Global| Dec 07 2020

Global| Dec 07 2020German IP Continues to Snap Back

Summary

Germany's industrial production gained 3.2% in October after a 2.3% rise in September to put together two strong months of results. Sequential growth rates show IP up at very strong rates of change over both three months and six [...]

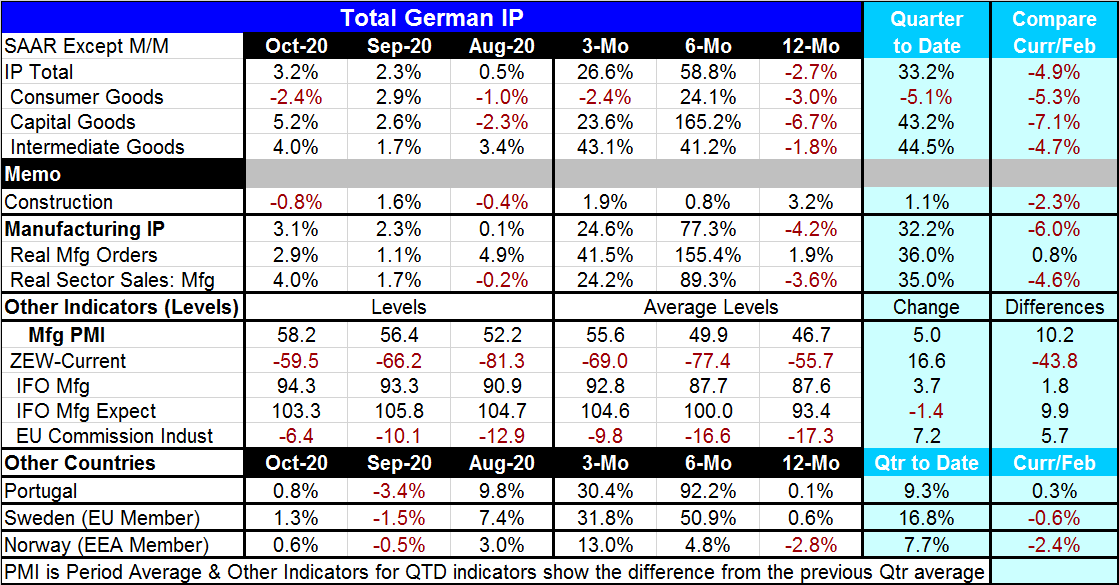

Germany's industrial production gained 3.2% in October after a 2.3% rise in September to put together two strong months of results. Sequential growth rates show IP up at very strong rates of change over both three months and six months but lower on balance over 12 months. Compared to February just before the Covid-19 shutdowns swept through Europe, IP is lower by 4.9% (as are all main sectors). What is clear is that IP is still recovering. It has not gained all that it last since the virus struck. And growth in the just unfolding fourth quarter is extremely strong.

Germany's industrial production gained 3.2% in October after a 2.3% rise in September to put together two strong months of results. Sequential growth rates show IP up at very strong rates of change over both three months and six months but lower on balance over 12 months. Compared to February just before the Covid-19 shutdowns swept through Europe, IP is lower by 4.9% (as are all main sectors). What is clear is that IP is still recovering. It has not gained all that it last since the virus struck. And growth in the just unfolding fourth quarter is extremely strong.

In the quarter-to-date, the consumer sector is showing output curtailment while capital goods output is coming on strong. Intermediate goods output has been posting steady and strong increases over the past three months. Construction output, however, has been spotty; it pulled back in October.

Manufacturing drives the IP result and it shows the same general patterns as IP overall. Orders and real sector sales both improved, strengthening for two months in a row further cementing a positive signal.

Other manufacturing surveys also underscore the manufacturing revival. The Markit manufacturing PMI continues to show steady gain through October. However, we also know that in November same PMI will make a sharp pull back as a new round of covid-19-containing closures was set in motion in Germany and across Europe. Since the PMI data are a bit more timely, we know where this is headed next month despite the strong trends through October.

The ZEW current reading has a negative disposition, but it has been steadily improving. The IFO reading is also improving but improving more slowly. IFO manufacturing expectations were set back in October. Meanwhile, the EU Commission index for industry is climbing back to stronger readings.

On balance, the various industrial indicators show the same picture, but that is only as far as things go this month. We are set for a setback in November and then we except another recovery since we are living in ‘real time' in December and we can see from this vantage point that some of the restrictions are being taken off and plans are in place to remove more in Germany as well as across Europe. The U.S. is behind Europe in this phase of the cycle with its infection rates still peaking.

We can't ever take any economic trend to the bank because the virus, if it emerges, trumps even the strongest trend. But what these various surveys all agree on is that when the Covid-19 restrictions are taken off the economy does rebound, and so far, it has rebounded strongly. With vaccines getting ready for deployment, this should be an encouraging finding even though it is no guarantee about how soon or how fast conditions can return to something that is more normal. The virus has done economic damage, but the global economy remains resilient.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief