Global| Jul 25 2014

Global| Jul 25 2014German Ifo Slips for Third Consecutive Month

Summary

Germany's Ifo index fell for the third straight month in July. The index fell to 8.6 from June's 11.8. In April it stood at 14.7; it has lost 6.1 points in four months. A number of German reports have been weak recently, ranging from [...]

Germany's Ifo index fell for the third straight month in July. The index fell to 8.6 from June's 11.8. In April it stood at 14.7; it has lost 6.1 points in four months. A number of German reports have been weak recently, ranging from industrial production to export orders and exports themselves. This report adds to that streak. However, yesterday's Market flash PMI readings showed a sharp rebound for German services and some pick up in German manufacturing. The picture of the German economy that continues to emerge from these reports is quite murky with dots that just do not want to get connected.

Germany's Ifo index fell for the third straight month in July. The index fell to 8.6 from June's 11.8. In April it stood at 14.7; it has lost 6.1 points in four months. A number of German reports have been weak recently, ranging from industrial production to export orders and exports themselves. This report adds to that streak. However, yesterday's Market flash PMI readings showed a sharp rebound for German services and some pick up in German manufacturing. The picture of the German economy that continues to emerge from these reports is quite murky with dots that just do not want to get connected.

There are readings of weakness for other EMU nations over this period as well. And all of Europe is under a pall because of the conflict in Ukraine. The news there continues to get darker, as does the news from Gaza. Some wounds won't heal. Today the U.S. accused Russia of firing rounds from Russian territory into Ukraine itself. For its part, Europe is readying an expanded list of Russian nationals to be sanctioned. It is set for release today. And in response to all the pressure, the Central Bank of Russia has unexpectedly hiked its key rate to 8% today. It may be that some of Germany's problems are geopolitical, but the way that things are going, the geopolitical and the economic are converging fast.

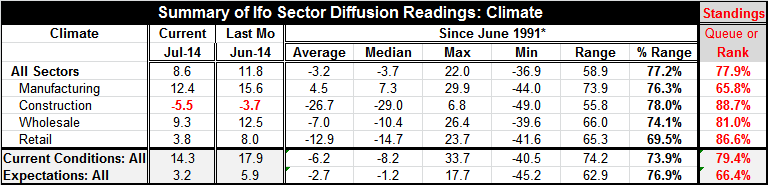

The chart above plots the Ifo sector indices while the table below plots the diffusion readings from the Ifo. In the chart, we see declines marking a broad slippage. Business expectations, current conditions and climate indices all are falling. In the table, we see that all indices have declined month-to-month in July. The all-sector index fell by more than 3 points, as did manufacturing. The construction reading fell by less than 2 points. Retailing fell by more than 4 points, taking the biggest hit.

The percentile standing of these indices have manufacturing as the weakest reading; it stands in its 65th percentile of its historic queue. Construction, despite its negative reading, has the strongest standing, in its 88th percentile. Retailing is close behind in its 86th percentile with wholesaling in its 81st percentile. The all-sector index now stands in its 77th queue percentile. That means it has been higher 23% of the time. The 80th percentile readings are relatively strong, while the 65th percentile reading for manufacturing is moderate at best.

The all-sector current index has slipped to the 79th percentile, but expectations are only at the 66th percentile.

If geopolitics are the big problem, expectations would be hit the hardest- and that is the case here. But the current index is also down from its peak value of 18.8 in April. Germany seems to be feeling the pinch from reduced activity as well as from dwindling expectations with likely links to geopolitics. which are continuing to erode.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief