Global| Aug 07 2015

Global| Aug 07 2015German IP Drops

Summary

German industrial production dropped in June, falling by 1.4% month-to-month. Overall IP has been steadily decelerating with annualized growth rates shrinking or turning progressively to larger negative numbers as the horizon [...]

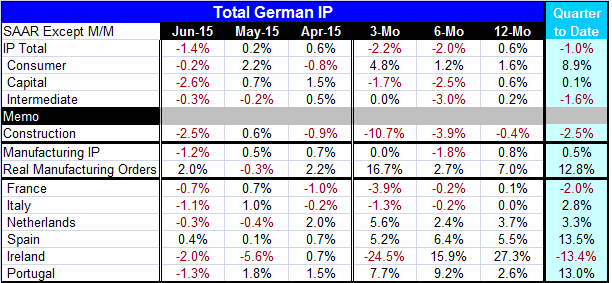

German industrial production dropped in June, falling by 1.4% month-to-month. Overall IP has been steadily decelerating with annualized growth rates shrinking or turning progressively to larger negative numbers as the horizon shortens. However, consumer goods output is in stark contrast with the rest of the report. Consumer goods output maintains positive growth across horizons of one year and less as output jumps to a growth rate of 4.8% over three months. But capital goods, the usual backbone of German industry, show negative growth rates over three months and six months. Intermediate goods contract over six months but are only flat over three months.

German industrial production dropped in June, falling by 1.4% month-to-month. Overall IP has been steadily decelerating with annualized growth rates shrinking or turning progressively to larger negative numbers as the horizon shortens. However, consumer goods output is in stark contrast with the rest of the report. Consumer goods output maintains positive growth across horizons of one year and less as output jumps to a growth rate of 4.8% over three months. But capital goods, the usual backbone of German industry, show negative growth rates over three months and six months. Intermediate goods contract over six months but are only flat over three months.

On balance, these are not the results expected from the strongest economy in the euro area.

Manufacturing output is feeble as it shrinks over six months and is flat over three months with a year-on-year rise of less than 1%. But real manufacturing orders show a sharply higher 16.7% annualized rate of growth over three months. German orders generally lead German output by one to two months. This means while the current IP results are disappointing, they should not be enduring. The German order data are generally reliable. German manufacturing orders are up by 7% over 12 months compared to output which is up by less than 1%. Orders point higher there too.

Turning to the rest of the EMU, we have mixed results. Early results are reported for France, Italy, Spain, the Netherlands, Ireland, and Portugal. Each of these countries, except Spain, showed a decline in IP in June.

However, Spain and Portugal as well as the Netherlands also show consistently strong IP growth over three months, six months and 12 months. Ireland shows strong six-month and 12- month growth, but that pulls back sharply to a 24.5% annualized contraction over three months. Italy and France, the second and third largest EMU economies, show progressively weak IP growth results.

What we see is the smaller economies (plus Spain, an austerity country and the fourth largest EMU economy) showing better results than the largest economies in the EMU. It is not clear why that is the case. In Germany's case, orders are still strong even as output has slowed. Italy is a still a struggling austerity country as well as a large EMU economy. France is struggling without formal austerity. Portugal and Spain are two austerity success stories, albeit with a long way to go.

In short, Europe continues to have some very mixed results. With Greece still undecided, there could be more financial burden in store for the larger countries in the EMU. If Greece is ejected or leaves the EMU, there will be financial losses inflicted across the EMU. This largely has not been discounted. Markets assume that Greece will get some sort of deal. Even the German finance ministry now says it prefers a bridge loan, perhaps leaving the door open for more temporary measures and/or more kicking the can down the road. Maybe Germany is done playing hardball.

In any event, Europe is once again on a bit of a weak patch and there is nothing to do about it. Well, there is always prayer.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief