalization? Does it put Mers and Sars in a different perspective? Were we lucky to escape them so easily? And is China’s health system and food chain to be suspect in the future? China had a food supply problem and a bout of avian flu and African swine fever that caused it to decimate –slaughter- its hog population. COVID-19 is hardly a unique event except for the way it spread and across humans. China’s pigs already have been slaughtered. The lesson here is to act fast. But how do you fight something you cannot see and that spreads asymptomatically? Is it possible to take any practical lesson away from this except how at risk we will be if it happens again? We are lucky that COVID-19 preyed most effectively on a relatively small group, the old and the sick (those with preexisting conditions). It was not lethal to most of the population. Of course, even with its restricted lethal streak, it has managed to be quite a killer. So what do we fear next and how do we change our activity to prevent this in the future?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief