Global| Nov 06 2015

Global| Nov 06 2015German IP Makes A Second Consecutive Drop

Summary

German IP drops for the second consecutive month in September. That pairs with a string of declines in real manufacturing orders to create a poor performance in September and a weak outlook ahead. This is not what the ECB had wanted [...]

German IP drops for the second consecutive month in September. That pairs with a string of declines in real manufacturing orders to create a poor performance in September and a weak outlook ahead. This is not what the ECB had wanted to see has it has prepared for another round of QE.

German IP drops for the second consecutive month in September. That pairs with a string of declines in real manufacturing orders to create a poor performance in September and a weak outlook ahead. This is not what the ECB had wanted to see has it has prepared for another round of QE.

Germany is hurting because of things that money policy will not be able to fix. Two key German export markets Russia, and more importantly China, have been ruined, one by sanctions and the other by a slowing economy and a tilt away from conspicuous consumption stemming from a witch-hunt for graft. Germany is also under the dark cloud of coming actions against its most important corporation, Volkswagen. And Volkswagen has just admitted that its environmental cheating was even more widespread than previously was known. It extended to non-diesel vehicles and tampering with reported CO2 emissions.

In an unrelated development, but one also in the auto sector, Japan's Takata is seeing its earnings and stock price plunge as automakers may shift away for its troubled airbag product. Micro problems can become macro issues if the company is large enough. Takata probably isn't. But Volkswagen is.

The Trends

German orders point to further slowing ahead with the weakness lodged in its foreign orders.

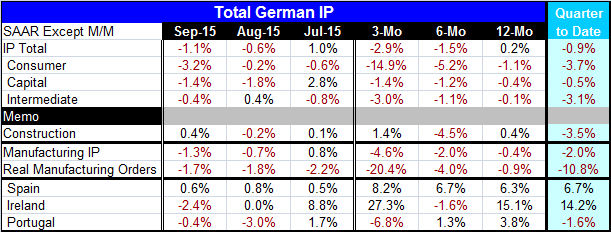

However, German IP is falling at a 2.9% annual rate and the sequential slowing is in a clear consistent deterioration from 12-month to six-month to three-month. Consumer goods IP is slowing especially rapidly with a -15% pace of decline over three months and a -1.1% drop over 12 months. Even the vaunted core of German strength, capital goods, shows IP falling at a 1.4% annual rate over three months and by 0.4% over 12 months.

The German quarter-to-date calculations for the just completed third quarter show declines up and down the line with the headline, showing a -0.9% rate of decline and plenty of weakness in the pipeline to affect next quarter. The current month is already showing a 10 rate of decline compared to the Q3 average for IP. That will make a weak starting point for October output.

Germany's construction sector showed a rise in output in September and a three-month gain at a 1.4% pace. But even the construction sector is showing a drop in output at a 3.5% annualized rate in Q3.

All of manufacturing shows IP falling at a 2% annual rate. Real manufacturing orders are also falling, at a strong 10.8% annualized rate in Q3.

In EMU

Few EMU economies report IP this early. Spain showed an IP increase in September and a pattern of accelerating output gains. Spain, the fourth largest EMU economy, shows output is up at a 6.7% annual rate in the third quarter. Ireland and Portugal show output declines in September while Ireland shows a strong three-month gain and Portugal shows a sizeable decline. In the third quarter, Ireland's IP is up at a 14.2% annual rate and Portugal's is falling at a 1.6% annual rate.

Summary and Outlook

The German industrial performance is disappointing. The reason for this weakness is structural meaning that there is little in the way of German and EMU macroeconomic fiddling that can affect it. If the ECB does pursue more QE, there will be a nearly zero impact on Germany. Even if the QE impacts the euro, as it surely will drive it even lower, German exports are not suffering from price competiveness issues; weak and shifted global growth are the problems.

This is an unequivocally bad piece of news for Germany and for Europe. It suggests that weakness in Europe is going to be that much harder to erase. ECB President Mario Draghi may celebrate for one brief moment the stronger U.S. employment report for October and the prospect of a December Fed rate hike which will drive the euro even lower and further improve European competitiveness. But that path for the euro has not had much to show for it in terms of stimulated growth. The news from Germany, the largest economy in the EMU, will swamp the news from the U.S. Germany's situation will have much more pronounced impact on the EMU than the goings on in the U.S. economy. At the end of the day, it's every man for himself. That's what happens when the ship is sinking. And that is the risk that Europe is facing and with too few tools to address the risk.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief