Global| Jun 08 2021

Global| Jun 08 2021German IP Logs Massive 12-Month Gain But Eases Month-to-Month

Summary

Germany's industrial production fell by 1% in April, dropping for the third time in four months. IP is lower over three months for Germany overall and for each manufacturing sector. Over six months German IP is making a gain, but that [...]

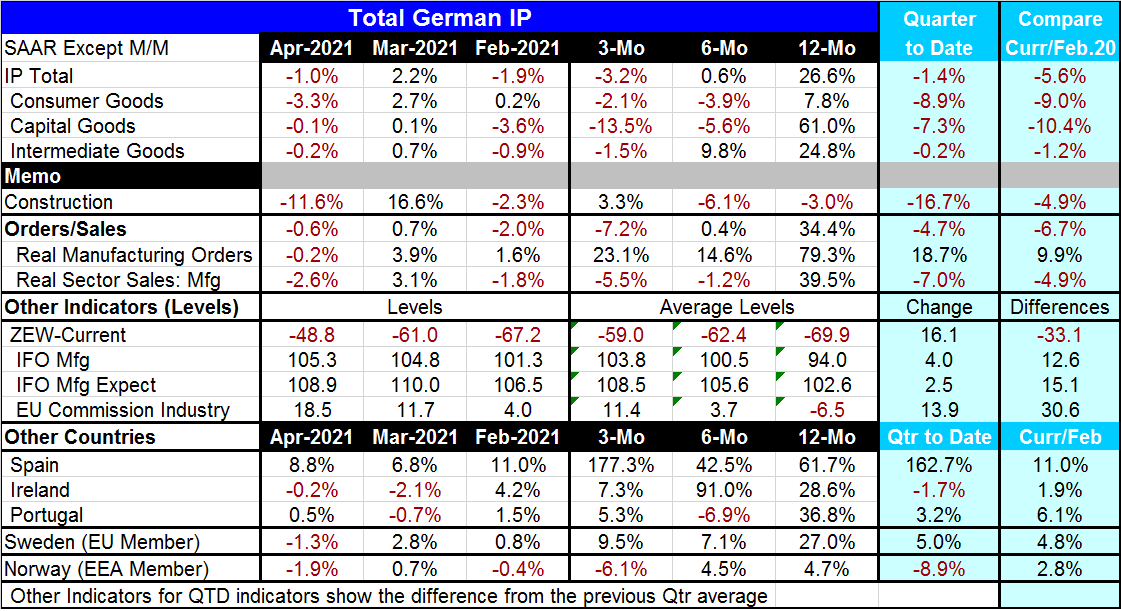

Germany's industrial production fell by 1% in April, dropping for the third time in four months. IP is lower over three months for Germany overall and for each manufacturing sector. Over six months German IP is making a gain, but that is all on the back of intermediate goods as consumer and capital goods output both are weaker over six months. Over 12 months output is extremely strong, rising from that 12-month ago crater caused by the onset of Covid-19. Capital goods output is up by 61% over 12 months. Consumer goods output is up by a relatively moderate 7.8%.

Germany's industrial production fell by 1% in April, dropping for the third time in four months. IP is lower over three months for Germany overall and for each manufacturing sector. Over six months German IP is making a gain, but that is all on the back of intermediate goods as consumer and capital goods output both are weaker over six months. Over 12 months output is extremely strong, rising from that 12-month ago crater caused by the onset of Covid-19. Capital goods output is up by 61% over 12 months. Consumer goods output is up by a relatively moderate 7.8%.

We have been hearing a lot about ‘base effects' from the central banks that have warned that 12-month inflation is going to look higher because prices were so restrained a year ago. That same effect applies to output and we see it in action here. As you can plainly, output fell in April; yet, the year-on-year gain is massive. Last month the year-on-year change was -3.7%. Clearly the IP gain is being driven by the change in the base, not by current economic circumstances.

The quarter-to-date changes show that output is in fact in a weak patch. In Q1- very early in Q1- the change in output over the Q1 base shows a decline is under way. But then we are only one-month into the new quarter so the reading is not very robust. Still, the message is that growth is floundering a bit here. Overall output is down at a 1.4% pace in the new quarter, while consumer goods and capital goods performance is even weaker. The overall result is held up by the tiny setback in the output of intermediate goods.

The construction sector has a slightly different pattern. It too shows a decline in the current month and is declining in the quarter-to-date, but its sequential growth rates from 12-months to six-months to three-months are different than for manufacturing.

The final column of the table takes us from February 2020 to date. On that span, manufacturing IP overall as well as for all the sectors is lower and construction output is also lower. Despite the fact that there has been real strength in the PMI indexes for manufacturing, we see that actual manufacturing output is lagging its pre-Covid-19 levels. This jibes with the German real orders and sales data that showed increases in real orders but lagging behavior in real sales (see order and real sector sales trends in the panel below the IP summaries). Orders do not face real world constraints. Sales and production do. Similarly, PMI data only address the breadth of output in a sector or industry and not its strength. It is good to bear in the mind that despite some really heated up PMI readings manufacturing is still not back to its pre-Covid-19 levels of output. And that is a very strong counterpoint to the eyepopping year-on-year growth rate that is posted this month.

The next step down in the table is to other indicators and these are based on industry surveys and in some cases diffusion indexes. Month-to-month three of these four readings get stronger. IFO manufacturing expectations is the exception. However, each of those four statistics: ZEW current, IFO Mfg, IFO Mfg expectations and the EU Commission Industry gauge, shows stronger values in April that for its respective Q1 average. And all except the ZEW current index are higher than their respective levels in February 2020. The indicators point more strongly ahead than do the actual output trends.

Five other European countries (three of them EMU members) show IP results at the bottom of the table. Three of the five show output drops in April; Spain and Portugal log increases in April output. However, over three months, six months and 12 months, these countries show a preponderance of output increases. Of the fifteen growth metrics (five countries on three horizons), only two show fleeting negative values. These five countries show a lot of forward momentum. In the quarter-to-date, only Ireland and Norway show any output declines. Meanwhile, compared to February 2020, all five show output increases in train as of April. That is impressive- German weakness aside.

Obviously, what policymakers and workers are most interested in is what is really happening as well as what is going to happen next. That makes the IP statistics and real sector sales data kings of the data heap. But indicators may be more sensitive and may be pointing ahead to coming trends. So in the end all data signals matter we just have to vet them properly. The trends in productions show Germany as a laggard but five other European countries are having real output expansion even in the face of some output setbacks in April. And for Germany, orders data point to strength ahead, mitigating some of the weak signal from the IP trend itself. Indicators are generally stronger than IP data and point to more strength ahead. All in all, the data survey for the month puts a more realistic spin on economic performance than just the headlines. This comprehensive survey of similar reports reveals some of the nuances of the unfolding recovery. The April output decline does not look so worrisome and the year-on-year output gain has its own air of fantasy. In between those two observations, the truth seems to be that the expansion is in progress. Germany seems to be struggling more than some of its European counterparts. But that probably has a lot to do with the data comparisons put into the mix by the uneven impact of the virus on economic activity over the past year and a quarter. On balance, the manufacturing push still seems to have a lot of momentum and room to run.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief