Global| Dec 09 2013

Global| Dec 09 2013German IP Drops in October

Summary

German industrial production fell by 1.2% in October, marking the second monthly drop in a row. In September IP dropped by 0.7%. German industrial output is now falling at a 1.5% annual rate over three months, faster than its 1.3% [...]

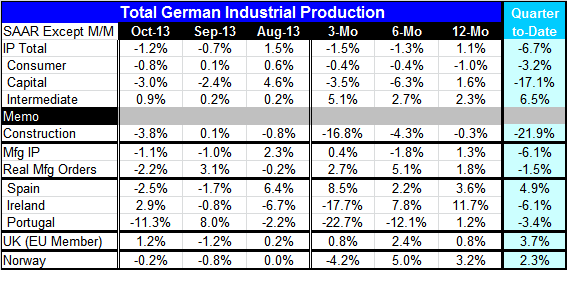

German industrial production fell by 1.2% in October, marking the second monthly drop in a row. In September IP dropped by 0.7%. German industrial output is now falling at a 1.5% annual rate over three months, faster than its 1.3% annual rate of decline over 6-months. Over 12-months IP is up at a 1.1% annual rate.

German industrial production fell by 1.2% in October, marking the second monthly drop in a row. In September IP dropped by 0.7%. German industrial output is now falling at a 1.5% annual rate over three months, faster than its 1.3% annual rate of decline over 6-months. Over 12-months IP is up at a 1.1% annual rate.

In the new quarter IP is falling at a 6.7% annual rate led by a 17.1% annual rate of decline in capital goods. The capital goods sector is usually the leading sector for German output. Consumer goods output is also falling in the quarter to date, but intermediate goods output is advancing at a 6.5% annual rate.

Manufacturing IP also fell for the second consecutive month. It is also falling sharply, at a -6.1% annual rate in the new quarter-to-date. But manufacturing IP is advancing on balance over the last three-months. It is not showing the same overall deceleration as overall IP. The output of construction sector goods is lower by a 3.8% in October alone and is dropping at a 21.9% annual rate in the quarter to date.

Other early European reporters of IP data show a mixed picture. Spain, Portugal and Norway show output declines in October while Ireland and the UK report gains. But in the quarter to date, IP is gaining in Spain, the UK and Norway. Output is declining in the quarter to date for Ireland and Portugal.

The UK shows steady if somewhat moderate output growth rates on trend. Spain shows acceleration. Ireland and Portugal show clear negative trends in play while Norway displays a decline in output over three-months that contrasts with growth rates over longer horizons.

On balance the early news on EMU concerning IP is mixed to the weak side. But industrial output can be quite volatile. The German result for October is heavily affected by weakness in the construction sector. Still German manufacturing output also is lower in September as well as October, but it has a firmer trend than does overall German IP.

The German report for October is not a major disappointment, but it is disappointing. Even stripping out the weakness in construction we are left with some considerable weakness in Germany industry.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief