Global| Sep 19 2006

Global| Sep 19 2006German Investors and Analysts Confident of the Present but Wary of the Future

Summary

More German investors and analysts participating in the ZEW surveys continue to attest to improved economic conditions, but have grave doubts concerning economic conditions six months ahead. The balance between those saying current [...]

More German investors and analysts participating in the ZEW surveys continue to attest to improved economic conditions, but have grave doubts concerning economic conditions six months ahead.

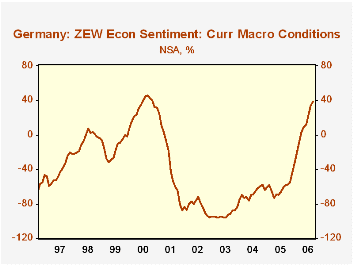

The balance between those saying current conditions were improving and those saying current conditions were deteriorating rose from 33.6% in August to 38.9% in September and was 92.0 percentage points above the -58.1% of September, 2005. It has only been since April of this year that more people believed that current conditions were improving than those who believed they were deteriorating. The current balance is close to the most recent peak of 45.8% in September, 2000 as can be seen n the first chart.

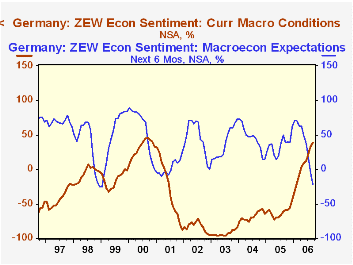

While feeling better about the current situation, the participants in the September ZEW survey have become decidedly more wary about the future. The balance between optimists and pessimists went from -5.6% in August to -22.2% in September and was 60.8 percentage points lower than that of September, 2005 when the balance favored the optimists to the extent of 38.6%. The sharp decline in sentiment is probably a reflection of the increasing probability of a slowdown in the United States economy and hence a reduced demand for German exports, plus the likely negative effect on consumer spending with the three point scheduled increase on January 1, 2007 of the VAT, and the uncertainty of other reforms. The contrast between opinions of current conditions and the future are shown in the second chart.

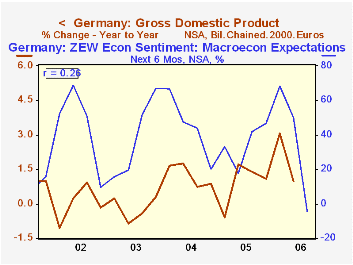

While the ZEW measure of expectations has often been an indicator of the future trend of the economy, it has not been a particularly good indicator of the magnitude of change in the economy. In the third chart we show the quarterly values of the expectations balances and the year to year change in real, seasonally unadjusted Gross National Product. As can be seen, there is only a small correlation (0.26) between the expectations balances and the year to year change in GDP. Moreover, the R2 suggests that only 6.76% of the change in the year to year GDP is accounted for by the expectations balance.

| Germany ZEW Survey | Sep 06 | Aug 06 | Sep 05 | M/M dif | Y/Y dif | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|---|

| Balance on Current Situation (%) | 38.9 | 33.6 | -58.1 | 5.3 | 92.0 | -34.8 | 44.6 | 38.4 |

| Balance on Situation Six Months Ahead (%) | -22.2 | -5.6 | 38.6 | -16.6 | -60.8 | 34.8 | 44.6 | 38.4 |

More Economy in Brief