Global| Apr 08 2013

Global| Apr 08 2013German Industrial Production

Summary

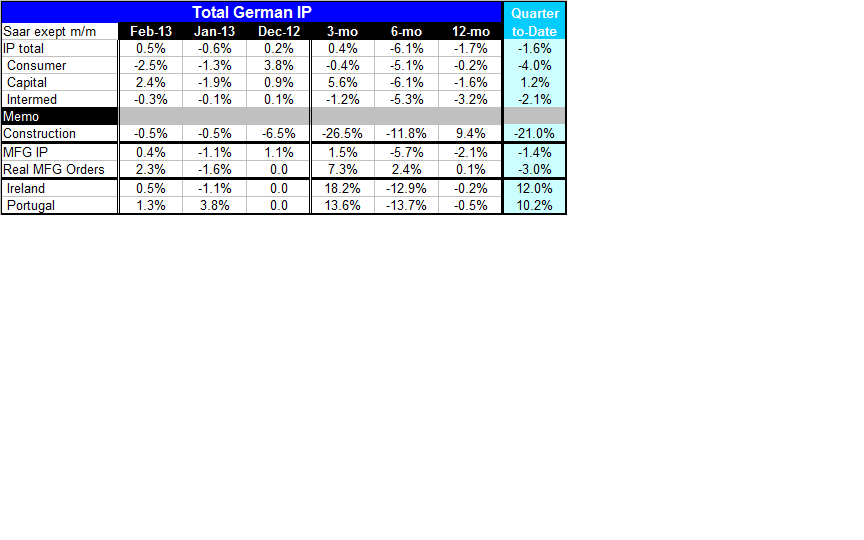

German industrial output rose by 0.5% in February after dropping by 0.6% in January. Even so, over three-months, IP is up at just a 0.4% annual rate. With two months of data in for the first quarter, IP is still shrinking at a 1.6% [...]

German industrial output rose by 0.5% in February after dropping by 0.6% in January. Even so, over three-months, IP is up at just a 0.4% annual rate. With two months of data in for the first quarter, IP is still shrinking at a 1.6% annual rate.

German industrial output rose by 0.5% in February after dropping by 0.6% in January. Even so, over three-months, IP is up at just a 0.4% annual rate. With two months of data in for the first quarter, IP is still shrinking at a 1.6% annual rate.

Consumer goods output is shrinking at a 4% annual rate in Q1. Capital goods output is up at a 1.2% annual rate. Intermediate goods output is falling at a 2.1% annual rate.

Construction output has been steadily falling. It is declining at a 21% annual rate in Q1.

German manufacturing output and real orders elevated in February, but each series is still contracting in Q1. Only Ireland and Portugal in the Zone have reported out IP data for February and both have industrial output rising strongly two months into the first quarter.

Overall the European Community remains under pressure and while the German economy is still on a different level than the rest of the Zone but it is not immune to the stresses, it is still laboring. Overall e-Zone investor confidence fell in April for the second month in a row to steeply negative -17.3 reading from -10.6 in March. Portugal is under pressure after its supreme court has disallowed a large slug of budget cuts it had adopted to meet its austerity demands. Now Portugal needs to launch 'plan B' to stay in compliance with the austerity demands that have been placed upon it. Germany is still surrounded by a lot of pressure and weakness. While it is doing better than the rest of Europe, neither Germany nor the e-Zone are yet out of the woods.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief