Global| Mar 11 2019

Global| Mar 11 2019German IP Is Much Weaker Than IP for Most of Europe

Summary

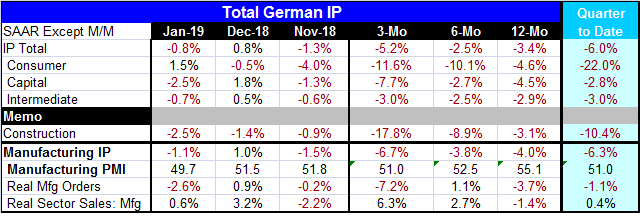

Germany shows a 0.8% drop in industrial production (-1.1% for manufacturing) in January. It shows declines over three months, six months and 12 months at rates of decline that are getting progressively larger. Output for German [...]

Germany shows a 0.8% drop in industrial production (-1.1% for manufacturing) in January. It shows declines over three months, six months and 12 months at rates of decline that are getting progressively larger. Output for German consumer goods and capital goods both follow that same prescription with sequential declines getting progressively larger. For intermediate goods output also declines on all those horizons, but the declines are steadier and cluster around a pace of -2.5% to -3% and do not show an inclination to get larger.

Germany shows a 0.8% drop in industrial production (-1.1% for manufacturing) in January. It shows declines over three months, six months and 12 months at rates of decline that are getting progressively larger. Output for German consumer goods and capital goods both follow that same prescription with sequential declines getting progressively larger. For intermediate goods output also declines on all those horizons, but the declines are steadier and cluster around a pace of -2.5% to -3% and do not show an inclination to get larger.

German construction output also follows the same progressively deteriorating pattern as the headline for IP. While manufacturing orders also have been weak, the weakness in output appears to be a steadier ongoing erosion. However, real manufacturing orders are falling by 3.7% over 12 months and at a -7.2% annualized pace over three months.

However, German real sales have the opposite pattern and have been gaining momentum. Real sector sales are falling by 1.4% over 12 months, then rising at a 2.7% pace over six months and gaining at a 6.3% annual rate over three months. That is a slightly confusing development. There is also an inconsistency between Germany's manufacturing PMI that took some time to fall below 50 and register the output decline that IP has been showing for some months. The IP result shows manufacturing falling by 4% year-over-year.

Germany's MFG PMI falls below 50 in January and February

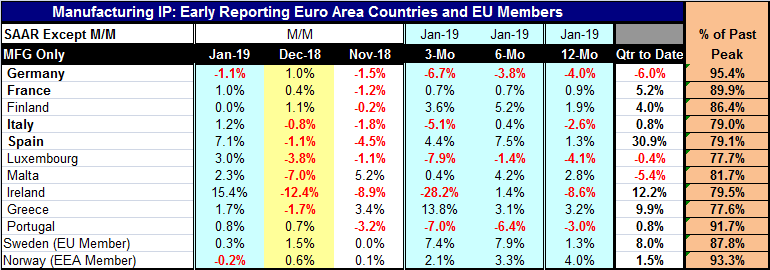

Germany is Europe's largest single economy and it is highly dependent on international trade. Much of that trade never leaves the EU customs union and much of it has no exchange rate consequences being intra-EMU trade as well. And for the time being, at least the rest of Europe is doing much better than Germany, at least in terms of momentum. Industrial output is falling in Germany and it is the only drop recorded in January among 10-EMU economics and one of only two drops among 12 European economies (Norway is the other).

However, over three months, five of 10 EMU economies show IP declines in progress. Three show declines over six months and five show declines over 12 months. But in the quarter–to-date only Germany, Malta and Luxembourg show output declines. Output trends looked considerably more dicey in December when six EMU members posted IP declines but with the recovery in January, Germany, Luxembourg and Portugal have the clearest deteriorating profiles. However, France is still weak with output growth on all horizons but also growing at an annualized rate of less than 1% on all horizons. Italy shows a sharp drop in output over three months and shows output lower over 12 months, but it manages to log a gain over six months. Ireland also interrupts a series of 12-month and three-month IP drops with a gain over six months.

As those comparisons show that there is not a lot of strength in Europe viewed country by country, but Germany and Portugal are the only sizeable economies with serious contractions in play. Still, France remains listless and Italy shows a severe decline in the last three months. It would not take much to turn on weak signals across Europe, but the point for now is that January did not do that. January pushed things in a more positive direction.

Manufacturing IP in Germany, despite its ongoing decline, still has the highest ratio to past peak (95%) IP of any EMU country- and of any country in the table. France is at 89%; Italy is at 79% along with Spain. Despite the sharp and ongoing weakening, Germany's IP is still at an elevated operating rate there.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief