Global| Dec 28 2018

Global| Dec 28 2018German Inflation Calms After a Year of Hullabaloo

Summary

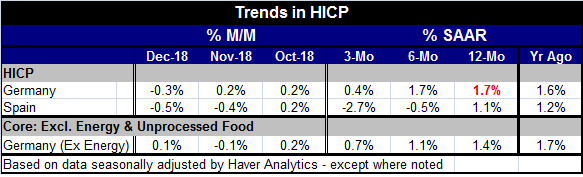

Germany's HICP fell by 0.3% in December. In Spain, the HICP fell by 0.5%. German ex-energy inflation rose by only 0.1% in December after a 0.1% decline in November. Where's the beef? The ECB has been under a steady drumbeat of [...]

But Rest Assured: There Is More Hullabaloo to Come...Just Not over Inflation

Germany's HICP fell by 0.3% in December. In Spain, the HICP fell by 0.5%. German ex-energy inflation rose by only 0.1% in December after a 0.1% decline in November.

Germany's HICP fell by 0.3% in December. In Spain, the HICP fell by 0.5%. German ex-energy inflation rose by only 0.1% in December after a 0.1% decline in November.

Where's the beef?

The ECB has been under a steady drumbeat of pressure to dismantle its stimulative programs and has been criticized for letting inflation rise too much. Now in Germany, the strongest economy in the EMU with the most overheated labor market, the price level is falling in December and the year-on-year rate of inflation has dropped back to a very comfortable very stable under target 1.7% - a pace that even the Bundesbank could love. The pace in traditionally more inflation-prone Spain is only 1.1% over 12 months. And German inflation excluding energy is a paltry 1.4%.

Inflation is ending 2018 much better behaved than almost anyone expected. Fancy that!

Much of this owes to OPEC and its ongoing disorientation along with a special mention, of course, to fracking in the U.S. to say nothing of Iran continuing to be able to export oil even with U.S. sanctions (and some exemptions) in place. The oil market is a wily creature. For now the fickle finger of fate points lower for oil, but one can never be sure of when that finger will invert, develop a crook and beckon prices higher. Still, it does seem that the oil market and concerns about global growth are going to keep petrol prices pouting for some time.

Compared to December of one year ago German inflation is 'up to' a 1.7% pace compared to 1.6%. The German ex-energy pace is down to 1.4% from 1.7% a year ago. Inflation in Spain is lower at 1.1% compared to a 1.2% over 12 months ended in December 2017. Deck the halls with inflation-fear folly!

If we assess inflation trends over the intra-year period from 12-months to six-months to three-months, we find the annualized rate of inflation is progressively falling for all the measures in the table. On Dasher on Dancer, on Donder and Draghi, inflation is lower and sill looking soggy!

Financial markets and prospects

Financial markets are in a tizzy. The U.S. stock market had a horrific sell off then the DJIA jumped out of the blue by over 1,000 points in a day, a gain of over 5% (remember when a 500-point drop was a 20% decline?). Trump minions are now saying that Powell is safe based on viewing the video-tape replay after Trump had called him 'out' at the plate initially. It's hard to know if we should be reassured by any of this, given the mercurial nature of the CEO in Chief and his penchant for holding a grudge. Maybe he will find a new angle on the video-tape replay at some point in the future and revert to his original call? Maybe Powell really is safe until Trump calls him a 'Democrat?' That was the signal that ended it all for Mattis, anyway.

Clearly, U.S. policy is based on some factors that are hard to pin down and harder still to depend on. Market valuations depend on Fed policy and on the Fed being independent. But the President was hired (Oops, I mean elected) to be a disruptor and in his world that does not mean that disruption faces any boundaries. Except when it does and even then a few histrionics can be used to great effect.

As the year draws to a close, the Fed has managed to raise Fed funds steadily even though that was never its stated policy (nothing up my sleeve!). I wonder why the Fed felt it could not tell us that that was its true agenda.

The U.K. is still mucking around with Brexit scenarios. Italy has been given a new longer leash on life by the EU Commission that has accepted an only slightly pared budget position and a promise of a smaller deficit next year. China seems to be offering all sorts of changes to try and settle the U.S. trade dispute but not really getting to the nub of what the U.S. wants.

What do we want? FAIR TRADE! When do we want it? NOW!

Good luck with that. Instead, China has offered to drop tariffs to zero on all sorts of things that the U.S. could never export to it on its best of days.

While Trump remains a highly controversial and much criticized figure, it is interesting to note how his trade attacks have paved the way for many more criticisms from mainstreamers about China and about China's unfair trade practices. There is no more saying, 'Well, it's close enough to Free trade for me...' And no more 'Well, they get IOUS and we get goods!' Thank God Trump's shaking things up has brought some to their senses.

Here is hope that in 2019 Mr. Trump knows when to stop shaking and when to start compromising and deal-making. Here is hoping he does not have a fit of jealousy over the 'Wall' that Mr. Putin just successfully completed around Crimea.

There is still a U.S.-EU trade deal to be struck. And there are plenty of places for things to go wrong…or to surprise the critics and to go 'right.' Markets are in disarray wondering what will happen, worried one day and ebullient the next. Unfortunately market schizophrenia is unbecoming. Investors like their markets better behaved. Will that happen in 2019?

From this vantage point, it is hard to tell. But at least the inflation scare is off. And in the U.S., the central bank can at least be happy that it has been able to get Fed funds above 2% without creating a recession (so far…). And the dogs have called Trump off the Fed (or vice versa). The ECB has stoppered its stimulus program. The BOJ is still running its stimulus flat out. And the BOE is waiting on a Brexit clarification. But China is on a hot seat and conditions there are deteriorating.

Note that since the U.S. demand for Canada to extradite a Huawei officer, that request has stirred up all sorts of animosities in China that has begun to incarcerate and charge Canadians in China in ways that make no sense. As 2018 draws to a close, China has revealed its true self to the world. Its belt and Road program is a bait and switch program of influence, entrapment and planned domination. Even economists that did not used to say bad things about China are having second thoughts. You know…it's way overdue. It's time for Baby Huey to change its own diaper.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief