Global| Feb 07 2020

Global| Feb 07 2020German IP Continues to Stumble And Fall

Summary

Germany's industrial production fell 3.5% in December. There are declines in December in consumer goods, capital goods and intermediate goods. Construction spending was lower in December. Manufacturing IP in December fell 2.9%. The [...]

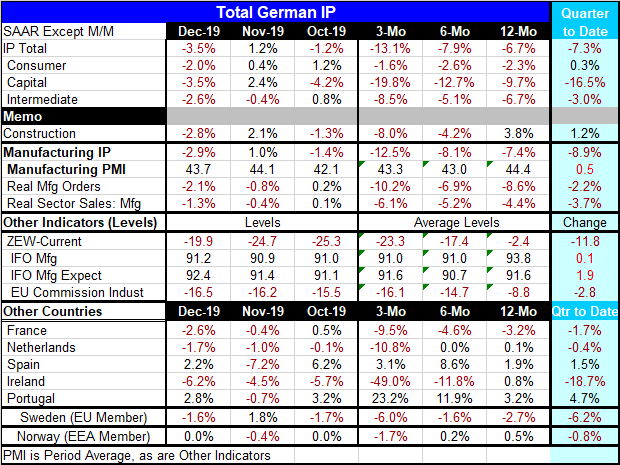

Germany's industrial production fell 3.5% in December. There are declines in December in consumer goods, capital goods and intermediate goods. Construction spending was lower in December. Manufacturing IP in December fell 2.9%. The German manufacturing PMI remained below 50 and slid to a lower level in December. Both real manufacturing orders and sales fell. These readings are very clear...crystal clear. The indicators for December show some month-to-month improvement. But the traditional hard core real-count data as opposed to diffusion type surveys are unambiguously weakening in December.

Germany's industrial production fell 3.5% in December. There are declines in December in consumer goods, capital goods and intermediate goods. Construction spending was lower in December. Manufacturing IP in December fell 2.9%. The German manufacturing PMI remained below 50 and slid to a lower level in December. Both real manufacturing orders and sales fell. These readings are very clear...crystal clear. The indicators for December show some month-to-month improvement. But the traditional hard core real-count data as opposed to diffusion type surveys are unambiguously weakening in December.

IP and all sectors decline

German IP is not just declining, but its pace of decline is accelerating from -6.7% over 12 months to -7.9% over six months to -13.1% over three months. Sequential growth rates are negative across all three sectors and for all three-time horizons in the table. Capital goods output shows the clearest ongoing and deteriorating weakness with deceleration as its main marker. Output declines for consumer goods are shallower and not deteriorating at a quickening pace as they are for capital goods. Intermediate goods output is declining at a faster pace over three months than it does over 12 months, but its six-month pace is not quite in line with marking it as a steady deceleration; still the growth progression shows uneven worsening.

Indicators

The indicators based on diffusion surveys generally show less deterioration and some month-to-month improvement in December. The EU Commission reading is an exception. But the ZEW current, the IFO current manufacturing gauge and the IFO expectations manufacturing gauge each show improvement month-to-month. The ZEW current and IFO manufacturing expectations indexes also show some slight improvements from October to November and gain from November to December. But considered more broadly, the sequential progression from 12-months to six-months to three-months generally shows deterioration is the rule even according to survey data.

Quarter-to-date

For the quarter-to-date (QTD) – the statistic now refers to the completed Q4- total IP is falling at a 7.3% annual rate with construction up at a 1.2% pace and manufacturing falling at an 8.9% annualized rate. Capital goods is the weakest sector, declining at a 16.5% annual rate followed by a 3% pace of decline for intermediate goods. Consumer goods output is actually rising but at a very feeble 0.3% annual rate in the quarter. On a QTD basis, the manufacturing PMI actually increases slightly.

Summing up

The impact on output across the early reporting Europe is mixed but with a lot of weakness mixed in. The weakness in Germany is fully consistent with weakness in real orders and in real sector sales. As 2019 drew to a close, the German economy had a struggling manufacturing sector. The road ahead will not get any easier in 2020 as the global economy is challenged by the impact of the coronavirus.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief