Global| Jul 11 2014

Global| Jul 11 2014German Inflation Remains Very Tempered

Summary

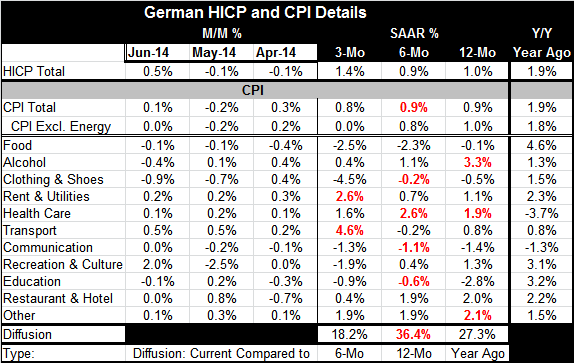

Germany's harmonized index of consumer prices advanced by 0.5% in June after falling in April and May. With June's HICP increase, the three-month annualized inflation rate is up to 1.4%, which is higher than the 0.9% pace over six [...]

Germany's harmonized index of consumer prices advanced by 0.5% in June after falling in April and May. With June's HICP increase, the three-month annualized inflation rate is up to 1.4%, which is higher than the 0.9% pace over six months and the 1% pace over 12 months. Still, inflation in Germany is low and a popup of inflation over three months is hardly a reversal of the long period of weak inflation in Germany. The chart shows that inflation is still locked in a long downtrend; it also shows that Germany's domestic CPI excluding energy is falling sharply in recent months.

Germany's harmonized index of consumer prices advanced by 0.5% in June after falling in April and May. With June's HICP increase, the three-month annualized inflation rate is up to 1.4%, which is higher than the 0.9% pace over six months and the 1% pace over 12 months. Still, inflation in Germany is low and a popup of inflation over three months is hardly a reversal of the long period of weak inflation in Germany. The chart shows that inflation is still locked in a long downtrend; it also shows that Germany's domestic CPI excluding energy is falling sharply in recent months.

The table shows the array of prices by eleven categories for Germany's domestic CPI report. The domestic CPI rose by only 0.1% in June with the CPI excluding energy flat on the month. The trends for this price index show inflation locked in at rates just below 1% over intervals of three months, six months and 12 months with the CPI ex-energy at 1% over 12 months, 0.8% over six months and flat over three months. The flatter profile for Germany's domestic CPI is just another way of making us wary about the acceleration that is being shown over three months in the HICP treatment of inflation.

We can create a diffusion index of inflation from the 11 categories presented in the table. That index is presented at the bottom of the table. This diffusion index compares inflation over three months to six months, inflation over six months to 12 months, and inflation over 12 months to that of one year ago. The diffusion index tells proportion of industries where inflation is increasing. Over three months, inflation is only increasing in 18% of these categories. Over six months, it's increasing in only 36% of the categories and over one year, inflation is increasing in only 27% of the categories compared with inflation of one year ago. Clearly, the look at German inflation from the individual category standpoint tells us that there is no widespread increase in prices going on. In fact, in the German detailed treatment over three months, only two categories showed acceleration compared to the previous six months.

There are number of events in the euro area that could cause wariness over continuing price weakness. In yesterday's report, we chronicled the widespread declines in industrial production that are in train across the euro area. We know that a number of other indicators have weakened too, including Germany's Ifo and ZEW indexes. Yesterday there was concern about a Portuguese bank; those concerns rattled markets in Europe extending their negative impact to trading on the United States stock exchanges. Taken together, these indicators should be taken as warning signals. However, on the day, Ewald Nowotny, President of the National Bank of Austria and ECB Governing Council member, has assured us that everything is fine in the euro area and that we need to give time for the ECB credit stimulus program to work.

Nowotny may be right. However, I think that the ECB should also be wary that it may not have done enough. The EMU-wide diffusion indices on manufacturing and services are giving us weak signals and the weakness in industrial production is a real phenomenon. If that is ongoing, the environment for lending is going to deteriorate. Even a program geared to try to stimulate lending will have a hard time being successful as activity cools. Moreover, Portugal is not the only country that has banking sector problems. Europe is quite aware that its banks are week. In fact, many have protested the proposed increase in BIS capital standards.

This is still a very difficult time for the world economy. China is still going through its transitions and its economy is uneven. Japan is trying to pull itself out of its torpor of deflation. But at the same time, Japan has increased its sales tax and that has set growth back. The United States and Europe are making progress in recovery; in both cases, progress is very uneven. Neither the US nor Europe have experienced anything like the normal economic recovery that they would expect after period of downturn. Financial markets are flying high, driven by the stimulus of highly excessive monetary accommodation. We can't take that performance as a forecast of expected good future events. Indeed, largely because financial institutions were so badly burned by their lending escapades in the last business cycle, even with cheap money lending is not picking up. Prices remain very subdued as the after-effects from the economic downturn continue to weigh on income trends, unemployment levels, and growth. In this environment, I would hope that policymakers would be more attentive to a clustering of negative information rather than dismissive of it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.