Global| Aug 13 2020

Global| Aug 13 2020German Inflation Moves Lower in July

Summary

Seemingly, no one is worried about inflation. The ratcheting up in oil prices is not having an impact on headline prices. In Germany, the HICP fell by 0.8% in July after rising by 0.5% in June, driving the year-on-year HICP to a flat [...]

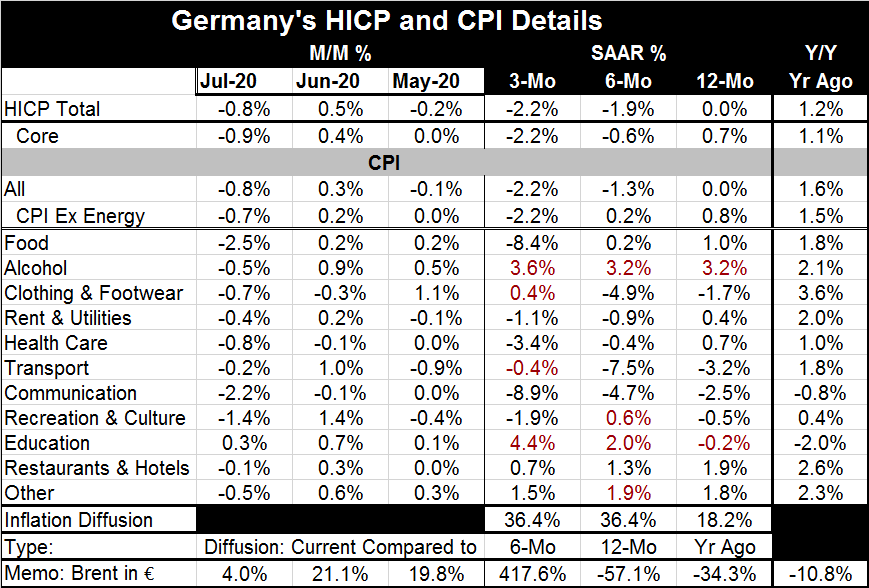

Seemingly, no one is worried about inflation. The ratcheting up in oil prices is not having an impact on headline prices. In Germany, the HICP fell by 0.8% in July after rising by 0.5% in June, driving the year-on-year HICP to a flat performance (0% over 12 months). Inflation is well below the target of a little less than 2% that is the gauge for inflation in all of the EMU. Of course, there are no country by country targets.

Seemingly, no one is worried about inflation. The ratcheting up in oil prices is not having an impact on headline prices. In Germany, the HICP fell by 0.8% in July after rising by 0.5% in June, driving the year-on-year HICP to a flat performance (0% over 12 months). Inflation is well below the target of a little less than 2% that is the gauge for inflation in all of the EMU. Of course, there are no country by country targets.

German core inflation fell by 0.9% in July after a 0.4% rise in June, bringing the core rate over 12 months to a pace of 0.7%, still quite short of what has been sought for overall EMU inflation.

Germany has scrapped a plan to run fiscal surpluses and replaced it with a plan for stimulus in the wake of the coronavirus. German companies, answering a survey from the IFO, have responded that they expect their businesses to be back to normalcy in less than 12 months: in manufacturing firms are saying they will be back to normal in about 10.1 months, while service sector firms say it will take more like 11.7 months. However, both of these seem to be particularly short timelines given the way the infections are breaking out repeatedly and given that there is still not vaccine in hand (except perhaps in Russia). However, on the face of it, Germans are optimistic.

The detail among German domestic consumer prices shows that inflation is still weak and trending lower across most categories. Inflation diffusion is well below 50% for year-on-year inflation and well below that over six months and three months. However, the impact of higher oil prices may just be in its infancy as Brent rose by 4% in July, its third straight month of rising.

Overall EMU inflation has been contained and has been under shooting for some time. Yet, the Germans are notorious for their fear and sensitivity to inflation. For now both the core measure and the headline in Germany offer reassurance that inflation is really controlled. The U.S. has reported an unexpectedly large increase in its monthly CPI and core CPI rates in July, but no one is worried about inflation taking hold there. Certainly, one of the worst things that could happen in this environment would be to see inflation emerge as countries generally have monetary policy at flank speed and are still pulling out the stops sporadically on fiscal stimulus.

Still, globally there is still a great deal of slack. Oil prices may have lifted, but oil is still in abundant supply. As/if oil prices rise from current levels, that will make more and more fracking economic again and that will, in turn, increase the supply of oil and limit oil price increases – a sort of marketplace automatic stabilizer to damp oil price pressures. Unemployment rates globally are still high. Apart from government policy (both fiscal and monetary), there really is no support for the notion of rising inflation. Inflation numbers will continue to percolate in the background and will attract only second tier attention.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief