Global| Sep 07 2016

Global| Sep 07 2016German IP Drops and Sets a Negative Trend

Summary

German IP dropped in July falling by 1.5%. The drop more than offsets a 1.1% gain in June and makes it two declines in the last three months. IP is falling on a consistent basis and it is nearly accelerating its drop from 12-Mo to [...]

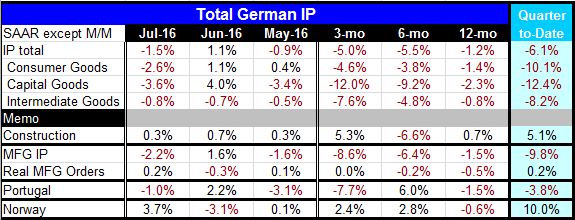

German IP dropped in July falling by 1.5%. The drop more than offsets a 1.1% gain in June and makes it two declines in the last three months.

German IP dropped in July falling by 1.5%. The drop more than offsets a 1.1% gain in June and makes it two declines in the last three months.

IP is falling on a consistent basis and it is nearly accelerating its drop from 12-Mo to 6-Mo to 3-Mo. While the drop is not accelerating for total IP it is accelerating for each of consumer goods, capital good and intermediate goods. Construction has been strong enough to keep these sectors from dictating the overall IP trend. Most disturbing is that the way lower is being led by capital goods output declines instead of being resisted by that key sector. Has global excess capacity finally come home to roost and to kill off the vaunted German capital goods sector?

Things that go bump in the night...

If you are prone to worry here are some of the things in this report to obsess over:

(1) German IP has fallen in 9 of the last 15 months

(2) German IP has fallen year-over-year in two of the last three-months

(3) Of the three main sectors (consumer goods, capital goods and intermediate goods) over the last 12 months output has fallen month-to-month on 20 of 36 possible occasions.

(4) Capital goods have become the most volatile sector by far

(5) Manufacturing output is seeing accelerating weakness

(6) Real manufacturing orders are flat or lower on all horizons but, at least they are not decelerating

(7) Overall output and all sectors are showing sharp output losses in the nascent third quarter over their Q2 base levels.

(8) There is no sign that weakness is temporary or is abating. It seems to be gaining pace.

Non-German trends to keep you awake at night...

(1) The drop below 50 for the U.S. MFG ISM

(2) Sharp drop in US ISM Non-MFG index to a 79-month low

(3) Weak Global PMI readings for manufacturing and services

(4) An unproductive kick-the-can-down-the-road G-20 meeting even with a clear whiff of protectionism in the air.

(5) Ongoing geopolitical instabilities and China's South China Sea intransigence

Hey...I could do more? German IP clearly is weak and that is a very important part the German economy. Global weakness has been swarming for months and with central banks having pulled every rabbit, bird or rodent possible out of their respective hats. Markets are losing respect for their continued protestations that they are not out of ammunition and that they could do more. If they could do more why haven't they? And why haven't they been more successful?

Why central banks fail There are at least two reasons for central bank ineptitude in this cycle: recognition and conviction. Bankers have been fooled by the degree of weakness and have convinced themselves that the steps they have taken are so huge that they have not really had their hearts in what they have done. That brings us to the second reason which is that whether we are talking of the Fed, the ECB or the BOJ there have been policy detractors. And policy detractors mix the message and blunt its effectiveness. In the US the hawks (who hate that designation) have been quick to switch and try to hike rates on thin evidence of inflation progress and have persistently tried to turn on the rate hike signal when the economy was not clearly in the required mode for rate hiking. They have been guilty of dogma and the belief that recession is followed by expansion, recovery, and inflation and they believe that the Fed has overstayed its welcome and over-cooked its stimulus. In Europe, the Germans have been permanent naysayers to more stimulative policy even delaying its implementation while waiting for policy moves to be 'legally vetted' causing policy changes to come too little or too late. Japan has simply dawdled never really seeing the strength of its headwinds and without greater weight given the oppressive effect of its high ratio of debt to GDP and shrinking population.

Faith? You 'gotta' have faith? ..and good policy too! On balance there is not much here to inspire faith. Fiscal policy is still off limits in most places for the time being. Only the BOE has powder it kept dry, then it expended a good couple of rounds on the Post Brexit UK economy whose nasty knee-jerk weak signals have since dissipated. But the UK is too small an economy to drive global growth and in any event its policy moves are meant to combat its own special weakness. All too many of the large economies are being sucked back into the black hole of economic weakness and maybe even policy despair.

Bleak trends-are they real? For now, the trends are bleak and the odds are not "ever in your favor". Perhaps the best hope is that some of this weakness will prove to be seasonal and related to a summer lull rather than to a fundamental step back. Perhaps... (which also means 'perhaps not'). But the downshifting in the US looks too severe to be caused by a summer lull. Germany and the rest of Europe have other trends that are flat or weak. China continues to fight its own demons. There is really hardly a bright spot left with the US auto sector now seemingly off peak. Will Europe's auto sector similarly run out of gas? Where will the 'kick' come from? There have been some scattered reports of better back-to-school buying in the U.S. We will keep an eye on that. Do we care if central banks actually do do more?

Even dark clouds have a silver lining...for someone One bright spot is that markets in Europe have liked the weak US data that have put the Fed back on its heels and shunted its rate-hiking ways to the back burner. Expectations for a delayed Fed rate hike have weakened the dollar, however, and that is not to Europe's advantage. Still, it is small thing. But more attention needs to be paid to the degree of weakness and the corroborating signals of weakness instead of brushing them aside and assuming revival is right around the corner. That is exactly the sort of policy hubris that has caused this extended weakness to fester. Happy day are not here again...Guess what? This time it HAS BEEN different. Now what?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief