Global| Nov 07 2019

Global| Nov 07 2019German IP Drop Squashes Optimism...Still the Slowdown Is Slowing

Summary

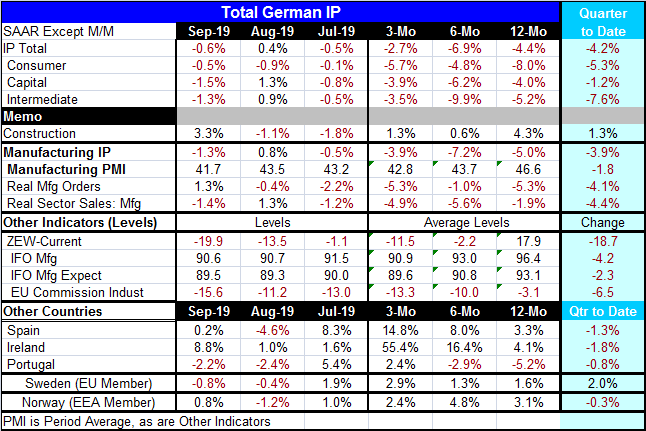

On the face of it, September was not a good month for German industrial production. Output fell by 0.6% overall, it fell by 0.5% for consumer goods, it fell by 1.5% for capital goods and it fell by 1.3% for intermediate goods. But [...]

On the face of it, September was not a good month for German industrial production. Output fell by 0.6% overall, it fell by 0.5% for consumer goods, it fell by 1.5% for capital goods and it fell by 1.3% for intermediate goods. But these declines come on the heels of an output increase in August. As a result, the annualized three-month drop in output is less than the year-on-year pace of decline and less than the annualized six-month decline. Even though output declines stepped up from 12-months to six-months, the degree of weakness has cooled over three months. These same trends play out for manufacturing and that can be seen graphically in the chart on the left. On that same chart, the manufacturing PMI from Markit (with a one month fresher observation) is still weakening while IP is in prevarication mode. Although the PMI is weakening, it also pauses making its sideways move in October instead of in September. So in some sense, both series hint at a lessening of the downward pressure despite a rather negative headline with negative across-the-board results.

Data on real sector sales released with the orders report yesterday show the trends in the graph on the right. Consumer goods and intermediate goods continue to weaken in terms of their 12-month growth, but capital goods sales have recovered from a low point late in 2018 and now are showing some actual expansion.

Sometimes the good news is buried deep in the details. And other times what appears to be passing for good news turns out not to be. So the manufacturing situation still needs to be monitored closely. Globally, manufacturing conditions remained very weak in October. And there are fresh forecast downgrades on the economic front.

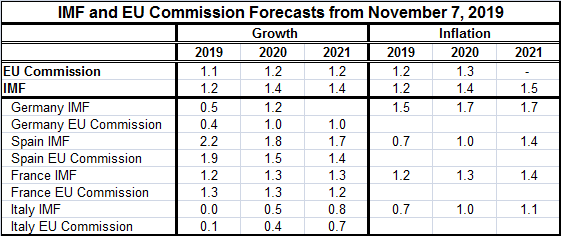

Forecast downgrades

Forecast downgrades

Both the EC and the IMF cut their projections for the euro area's growth. However, this was a bout of technical trimming since the outlook was only ‘slashed' from 1.2% to 1.1% (or from 1.3% to 1.2%) any less of a revision and it would have been invisible. You may be thinking- why bother? And since economic forecasts are not accurate to within one tenth of one percentage point, you may harbor even more cynical thoughts. But speaking as one who has been doing economic forecasting since 1977, let me point out that forecasts are forecasts but they also are signals and they serve a communications purpose. In this case, both institutions are ‘signaling' that growth conditions remain weak and that they still see risks on the downside. Had they kept the forecasts unchanged, that message would have been harder to deliver or more poorly received.

Forecast intent

These are forecasts that argue against premature policy backsliding. The EU Commission continues to see weak output and inflation remaining below its target value for the next couple of years. This is not good news to the ECB, but a weak forecast is another way to try to keep German blowback at bay. Mario Draghi is gone and Christine Lagarde has replaced him. She is fresh off her standing as head of the IMF. Even though she is a lawyer by training and more of a career politician by practice, she now has some firm economic responsibility on her resume and has moved into a position at the ECB that will test her. Will she revert to being a politician? Or will she stay on the straight and narrow and make policy ‘by the numbers?' German pressure is already evident. Lagarde has already promised that she will have a study performed look into the impact of negative rates to see how helpful they have been. Despite the ongoing under-shoot and projected under-shoot for inflation by the ECB, the Germans are more worried about the structural of policies of the ECB than they are about the fact that policy has missed its one and only policy objective, inflation at a pace of just below 2%, by a lot and for several years running. Clearly, battle lines are drawn up at the ECB. As the IMF view on Europe also includes an assessment of Italy that still did not see any pick up there. And Italian growth has been extremely weak and Italian inflation has been among the most subdued in all of the EMU (and that is expected to continue). And yet Italy is still having its feet held to the fire by the EU Commission its deficit position.

The Future...(no forecasts)

On balance, Germany remains a focal point for Europe as its largest economy with the most competitive industrial sector and the most exposure to international trade. Germany continues to struggle and it is expected to continue to struggle. Meanwhile, there is some growing optimism on the U.S.-China trade situation and perhaps a little less fear of Brexit since parliament seems to have reined in Boris Johnson. But now there are U.K. elections and there can be no certainty what the new political leadership will be in the U.K. either at the top or in Parliament.

There remains a great deal of global instability that transcends economics. Old alliances have increasingly been rethought as time has passed and put greater distance between ‘now' and the World War period when those alliances were forged. Countries look more to the future and hold ties less to the past.

Still, old alliances are still largely intact among countries with a great deal of shared values. Old allies can have disagreements about the new economic and political relationships and still remain allies. But these notions are being tested. In some places, the U.K. and Catalonia come to mind, people look for more self-determination and clearer break with the past. In Asia, the best example is, of course, Hong Kong.

Some claim that local or supranational governing units have wielded too much power and that the centralized large governmental structure is out of touch or has an agenda different from the people. This is the criticism of the elite- they do not know better than ‘us' what to do or what we need. Some even seek to break long held geopolitical claims; others have had to rule them: Hong Kong, Catalonia and the Kurds across Turkey, Syria, and Iraq come to mind. We have seen populist movements in Europe, especially in Spain, Portugal and Italy. We see countries around the globe from Europe to the U.S. to the Middle East, in Latin America and in Asia having these growing- or coming-of-age pains. This is a big broad set of events that have brought nations as well as groups of people within nations into conflict. It has spawned migrations nearly everywhere in the world as people try to change conditions where they live or give up and try to leave. Some are displaced by war, others by domestic violence related to drugs or just thuggery and the loss of order. These changes are a risk and have the potential to impact the future, the outlook, the forecasts - our reality- and should not be underestimated. No one should think that changing forecasts for growth by a tenth of a percentage point is a measure of the degree of change we may face. Nor does that serve as a ‘communication' of that risk.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief