Global| May 07 2020

Global| May 07 2020German IP Makes Largest Drop Under Reunification; All of Europe Is Also Under Pressure

Summary

Germany's industrial production fell by 9.2% in March after a 0.3% gain in February. Sequential growth rates are falling across all sectors and decelerating from 12-months to six-months to three-months. In the just completed quarter, [...]

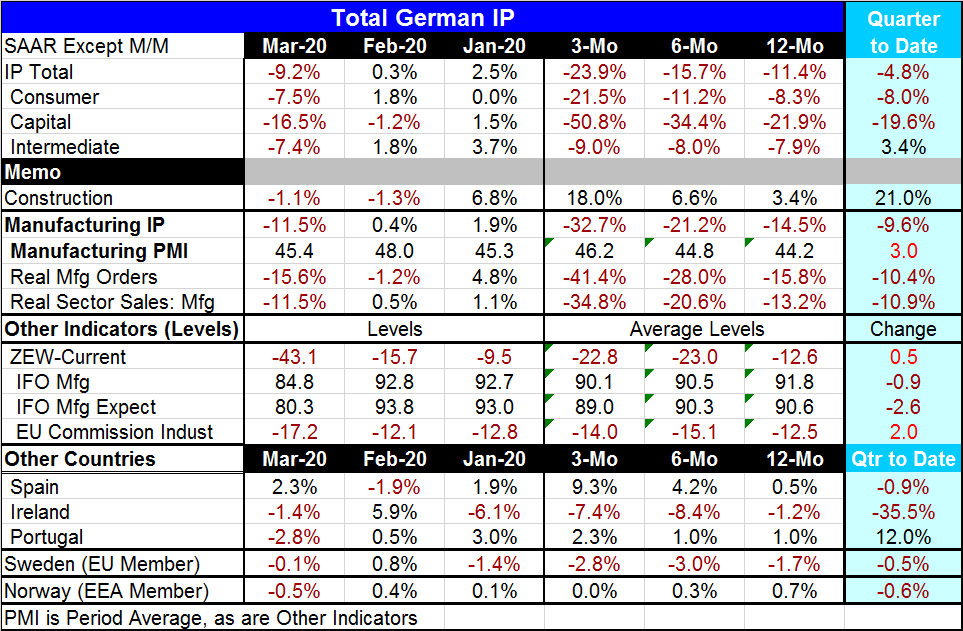

Germany's industrial production fell by 9.2% in March after a 0.3% gain in February. Sequential growth rates are falling across all sectors and decelerating from 12-months to six-months to three-months. In the just completed quarter, output is falling at a 4.8% annual rate. Output is falling fastest in the quarter for capital goods at a 19.6% annual rate. Consumer goods output is falling at an 8% annual rate. Intermediate goods output is rising at a 3.4% annual rate.

Germany's industrial production fell by 9.2% in March after a 0.3% gain in February. Sequential growth rates are falling across all sectors and decelerating from 12-months to six-months to three-months. In the just completed quarter, output is falling at a 4.8% annual rate. Output is falling fastest in the quarter for capital goods at a 19.6% annual rate. Consumer goods output is falling at an 8% annual rate. Intermediate goods output is rising at a 3.4% annual rate.

In March, output fell by 9.2% led by a drop in capital goods. Consumer goods output fell by 7.5% with intermediate goods output falling by 7.4%. March conditions are extremely weak and the weakness is unrelenting.

Construction output fell by 1.1% in March after falling by 1.3% in February. Those declines came on the heels of a strong 6.8% gain in January. As a result, construction output is still accelerating from 12-months to six-months to three-months. That's what data trends say, but that is not where the sector is headed as the monthly data show.

Real manufacturing orders are pulling back as are inflation-adjusted manufacturing sales. The declines are getting progressively greater over shorter periods as is the case with output. The entire manufacturing scene is collapsing. German domestic statistics are weak across the board, the ZEW index and the IFO current and expectations indices are weak and falling.

The table contains other early reporting European countries, among the five only Spain is seeing an increase in output in March; Spain is also seeing output accelerate from 12-months to six-months to three-months. Portugal's industrial output falls by 2.8% in March but is accelerating and holding a higher pace of growth from 12-months to six-months to three-months. Ireland and Sweden are being hit the hardest. Norway is showing withering output gains. Norway's central bank just cut rates to zero in a policy move made today.

The reaction to the virus will determine the future

Coronavirus is impacting growth across the region. Even as the numbers are getting worse, countries are starting to back-out of the lockdown. Maybe the worst of it is over; maybe the worst is not quite over. The second quarter is expected to generate the worst-looking economic numbers for most countries, but that will vary. Dealing with the virus is not yet over and not the same everywhere. The lingering effects are still going to be in play as output drops have been substantial and recovery rates are going to be muted. This puts a huge burden on governments to make payments to those who are impacted for an extended period.

The virus has come and swept through Europe, Asia and the North America so swiftly that nations used the knee jerk strategy of sheltering populations in a lockdown to try to prevent the virus from overwhelming medical facilities. These stop-gap measures have left countries without long-term protection against a reinfection. And a cycle of reinfection is the sort of thing that epidemiologists say is normal for this type of pandemic. That means what even if countries are able to make the current situation a bottom and to craft a lasting of slow recovery they will still not be out of the woods. By year end or sooner, the virus could be back. In fact, for now it is very hard to know if there is a path out of these woods without a vaccine. Work on a vaccine is going full tilt, but effort is no guarantee of success. At some point, economies may simply be forced to deal with the reality of the risk to life that the virus imposes and move on to acquire ‘herd' immunity and put the threat behind them for good.

So far, only Sweden has chosen this path. Later if there is a reflux of the virus Sweden is going to be in better shape than anyone else because it will have acquired herd immunity and it will not suffer the same sorts of viral outbreaks as will other countries that have tried to suppress infection rates. But the path from now until whenever ‘then' is, will still be quite treacherous.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief