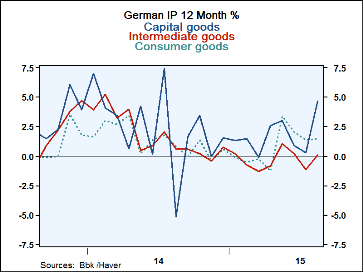

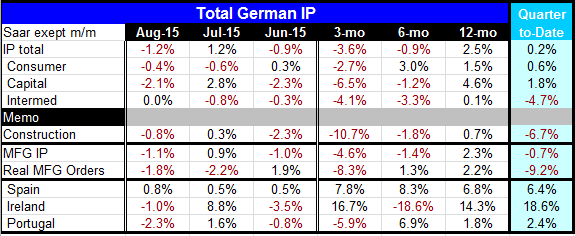

In August German IP fell by 1.2% marking declines in two of the last three months. Last month's 1.2% gain is offset by this month's 1.2% drop. Consumer goods and capital goods output both fell in August; intermediate goods output was flat.

In August German IP fell by 1.2% marking declines in two of the last three months. Last month's 1.2% gain is offset by this month's 1.2% drop. Consumer goods and capital goods output both fell in August; intermediate goods output was flat.

Over three months, output is lower in all three sectors. Over six months overall output is lower and output is lower in capital goods and in intermediate goods. Over 12-months output is higher overall and in each sector. Total output, the output of capital goods and of intermediate goods shows sequential weakness, with weakness more pronounced over more recent periods.

Despite the weakness over three-and six-months, in the quarter-to-date overall IP and all sectors except intermediate goods are showing gains in this period.

Construction is down in August and is lower in two of the last three months. It too is showing sequential weakness and is lower in the quarter-to-date.

Manufacturing as a whole is down by 1.1% in August and lower in two of the last three months. There is sequential weakness in MFG and MFG output is falling in the quarter-to-date. MFG output rightly parrots MFG orders which are also very weak and substantially weaker in the most recent months.

Three early reporters in EMU Spain, Ireland, and Portugal show somewhat better strength than Germany. Spain shows output up in August and up in each of the last three months. Ireland and Portugal each show output lower in August, up in July, and falling in June. Still their sequential strength is quite solid except for Portugal which is showing a net decline in output over three-months. All three countries show gains in the quarter-to-date.

German IP echoes the conditions of weakness for orders where developing country weakness and especially weakness in China have been impacting orders. Just yesterday the IMF trimmed its global outlook again. We are deep into an economic recovery that has not had much in the way of normal recovery growth or even ordinary trend growth. Still the recovery is showing signs of weakening. The proximate cause is weakness in commodity prices which hits developing economies and boomerangs to slow exports from the most industrialized countries.

Today Japan reported its lowest LEI value since May of 2014. There are no signs of any sort of turn-around. The global economy appears to be in the midst of another downdraft. It is too early to tell how severe it will be. But it catches the developing economies not yet having remedied their reliance on fiscal spending and with monetary measures seeming to be on their last legs. If weakness does cumulate it will come at one of the worst times possible. I think fiscal policy is still a tool that could be used but it is out of favor and if it is used it will be as a last resort. Moreover, it is likely to be less effective because of competitiveness problems.

Exchange rate misalignment is responsible for many of the global ills. Too much output has come from China and Asia where workers are low-paid and have a high savings rate. As a result this shift in the location of income generation lowers the global (growth) multiplier. In the West, nations are less competitive as a rule and income growth has lagged there where the propensity to spend and the (growth) multiplier is the highest. China's development in particular was supported by a too-weak exchange rate and has created dislocations. And with production in Asia still cheaper than in the West, firms are reluctant to reinvest in the West-extending the weakness. Fiscal policy spending will not remedy this. A vicious circle of sort has been set in motion. Let me throw in a reminder that the US has been in a nearly constant current account deficit since the early 1980s- a period of nearly 35 years. Nations have neglected misaligned exchange rates for a long time. In the US it has made no difference, under Republicans or under Democrats it has been the same thing. There is no realization of what damage misaligned exchange rates are doing to the global economy. Until this is fixed, fiscal and monetary policy solutions are straws in the wind not solutions in the works.

Global| Oct 07 2015

Global| Oct 07 2015 In August German IP fell by 1.2% marking declines in two of the last three months. Last month's 1.2% gain is offset by this month's 1.2% drop. Consumer goods and capital goods output both fell in August; intermediate goods output was flat.

In August German IP fell by 1.2% marking declines in two of the last three months. Last month's 1.2% gain is offset by this month's 1.2% drop. Consumer goods and capital goods output both fell in August; intermediate goods output was flat.