Global| Jan 25 2017

Global| Jan 25 2017German IFO Sector Diffusion Indexes Back off in January

Summary

January brings a slight rolling over of the values for the IFO index. Each sector has a reading that is slightly lower month-to-month. The combination all-sector index is lower by 2.2 points on the month. This is comprised of a [...]

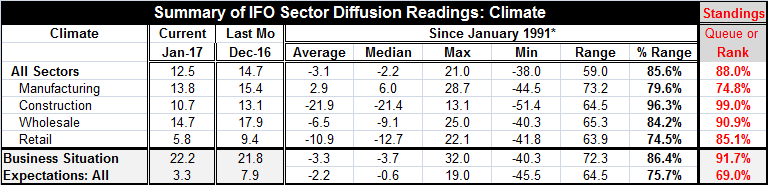

January brings a slight rolling over of the values for the IFO index. Each sector has a reading that is slightly lower month-to-month. The combination all-sector index is lower by 2.2 points on the month. This is comprised of a manufacturing reading that is lower by 1.6 points, a construction sector that is lower by 2.4 points, wholesaling sector that is lower by 3.2 points and retailing sector that is lower by 3.6 points.

January brings a slight rolling over of the values for the IFO index. Each sector has a reading that is slightly lower month-to-month. The combination all-sector index is lower by 2.2 points on the month. This is comprised of a manufacturing reading that is lower by 1.6 points, a construction sector that is lower by 2.4 points, wholesaling sector that is lower by 3.2 points and retailing sector that is lower by 3.6 points.

Despite all this month-to-month weakness, the all-sector index still sits in its 88th queue percentile and is higher only 12% of the time historically (since 1991). Construction has the relative strongest standing with a 99.0 percentile positioning. Wholesaling is next with a 90.9 percentile standing, followed by retailing with an 85.1 percentile standing. The lowest standing is in manufacturing, at a standing of 74.8%, which has been higher than its January reading a bit more than 25% of the time.

The business situation has improved month-to-month with index of current conditions up to 22.2 in January from 21.8 in December. But what is lacking is a strengthening outlook as expectations have slipped month-to-month to 3.3 in January from 7.9 in December, still a net positive outlook, but one that is substantially weaker than just last month. It is the weakest expectations reading since August of last year. While the business situation is stronger only about 8% of the time, expectations are better 31% of the time. As such, expectations are still solidly in the upper portion of their historic distribution but are well short of being hailed as strong and are sagging on weakening momentum.

The IFO report is not fully consistent with the sector report on manufacturing and services released yesterday by Markit. In the Markit framework for Germany the private sector slipped month-to-month with manufacturing improving and services eroding. By comparisons, all sectors fade somewhat in the IFO survey but manufacturing fades by the least- it is the relative strongest month-to-month. In terms of the assessment of the level of activity, IFO has manufacturing as the weakest sector while in the market framework services are the weakest. And this is not just because of assessing them over different horizons since if we evaluate sectors under the IFO only since January 2011 as we did for the Markit assessment we would find the same result that manufacturing in the IFO framework is weaker and the service components each stand stronger.

The Markit and IFO surveys each give us a significantly different look at the German economy and where they find that risk and weakness reside. But this has to do with differences in what the two surveys measure.

The truth is that the German economy is the best-performing in Europe. Its finances are running near a budget surplus situation. But the influx of migrants and the resulting social instability that the influx of migrants has created may have impacted the services sector more than the manufacturing sector. The German economy tends to be led by manufacturing and external demand and it still is to the extent that the German current account surplus is massive by world standards. Still, manufacturing is not performing up to its usual standards because of global weakness. Absolute and relative measures of the German economy are out of sync and the German economy is definitely out of sync with its usual historic outlook and cyclical behavior. What we see in the Markit and IFO rankings are different ways in which historic comparisons find the German economy lacking. There is no quick or easy way to put the IFO and Markit readings on the same footing; the surveys are simply different. Any way you slice it the Markit survey simply finds more weakness in services than does the IFO in either current conditions or in expectations (those IFO data are available with a lag). As an overarching reading, the GfK consumer survey for Germany continues to find consumer nearly on top of the world. Clearly, we know that the German people regardless of these surveys have worries about migrants, about the stability of the EMU, about rising inflation, and about their own upcoming elections in which Angela Merkel will run again but with her reducing popularity. Clearly, the way in which a survey poses its questions in this environment will have a lot to do with what the responses will be. I suspect that the German people and German firms are not a cozily happy as some of the surveys portray them. But it's hard to say if their angst is playing out more in the services sector or in the manufacturing sector.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief