Global| Oct 20 2020

Global| Oct 20 2020German Inflation Is Still Falling But Show Signs of Stirring

Summary

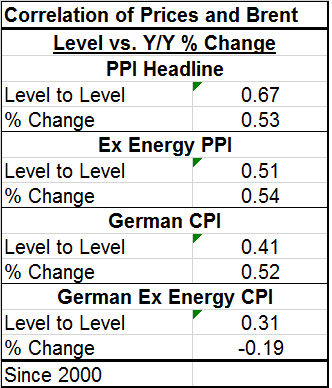

German PPI trends continue to be weak and show prices declines when expressed as year-over-year changes. The German PPI now has eight monthly declines in a row logged for its year-over-year PPI change. The year-on-year drops was [...]

German PPI trends continue to be weak and show prices declines when expressed as year-over-year changes. The German PPI now has eight monthly declines in a row logged for its year-over-year PPI change. The year-on-year drops was largest at -2.2% in May and it has since then been getting smaller (logging a smaller decline) month-by-month. In August the year-on-year drop was 1.2%; in September it is a 1.0% drop.

German PPI trends continue to be weak and show prices declines when expressed as year-over-year changes. The German PPI now has eight monthly declines in a row logged for its year-over-year PPI change. The year-on-year drops was largest at -2.2% in May and it has since then been getting smaller (logging a smaller decline) month-by-month. In August the year-on-year drop was 1.2%; in September it is a 1.0% drop.

The trend in the year-on-year change is therefore still negative for a long stretch of time, but it is showing signs of turning toward flat and rising the potential for positive gains in the period ahead.

Much of this is on the back of declining oil prices. Crude oil (Brent) made its largest year-on-year drop for the year at -62% in April- just one month ahead of the largest PPI headline drop in inflation. In April oil prices fell to $27.09/barrel then climbed back to $45.10/barrel in August. In September, however, oil is slipping again falling to $41.9/barrel. As I write this, oil is trading in the neighborhood of $42.93/barrel suggesting that the significant drop in September may not be a reversal of the uptrend. But with global growth in the grip of the virus again, another patch of weak growth with adverse knock-on impact for oil prices cannot be ruled out.

For now the year-on-year decline in the PPI continues, but as a trend it is less virulent and therefore less worrisome. However, because the virus has leapt back up into business and it has become extremely potent again the risk to growth is back in play. Belgium and the United Kingdom seem to be facing very difficult circumstances. Most of Europe is in the grip.

For now the year-on-year decline in the PPI continues, but as a trend it is less virulent and therefore less worrisome. However, because the virus has leapt back up into business and it has become extremely potent again the risk to growth is back in play. Belgium and the United Kingdom seem to be facing very difficult circumstances. Most of Europe is in the grip.

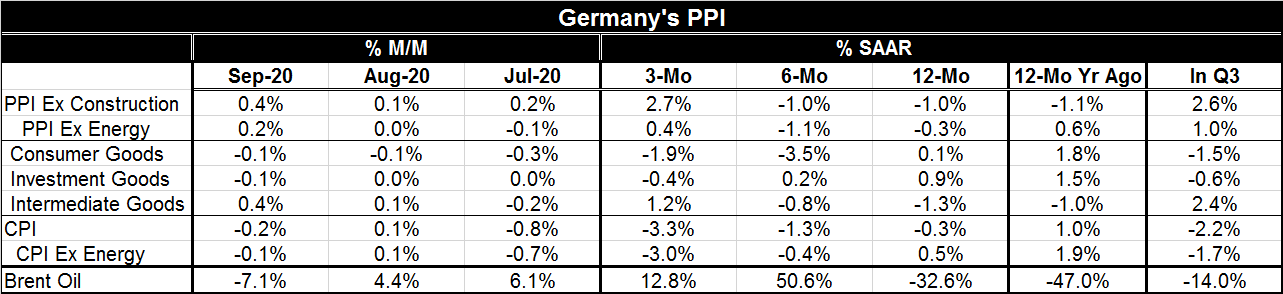

Price trends in Germany as they stand show the headline PPI rising at a 2.7% annual rate over three months; the PPI excluding energy is up at a more modest 0.4% annual rate on the period.

By PPI component, inflation is lower year-on-year only for intermediate goods, the category that most weights oil prices. However, over six months both intermediate goods and consumer goods prices are falling. Over three months prices are falling for consumer goods and investment goods, but they are rising for intermediate goods as oil prices are again moving higher (up at a 12.8% annualized rate over three months and at a 50.6% annual rate over six months).

Meanwhile, German consumer prices even excluding energy are showing decelerations in momentum from 12-months to six-months to three-months with outright declines posted on all horizons except for ex-energy prices over 12 months.

In the just completed third quarter, the PPI headline is up at a 2.6% annual rate with its ex-energy manifestation up at a 1.0% annual rate. The more important consumer price index shows a 2.2% annual rate of decline with its ex-energy index also falling at a still significantly worrisome 1.7% annual rate. The PPI components show declines in Q3 in two-of-three sectors.

Inflation has not been a central bank topic of interest for a while since inflation has not been a problem and has only been under control or at least under the radar. The Germans seem to retain their past loathing of inflation since having suffered through a hyper-inflation. The current ‘undershooting’ seems tolerable and not worrisome to them or to their representatives on the European Central Bank. But in Japan, for some time the Bank of Japan has pondered the impact of persistent target missing (undershooting) on its credibility. In just the last few months, the Federal Reserve has indicated a policy shift and expressed a desire to actually reach its inflation objective and stop its persistent undershooting rather than to treat 2% inflation as an aspirational ideal.

The way that central banks view their inflation targets turns out to be very important and perhaps more important than what that the target actually is. For the moment, we can regard the Germans as probably less willing to do any more in the way of stimulus since deflation seems less of a threat especially with oil prices rising. The ECB has only a mandate for hitting its target of slightly less than 2% that is sufficiently vague to leave some room for maneuver. Looking ahead, since the ECB has done such massive undershooting, it should have great flexibility to institute forbearance with interest rates should inflation rise (when it eventually does rise). At that time, we will see if the ECB will continue to look at the notion of inflation as part of a broad inflation picture or if the Germans will try to focus the ECB on forward-looking inflation to exclude past inflation undershooting.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief