Global| Feb 13 2014

Global| Feb 13 2014German Inflation Continues Under Downward Pressure

Summary

The German harmonized consumer prices edged up by just 0.1% in January after falling by 0.2% in December. Inflation in Germany continues to be subdued. However, over three months the Harmonized Index of Consumer Prices (HICP) is up at [...]

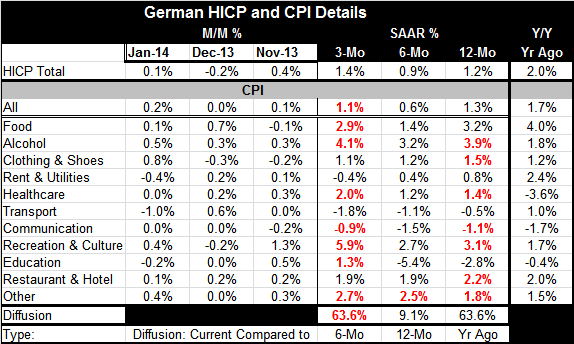

The German harmonized consumer prices edged up by just 0.1% in January after falling by 0.2% in December. Inflation in Germany continues to be subdued. However, over three months the Harmonized Index of Consumer Prices (HICP) is up at a 1.4% annual rate, faster than its six-month pace and faster than the 12-month pace. Germany's domestic CPI index shows a slightly different inflation, up by 0.2% in the month and up only a 1.1% pace over three months, below its 1.3% pace over 12 months.

The German harmonized consumer prices edged up by just 0.1% in January after falling by 0.2% in December. Inflation in Germany continues to be subdued. However, over three months the Harmonized Index of Consumer Prices (HICP) is up at a 1.4% annual rate, faster than its six-month pace and faster than the 12-month pace. Germany's domestic CPI index shows a slightly different inflation, up by 0.2% in the month and up only a 1.1% pace over three months, below its 1.3% pace over 12 months.

The German domestic CPI shows that inflation is accelerating in 53% of the categories over three months compared to its six-month pace. Six-month inflation is decelerating sharply and only 9% of the categories show upward pressure compared to a 12-month horizon. The 12-month inflation rate is decelerating in about 63% of its categories compared to the year-over-year inflation rate of 12 months ago. On balance there is not much here in the way of dependable trends. There is still a great deal of volatility in what German prices are doing. However, prices are staying under control.

Over three months the highest annualized inflation rate is recreation and culture at a 5.9% pace, followed by alcohol at a 4.1% pace and food at a 2.9% pace. At the other end of the spectrum, prices are falling at a 1.8% annual rate for transportation, at a 0.9% pace for communications and at a 0.4% pace for rent and utilities. Over six months the high inflation rate is for the `other category' at only 2.5%, while three categories, education, communication, and transportation show price declines. Year-over-year trends mark the highest inflation for alcohol at 3.9% followed by food at 3.2%. At the low-end, transportation prices are falling by 0.5%, communications falling by 1.1% and education costs are down by 2.8%. There is still a lot of weakness in German prices and not much sign of acceleration.

Inflation trends also tell us something about growth although that is an inductive conclusion you have to be careful with. The German economy has turned somewhat more erratic recently. German orders and industrial output have been showing fluctuations. The rest of the euro area is going through some of the same difficulties.

Recent reports, for example, are still weak. Unemployment continues to move higher in Greece. It is up to 28% in November from 27.7% in October. In Lithuania, producer prices continue to fall; they are down for the 11th consecutive month in January. In the UK, there is evidence of progress as property repossessions are the lowest since 2007; they have been falling since their peak in 2009. Dutch inflation also has continued to ease and is at its lowest level in 3.5 years. In Switzerland producer prices and import prices were unchanged in January.

The European Central Bank has generally been doing whatever it can get traction in the economy, an action that should result in putting some pressure on the inflation rate. Economic traction has been hard to get and inflation continues to be erratically low in the euro area. Germany continues to anchor trends in the euro area although it is not consistently running the lowest inflation rate anymore. Ongoing distress in a number of southern European states has kept inflation there very much in check. When we look at inflation these days, we're looking less to see if it is accelerating than to see if it is decelerating to get some idea whether deflation is a growing risk. We also seek evidence of growth taking root. We get few reassurances from inflation in January 2014.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief