Global| Apr 09 2014

Global| Apr 09 2014German Imports Finally Begin to Outpace Exports

Summary

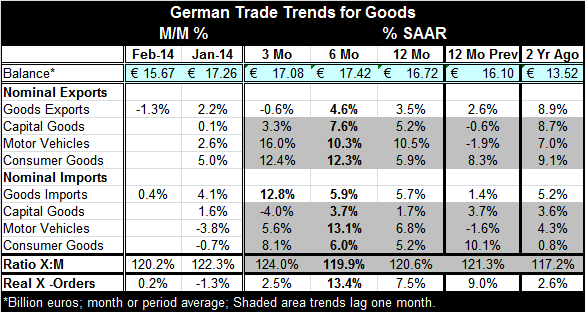

German goods exports dove lower in February, dropping by 1.3% after a strong gain of 2.2% in January. Imports continued to rise with a moderate 0.4% gain after a surge of 4.1% in January. These forces combined to shrink the German [...]

German goods exports dove lower in February, dropping by 1.3% after a strong gain of 2.2% in January. Imports continued to rise with a moderate 0.4% gain after a surge of 4.1% in January. These forces combined to shrink the German surplus in February from 17.26 billion euros to 15.67 billion euros.

German goods exports dove lower in February, dropping by 1.3% after a strong gain of 2.2% in January. Imports continued to rise with a moderate 0.4% gain after a surge of 4.1% in January. These forces combined to shrink the German surplus in February from 17.26 billion euros to 15.67 billion euros.

Year over year the German surplus is lower by about 1 billion euros. It is the first year-over-year contraction in the surplus since August of last year.

German exports are higher by 3.5% over 12-months compared to a gain of 5.7% for imports. The relatively stronger gain in imports has shrunk the surplus - can it continue?

The data by category lag one month. They show very strong 12-month gains in motor vehicle exports and strong gains for capital goods and consumer goods exports as well. Imports show strong gains in motor vehicles and consumer goods with capital goods imports up at a moderate pace.

The ratio of exports to imports is below where it was one year ago, underlining that import value is gaining slightly on exports. The composition of imports shows that, as of January, consumer goods imports are gaining and rising with steady acceleration. Meanwhile export trends have become a bit uneven.

Over the past 12-months imports rose by 5.7%, faster than their gain of 1.4% over the previous 12-months. Exports grew by 3.5%, also up from their previous 12-month pace of 2.6%. Both exports and imports are accelerating on that basis. Real export orders are up by 7.5% over 12-months, slightly weaker than their previous 12-month gain of 9%. Still, exports have solid momentum.

The German surplus now shows multi-monthly signs of pulling back. Exports are still strong, but imports are starting to accelerate, even for consumer goods. Germany may finally have reached the point where its recovery is going to start to aid other countries in the euro area by ramping up German domestic demand. It's a hopeful time for German trade underpinned by some encouraging trends for the rest of the EMU.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief