Global| Aug 07 2019

Global| Aug 07 2019German IP Drops Again

Summary

In June, German manufacturing output declined on all fronts. Consumer goods output declined. Intermediate goods output declined. The output of capital goods declined. It makes you nostalgic for the good only days, like yesterday, when [...]

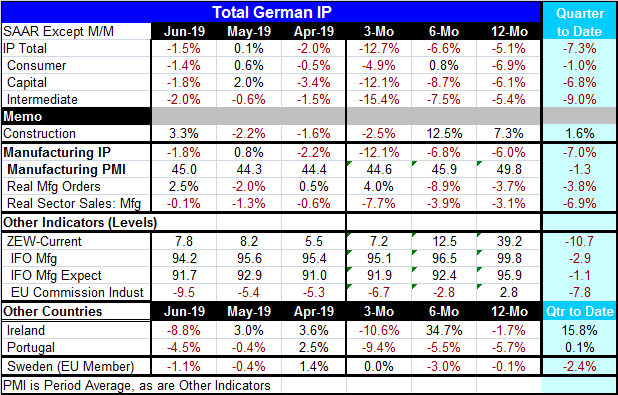

In June, German manufacturing output declined on all fronts. Consumer goods output declined. Intermediate goods output declined. The output of capital goods declined. It makes you nostalgic for the good only days, like yesterday, when something good happened to orders and foreign orders surged. But the good news was short-lived. Output is staying on its declining ways with better than a 1% decline in each sector on the month. Orders probably will not report their good news of yesterday.

In June, German manufacturing output declined on all fronts. Consumer goods output declined. Intermediate goods output declined. The output of capital goods declined. It makes you nostalgic for the good only days, like yesterday, when something good happened to orders and foreign orders surged. But the good news was short-lived. Output is staying on its declining ways with better than a 1% decline in each sector on the month. Orders probably will not report their good news of yesterday.

Sequential weakness

Output is declining overall and for all three sectors on all horizons (three-months, six–months and 12-months) with only one exception. That is that over six months consumer goods output is rising but only at a 0.8% annualized rate. It is an exception in 'sign' only and it is still weak and declining on the other horizons. In fact, for IP overall, for intermediate goods and for capital goods, there is sequential weakening of growth rates as well. The declines get more severe over the most recent periods. IP is weak and it is weakening.

Europe is slowing…and so is everyone else

Germany is slowing and Europe is slowing. Brexit is threatening. In Asia, three central banks that had been holding their 'fire' shot off rate cuts today. The central banks of New Zealand, Thailand, and India all cut rates today. India executed a 35bp rate cut. Australia reported out a sharp decline in its construction sector survey. The trade war is still raging and markets are reeling under the shock of a bullet they thought they had dodged. The ricochet has proved to be as damaging as a direct hit. In the end, China's decision to go back on its negotiating progress with the U.S. saying it could not provide the assurances it earlier had agreed to has proved to be a huge mistake that has enveloped the world in a much more hostile situation. It is China's own 'renegade' status that has caused the U.S. to seek so many safeguards in its negotiations and not just take China at its word. China is getting a lesson in what it really means to be a big player- instead of a bit –player- in the global economy. There are rights and there are responsibilities. China has only wanted the rights. Now it is learning about responsibility and rules of fair play.

The 'strong man' of Europe is on his knees

Germany shows weakness across just about all of its manufacturing or industrial measures. It shows broad-based ongoing declines in the second quarter. Ireland, Portugal and Sweden, also early IP reporters, also show output weakness and declines or flat output over three months as well as 12 months.

Macroeconomic investment

I look at this as a period of investment in the future. We are investing in the reeducation of China as to how it will have to behave in the future regardless how big it gets. There are standards for behavior and all nations must compete fairly. The U.S. is also laying down new ground rales for its trade relations with other developed nations that have been granted freer access to the U.S. market than U.S. firms have had access to their markets. The idea is to level the playing field for trade in general, not just regarding China.

The missing link

But the missing piece is still that there is no mechanism for the oversight of exchange rates and arguably it is misaligned exchange rates that were the trigger for all these trade imbalances to arise and to persist. Foreign exchange rate misalignment was behind the trade war. Fixing that remains as an extremely important problem that must be addressed and so far has only been ignored.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief