Global| Aug 25 2015

Global| Aug 25 2015German Ifo Rose in July But All Is Not Rosy

Summary

The German Ifo index rose in July by one point. Two of its four sectors also rose and two withered. Rising were manufacturing by 0.4 points and wholesaling by an eye-popping 6.6 points. Wholesaling includes the important German export [...]

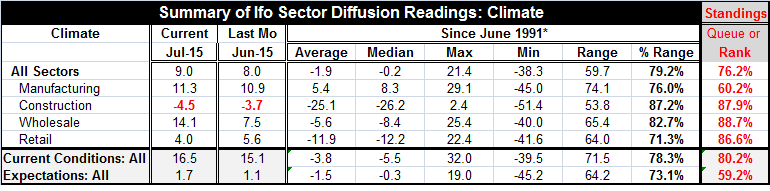

The German Ifo index rose in July by one point. Two of its four sectors also rose and two withered. Rising were manufacturing by 0.4 points and wholesaling by an eye-popping 6.6 points. Wholesaling includes the important German export sector. Its strong rise in July is the 11th greatest monthly gain in the last 146 months (12 years). Falling on the month was construction that moved lower by 0.8 points and retail that fell by 1.6 points.

The German Ifo index rose in July by one point. Two of its four sectors also rose and two withered. Rising were manufacturing by 0.4 points and wholesaling by an eye-popping 6.6 points. Wholesaling includes the important German export sector. Its strong rise in July is the 11th greatest monthly gain in the last 146 months (12 years). Falling on the month was construction that moved lower by 0.8 points and retail that fell by 1.6 points.

The all-sector standing has climate in the 76th percentile of its historic range. That is a moderately positive reading. Among the specific sectors, manufacturing is the weakest with a 60th percentile standing. Wholesaling is now the strongest with the 88th percentile standing. Construction and retailing are close behind with rankings in their 87th and 86th percentiles, respectively.

The current conditions index rose to 16.5 in July from 15.1 in June. Expectations rose to 1.7 from 1.1. Current conditions stand at their 80th percentile. Expectations are at their 59th percentile, a decidedly marginal reading albeit still positive (above 50).

Despite the drive in the German economy, construction cannot find its footing. Retailing has a strong standing overall but is slipping for the month. That's a bad reading from the consumer. Wholesaling is flying with very strong momentum and manufacturing is improving. That is Germany's traditional base. We have yet to see strength emerge in the PMI framework for manufacturing to corroborate this, however.

Of course, looking ahead Germany will have to make sense of the global economic chaos. And there is still the issue of Greece to be settled. While China's markets continue to plunge today, European markets rose and the U.S. market opened higher. While this is welcome news, there has been a lot of wealth destroyed by the global stock market selloff. Dropping wealth usually curtails consumption.

In all likelihood we are looking at a weaker year ahead than we previously expected. And there is no guarantee that just because stocks bounced today they will stay higher tomorrow. Despite some well-delayed policy moves by China that it announced today, China has some severe economic issues it must yet deal with. They will not be solved by dabbling in financial markets. Its banks are shaky and it has severely misaligned asset prices. It is not addressing them.

We believe there are structural problems of many sorts in Europe and in the U.S., too. Also the world trading mechanism has a broken exchange rate module. These problems have contributed to uneven trade, skewed growth and unsustainable flows of funds that have been the basis for financial excesses.

Until these issues are addressed, this era of weak growth will continue. That means the risk to the downside will continue to loom large and could be triggered by events that healthy economies or economic systems could normally shrug off. U.S. monetary policy is still an important staple of the international financial system. Everyone is still waiting to hear what the Fed will do. Will it follow the advice of Martin Feldstein and hike rates anyway? Or will it follow the advice of Larry Summers and keep rates low because of secular stagnation? It matters.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief