Global| Nov 11 2016

Global| Nov 11 2016German Inflation Picks Up; Is It for Real?

Summary

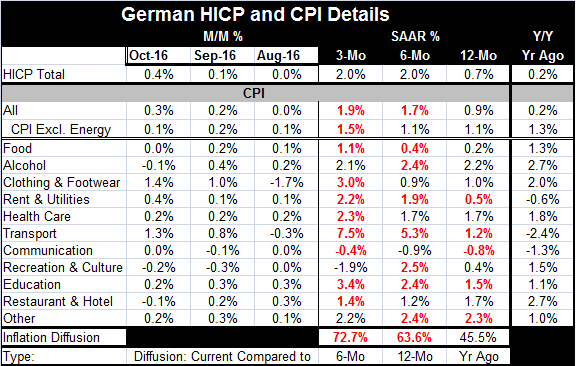

The graph (on the left) is most useful for the discussion of whether inflation's rise is 'real' or not. The graph clearly shows that Germany's headline inflation is surging, rising from the ashes of declines to log an advance of 0.9% [...]

The graph (on the left) is most useful for the discussion of whether inflation's rise is 'real' or not. The graph clearly shows that Germany's headline inflation is surging, rising from the ashes of declines to log an advance of 0.9% year-over-year (0.7% for the HICP). This surge is a stunning turnaround from just nine months ago when the price level was still falling year-over-year.

The graph (on the left) is most useful for the discussion of whether inflation's rise is 'real' or not. The graph clearly shows that Germany's headline inflation is surging, rising from the ashes of declines to log an advance of 0.9% year-over-year (0.7% for the HICP). This surge is a stunning turnaround from just nine months ago when the price level was still falling year-over-year.

Distortion vs. trend

We always have known that the headline drop was distorted by the drop in oil prices. Central bankers themselves have told us this repeatedly. In fact, the companion plot to the headline CPI is the CPI excluding energy; it tells a wholly different story of an inflation rate that has been hovering below the pace of 1.5% and is now decelerating even in the face of the bump up in oil prices. In short, there is not much evidence here that inflation is really spreading its wings. The headline measure is showing more clearly the immediate impact of oil prices. Even though inflation rates are rising on a broad front across commodity groups (from 12-month to six-month to three-month), the aggregate impact excluding energy is decelerating and remaining moderate even by the standards of the past two years or so when the headline pace was so very low and core prices were much more stable. The current three-month ex-energy CPI (a very volatile bit of data, I might add) ranks just off the top one-third of its last two-year queue of data, but the six-month pace ranks near the bottom of its two-year queue (ranking 21 out of 24 observations).

Shifting sands

Right now inflation and growth trends are caught amid a confluence of trends. Global growth remains weak anchored by still struggling China, plodding Europe and a U.S. economy held back by persistently lethargic productivity growth. However, markets are beginning to churn as an unexpected win of the U.S. presidency by Donald Trump is resetting expectations for growth based on the use of U.S. fiscal policy and other potentially reflationary policies as well.

Hard to restart growth

However, growth has been hard to restart globally. And maybe the new U.S. president is willing to use some tools and take some paths that have not yet been tried. Apart from his bodacious promises, there is little substance of growth there yet. Europe is showing no sign of stepped up growth, just signs of continued sputtering. If inflation expectations are stirring, we should be careful to note that oil prices have made a nice move off their lows and that inflation expectations often ride on the back of oil price swings. How far does oil have to swing? That is an important question for both growth and inflation prospects.

A digression on oil and OPEC

OPEC is still increasing oil output in the wake of telling us about all the cutbacks it was going to produce; that right there is reality check number one. In the end, Russia was not on board to join a program of cuts and Iran is sticking to its plan to pump as much oil as possible since its oil export ban has been lifted. Even the Saudis are hurt at this level of oil prices and they seem reluctant to act as leader and unwilling to undertake cuts for the good of the 'oil team.' The Saudis have cut by 20% the payments to a number of high-level domestic ministers. Saudi Arabia also negotiated a huge bond floatation to help get funds to ease it through these 'hard times.' Despite the OPEC longing for higher prices, there has been no commitment to take the actions that might have that effect. The one clear reason is the hatred of 'free riders'. Oil producers outside OPEC and its direct sphere of influence are not going to join in on production cutting. The oil industry in the U.S. will benefit from high prices. As prices get higher, more U.S. drilling will occur there. This perversely will divert more oil monies to these uncooperative U.S. firms who will benefit from Saudi and other OPEC nations' output reductions...should they occur. It is a sticking point for OPEC and a key instability that the cartel always has had. Even if one is 'on the OPEC team', once prices have risen there will be an incentive to pump more oil and sell it at higher prices. But if cheating were to be widespread, prices would come crashing back down. Oil industry experts often note that the cure for high oil prices is high oil prices (for this reason, as well as other reasons). There always has been and will be incentives to cheat. Even though oil demand is relatively inelastic in the short run (small output cuts could underpin substantially higher prices), no one wants to be the country that reduces its own output to raise prices for everyone else. OPEC and 'friends' are still fighting about this. And the point of this digression on oil is that oil prices are probably going to have this 'one time' impact on lifting inflation rates, but there is not going to be ongoing or escalating pressure from oil because the cartel is too divided to deliver on that goal.

Bond yields rise...do they ever

Bond yields are rising in Europe for a variety of reasons. Italy has an important referendum that could result in its Five Star movement gaining political influence. To some extent, the ripples are spreading from the U.S. bond market which is beating a hasty retreat in the wake of the Trump win. Right now the U.S. is being shaken by new expectations about how policy is going to shift and how the country's very direction is being uprooted by the rogue nonpolitician who promised to not act like an insider. The Trump effect is being felt everywhere and not simply for the potential for it to register demonstration effects beyond the U.S. borders.

Underpinning or overshooting?

I do not yet see the underpinning for any global inflation to take place. OPEC is not lined up to achieve its price goals. China is still too weak and struggling. The dollar is rising and Trump policies, even if 'successful', should also tend to boost the dollar and that will tend to dampen U.S. growth and inflation. A complex scenario is unfolding that will generate effects and counter effects. We should be careful not to expect too much all once. Right now markets seem to have all the trappings of overshooting any reasonable goal of reality.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief