Global| Jul 07 2015

Global| Jul 07 2015German IP, Flat in May, Still Shows Upturn

Summary

Germany's industrial production was flat in May, but it still carries momentum from the gains in earlier months. Still, the sequential growth rates show deceleration in overall output mostly due to decelerating output of intermediate [...]

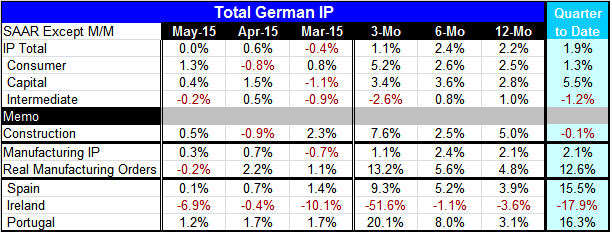

Germany's industrial production was flat in May, but it still carries momentum from the gains in earlier months. Still, the sequential growth rates show deceleration in overall output mostly due to decelerating output of intermediate goods. Consumer goods output shows sequential acceleration and capital goods output, while not sequentially accelerating, has stepped up its growth over three months and six months compared to 12 months. The construction sector is also accelerating.

Germany's industrial production was flat in May, but it still carries momentum from the gains in earlier months. Still, the sequential growth rates show deceleration in overall output mostly due to decelerating output of intermediate goods. Consumer goods output shows sequential acceleration and capital goods output, while not sequentially accelerating, has stepped up its growth over three months and six months compared to 12 months. The construction sector is also accelerating.

Real manufacturing orders do tend to presage trends in manufacturing in Germany. Germany shows sharply accelerating real orders. So far manufacturing IP is not in step, but it should pick up based on order strength and past relationships.

In the quarter to date, trends are shifting as overall IP is up at just a 1.9% pace with consumer goods output up at just a 1.3% pace. German capital goods output is up strongly in the quarter to date at a 5.5% pace. But construction output is falling at a 0.1% pace. Manufacturing overall is up at just a 2.1% pace and lagging real manufacturing orders which are very strong at a 12.6% pace and point to acceleration in IP ahead.

All of these data suggests that Germany is on the brink of much stronger IP growth as real orders are surging and output is still lagging. Orders tend to lead output in Germany by about two months.

Few EMU nations have reported IP results for May yet. However, Spain, Portugal and Ireland, not exactly a representative group, have reported. Spain and Portugal are each showing explosive growth. Spain's three-month growth rate for IP is 9.3% and Portugal's pace is 20.1%. Both have year-over-year IP growth in excess of 3% largely due to the recent spurts. Ireland struggles with IP off very sharply over three months and down by 3.6% over 12 months.

Of course, all eyes are on Greece. And negotiations today should bear fruit one way or the other. That will have a lot to do with how events play out in the coming weeks and months and even further. Some now see a renewed push to keep Greece in the euro area spearheaded by France. Accordingly some think there will be some minor sweeteners that Alex Tsipras will accept to save face. If this is true, it is not clear how he will sell the rest of the austerity obligation as a victory. Whatever is really going on behind closed doors we will know soon and it will help to pave the way for clearer thinking about the future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief