Global| Mar 08 2017

Global| Mar 08 2017German IP Holds to Expansion Path

Summary

German IP advanced in January despite Germany having reports a very sharp decline in new orders yesterday. Of course, orders and output are connected with more than a one-month lag. But output is showing signs of fatigue. The IP gain [...]

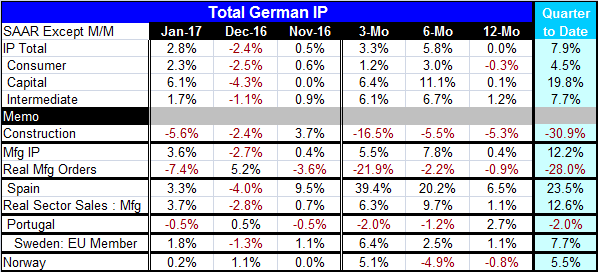

German IP advanced in January despite Germany having reports a very sharp decline in new orders yesterday. Of course, orders and output are connected with more than a one-month lag. But output is showing signs of fatigue. The IP gain of 2.8% in January is on the heels of a 2.4% drop in December. That leaves the three-month growth rate below the six-month growth rate and puts the 12-month pace at unchanged. Manufacturing output has the same sort of six-month to three-month deceleration in its growth rate but with a small 0.4% gain over 12 months.

German IP advanced in January despite Germany having reports a very sharp decline in new orders yesterday. Of course, orders and output are connected with more than a one-month lag. But output is showing signs of fatigue. The IP gain of 2.8% in January is on the heels of a 2.4% drop in December. That leaves the three-month growth rate below the six-month growth rate and puts the 12-month pace at unchanged. Manufacturing output has the same sort of six-month to three-month deceleration in its growth rate but with a small 0.4% gain over 12 months.

Construction and the quarter-to-date

Construction output, often an artifact of weather in Germany this time of year, has two substantial declines in a row and shows an accelerating contractive trend from 12-month to six-month to three-month. Construction is down at a 30% annual rate in the new quarter (annualized) but overall output is up at a solid 8% pace early in Q1 and manufacturing IP is even better, logging a 12.2% gain.

Sectors

German sector output trends mirror the recent up/down path of the headline. For all sectors, three-month growth cools relative to six-month growth and all have modest gains or a slight loss over 12 months. German output trends are not impressive.

Early data reporters

There are some early reporters of industrial production in Europe. Among them, Spain, Sweden and Norway have output increases in January while Portugal logs a decline. Over three months, all but Portugal have output increases on the books. Spain shows a slowdown in real manufacturing output from six-month to three-month while Sweden and Norway show a pick-up and Portugal's output decline deepens. Three-month growth rates are better than year-on-year growth rates everywhere but Portugal. Portugal, despite output declines over six months and three months, has the strongest gain over 12 months in this group at 2.7%. Spain's real manufacturing output is up by just 1.1% over 12 months, Sweden's output is up by 1.1% and Norwegian output is lower on balance over 12 months. In the unfolding quarter-to-date, these countries exhibit mixed trends. Only one month into the new quarter, it is hard to pin anything down at any rate. The 'early reporting' group has no consensus at this development.

The shadow doesn't know

These reports taken together with the German result suggest that output is still advancing but not very strongly. Of course, all industrial reports will be in the shadow of the deep drop in German industrial orders until we get more perspective on that.

Globally speaking

In a more global framework, China reported a huge increase in imports in January while its exports were weak. It also reported its first deficit in three years. Wow! That 'Trump trade magic' works fast doesn't it? Japan logged a current account surplus but also posted a trade deficit. Yesterday, the U.S. logged a larger deficit as exports were mixed but weak outside of commodities with imports gathering clear strength outside of oil and agriculture goods. None of this really sets the international picture in any firm way. The OECD opted to not change its global outlook for growth rates just this past week. But seeing strong imports in China and a revival in U.S. demand constitutes two important trends if they are able to hold up. Taken on their own, the European industrial reports have tended to be more mixed against a backdrop that has been clearly strengthening in the PMI gauges for manufacturing and services. We continue to look to see if these different types of reports are going to line up with one another. At this point they do not, adding to the outlook confusion.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief