Global| Aug 07 2013

Global| Aug 07 2013German IP Jumps After Stumble

Summary

Germany: an export-led growth spurt in action- As go capital goods, so goes Germany. German industrial orders have been increasing and showing that the greater part of their increase is coming from the foreign sector. Germany has long [...]

Germany: an export-led growth spurt in action- As go capital goods, so goes Germany. German industrial orders have been increasing and showing that the greater part of their increase is coming from the foreign sector. Germany has long been an economy that, while the 'strong man' of Europe is also a strong man that seems to need steroid infusions from the surrounding area (good thing the national sport is soccer, not baseball). Germany has a certain symbiosis with the rest of Europe. It is not a strong economy that originates its own growth through domestic demand and then spreads the wealth of domestic demand to the rest of Europe invigorating the region with growth. Rather Germany acquires demand from outside of the country and satisfies it with domestic output, boosting its economy and contributing to the growth of its surrounding EMU countries only through second or third round effects. If this were only a domestic mechanism we would call it 'trickle down' economics.

Germany: an export-led growth spurt in action- As go capital goods, so goes Germany. German industrial orders have been increasing and showing that the greater part of their increase is coming from the foreign sector. Germany has long been an economy that, while the 'strong man' of Europe is also a strong man that seems to need steroid infusions from the surrounding area (good thing the national sport is soccer, not baseball). Germany has a certain symbiosis with the rest of Europe. It is not a strong economy that originates its own growth through domestic demand and then spreads the wealth of domestic demand to the rest of Europe invigorating the region with growth. Rather Germany acquires demand from outside of the country and satisfies it with domestic output, boosting its economy and contributing to the growth of its surrounding EMU countries only through second or third round effects. If this were only a domestic mechanism we would call it 'trickle down' economics.

What we are seeing in Germany now is a typical example of a German economic expansion. Foreign orders are beginning to lead the way for increases in German output. German output is being led by the expansion of production of capital goods with intermediate goods being pulled up on their heels and consumer goods trading along behind them.

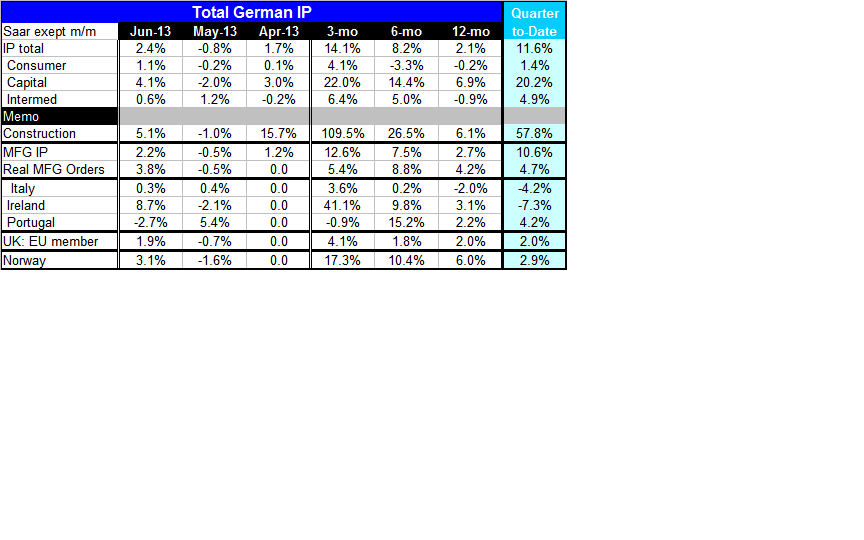

Month-to-month- In June, overall German industrial production rose by 2.4% month-to-month reversing a 0.8% decline in May. Capital goods output increased by 4.1%, consumer goods output increased by 1.1%, while intermediate goods output increased by 0.6%.

Over three-months, and more- Over three months, industrial production is up at a 14.1% annual rate and is accelerating from 8.2% over six months and from 2.1% over 12 months. That is a very clear very stark profile of production acceleration. In the just-completed second quarter, industrial production is up at an 11.6% annual rate over the first quarter.

Sectors by pecking order- The sectors trends show that the greatest growth and acceleration is in capital goods, followed by intermediate goods with consumer goods trailing these trends. Capital goods output is up at a 22% annual rate over three months exceedingly its six-month rate of 14.4% and it's twelve-month pace of nearly 7%. Intermediate goods is up over three-months at a 6.4% annual rate, ahead of its 5% annual rate over six-months as both of these reverse the 0.9% drop in intermediate goods production still has on the books for its year-over-year change. Consumer goods output is up at a 4.1% annual rate over three-months, reversing a 3.3% annually drop over six-months and a 0.2% decline of over 12 months. The German capital goods locomotive is pulling the intermediate goods, and consumer goods sectors into a stronger growth profile. In the quarter to date capital goods output is up 20% over Q1 intermediate goods output is up 4.9% over Q1 while consumer goods output is up 1.4% over Q1.

Construction sector booms- While the recent PMI metric from Markit for July found the German construction sector slowing, it remained in expanding territory. Industrial output for the construction sector in June saw output up strongly 5.1% in the month; the sectors absolutely exploding faster than Mr. Creosote in a Monte Python sketch, ballooning over three-months with a 109% annual rate of growth up from a 26% annual rate over six months in a 6% annual rate over 12 months. Some of this is a bounce back from activity that was held back because of widespread flooding across parts of Germany earlier in the year.

A typically German recovery- In the just completed second quarter, manufacturing output is up at a 10.6% annual rate, ahead of the 4.7% annual rate for real manufacturing orders. Both orders and output are pointing higher. The orders data show that much of the strength (not detailed here) comes from increases in demand from beyond German borders, while the domestic output data reinforce the fact that the German capital goods sector is getting back in gear. This configuration of events is as typically German as a beer garden, sauerkraut and Oktoberfest.

Beyond the German rebound...Also reporting industrial production results early are Italy, Ireland, Portugal, the United Kingdom and Norway. The details are in the table. Each of these countries - except Portugal- is showing the same progressive increase in growth rates over more recent periods (output acceleration). This trend reinforces the notion that recovery in Europe is beginning to take hold - and that it spreading. The unfortunate exception to this trend is Portugal although there may be a timing problem. Portugal has a very strong growth rate over six-months but output has a declining growth rate over three-months and yet its recent strength has been enough to give it the highest growth rate in the recently completed second quarter (compared to Q1) among this group of countries at 4.2% in Q2. Still, its recent profile is somewhat shaky and Portugal, you recall, is a country that is supposed to be the poster child for austerity having toed the line more carefully than any other member that was put under its yoke. The real test for Portugal may come in the coming months when we will see if economic revival helps Portugal to expand in a better, more balanced way, with more budget control than the countries that were less willing to bite the bitter bullet of austerity.

Europe is turning the corner-but not on two wheels- For now the data point to an expanding Europe. And we are starting to see more articles being written on the theme of an expanding Europe. Given the data and the turnaround that we earlier chronicled in global manufacturing PMI trends, some optimism seems appropriate. However, many the rivalries and much of the discord within the monetary union is still in play; some key countries -- most notably France -- never did adopt the austerity that promised to put them on a stronger economic growth path. And so, we want to watch as Europe begins to recover to see which countries have the most balanced and sustainable progress. However, it's not clear that Europe has achieved escape velocity from its recession and so we need also to continue to monitor its ongoing recovery for sustainability as well as for the composition of growth among member country economies.

Forward-guidance takes root like an out-of-control international monetary weed- Separately we have the Bank of England adopting as UK monetary policy the notion of forward guidance following in the troubled footsteps of the Federal Reserve.

Troubled footsteps? I have been, and continue to be, critical of forward-guidance as a monetary policy. If you do not know where you're going and you plug numbers into a GPS machine, it cannot tell you where to go either unless it knows the location. Similarly central banks do not have the most accurate forecasting record. They really don't know where their respective economies are going. The Federal Reserve completely and totally missed forecasting the last recession -- and it was not alone in this misadventure. Yet, it would have us believe that it can provide what it wants us to think, on one hand, is a 'guaranteed' interest-rate path, but what it admits 'on the other hand' is its expectation (or is now its VIEW?). And, is that a 'view' that will change and a policy path that will diverge from guidance if/when the future is different? I believe it is! So what is it about forward-guidance that is anything new? Harry Truman once said that he wanted a one-armed economist so the guy couldn't say, 'but on the other hand...' Now the Fed is offering up as cutting-edge economics what we used to think of as Harry Truman's nightmare. And the Fed has suckered into the program both the BOE and the ECB.

Hubris at the central bank- How is central banking guidance any different from Harry Truman's nightmare, except that the central bankers would have us believe that their best case is the right one? What if it isn't? Then where will their forward guidance have gotten us?

What to expect when you're expecting forward-guidance- I would say that the next thing we look for from the Bank of England is more trouble in its communication policy. When a central bank adopts a policy that has duplicity at its core, that central bank will begin to have a problem expressing to the public exactly what its policy is. The strange policy of forward guidance is one of the reasons that the Federal Reserve is having such a difficult time with communication. At the core of this problem is that fact that the Fed BELIEVES in forward-guidance and does not see the duplicity inherent in the program! And, once you understand that the Fed's stated policy is to be transparent, you understand why it has such a difficult time articulating what it is doing to the public.

The Fed as an example- In the case of the Fed, the situation is made a little bit worse by the fact that several Federal Reserve members really don't find its notion of forward guidance satisfying, want to terminate the program of quantitative easing, and are not at all on the same page as the Fed majority whose views get represented more heavily in the Fed statements with some language modified to take into account the protestations of the dissenters- to keep them at bay.

And the ECB's experience? But, rest assured, the adoption of a policy of forward-guidance by the BOE can only lead to trouble. When Mario Draghi tried to implement it for the ECB, the Bundesbank's Jens Weidmann quickly clarified the ECB position by saying that forward-guidance would not keep interest rates low if policy called for an interest-rate hike. That about says it all, in a nutshell. The value of forward-guidance in keeping rates lower than they otherwise would be is zero (zero, zilch, nada). The contribution to creating certainty and to making future interest rates closer to the 'central bank's guidance' is speculative at best. Forward-guidance should be relabeled as forward-misguidance because it is trying to get us to focus on policies from the central bank that link the future to the forecast from the central bank that may prove to be wrong. How is that construed as progress in either the world of economics or in the world of central banking? And why do so many central banks want to build their policy on such a shaky foundation? is this an attempt to introduce central planning through the back door? It seems like a policy more appropriate for Russia or China to me.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief