Global| Feb 22 2021

Global| Feb 22 2021German IFO Remains Weak But Improves

Summary

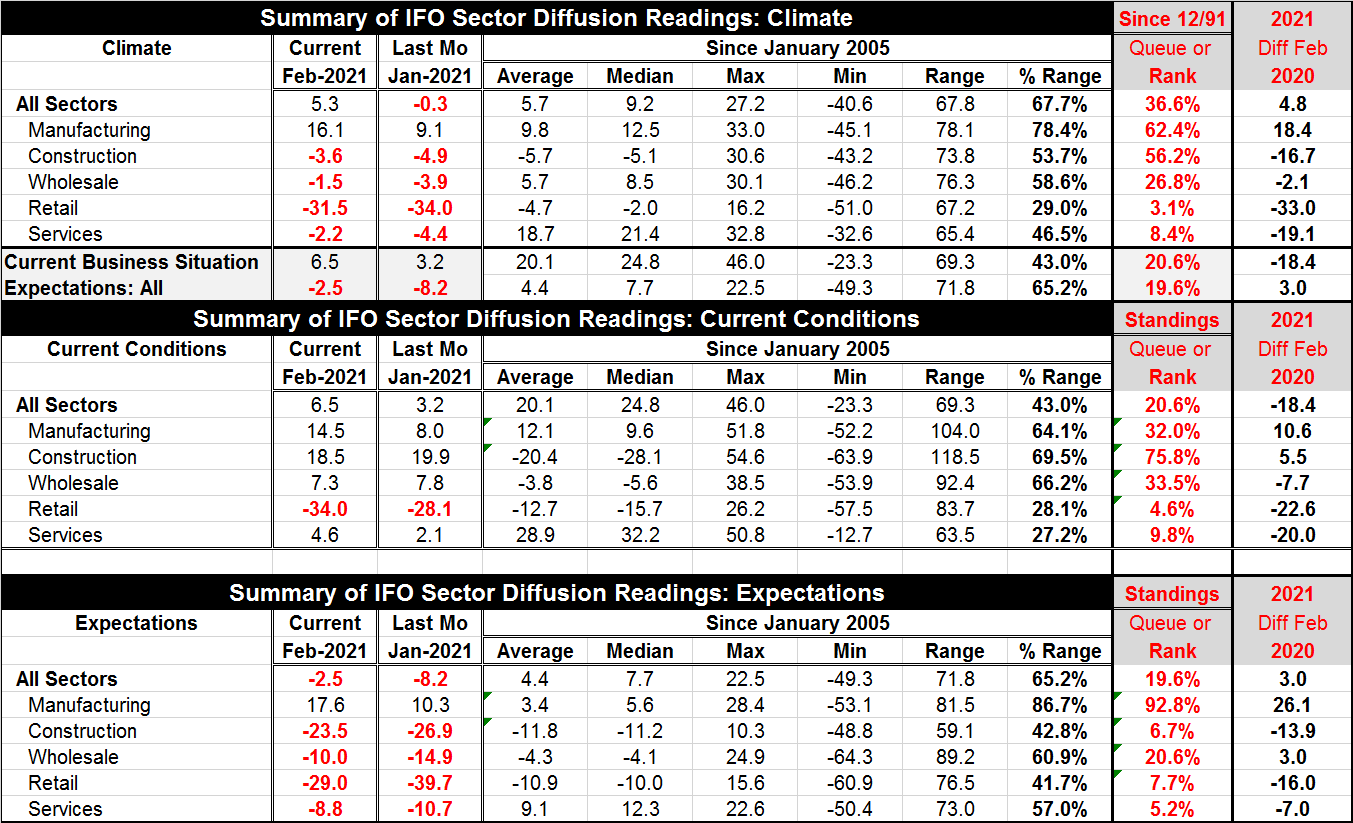

The German IFO comprehensive business survey saw its all-sector climate index rise to 5.3 in February from -0.3 in January. The current conditions index improved to 6.5 in February from 3.2 in January. Expectations also improved to [...]

The German IFO comprehensive business survey saw its all-sector climate index rise to 5.3 in February from -0.3 in January. The current conditions index improved to 6.5 in February from 3.2 in January. Expectations also improved to -2.5 in February from -8.2 in January. Still, these readings are weak. The climate index has a 36.6 percentile standing; the current index and has a 20.6 percentile standing; and expectations have a 19.6 percentile standing. Each of these standing metrics is below- well below-the 50% mark that chronicles the median for each series. While the IFO index shows ongoing improvement, the basic message is that conditions remain extremely weak. There's a long way to go to get back to normalcy.

The German IFO comprehensive business survey saw its all-sector climate index rise to 5.3 in February from -0.3 in January. The current conditions index improved to 6.5 in February from 3.2 in January. Expectations also improved to -2.5 in February from -8.2 in January. Still, these readings are weak. The climate index has a 36.6 percentile standing; the current index and has a 20.6 percentile standing; and expectations have a 19.6 percentile standing. Each of these standing metrics is below- well below-the 50% mark that chronicles the median for each series. While the IFO index shows ongoing improvement, the basic message is that conditions remain extremely weak. There's a long way to go to get back to normalcy.

This table has an added column to track improvement since the virus came to town. It is the final column that looks at the change in the index from February 2020 forward. On that timeline, climate is better by 4.8 points. The current index is worse by 18.4 points and the expectations reading is better by 3 points. The improvement in expectations to a net positive is new with all of it happening this month when the expectations index moved by 5.7 points carrying the index to a positive change vs. February of one year ago.

A look across the various sectors shows that retailing, services, construction and wholesaling have been the most impacted sectors. Only manufacturing shows gains in climate, current conditions and expectations. Even so manufacturing has a very high 92.8 percentile standing for expectations that compares to a very listless 32.0 percentile standing for its current index and a moderate 62.4 percentile standing for its climate reading.

Construction, wholesaling, retailing and services all show declines from February 2020 with all sectors showing double-digit drops except wholesaling where the drop is just 2.1 points. On the current index, all those same industries show drops with the exception of construction; that industry makes a gain of 5.5 points. Moreover, construction has the highest queue standing of all sectors for the current conditions aspect. Moving on to expectations, retailing construction and services show declines from one year ago. Manufacturing has the highest expectations standing- and it is extremely strong- while every other sector is well below the 50% mark.

We find a great deal of variation in this report not just across industries but even for the same industry over different assessment criteria. There is precious little strength or even firmness here. Of the 18 assessments (5 industries and an industry total over three different criteria), there are only four out of these 18 with values over 50% which places them above their historic median values back to 2005. However, industries are showing scattered progress since the virus struck. And the virus has continued to linger and seems to still pose a risk of striking again. It remains unclear how long it will be before the benefits of herd immunity are experienced anywhere. Scientists continue to have very different views on this subject. And various transactors groups in the economy have very different attitudes. Some professions do not want to mingle until they have been vaccinated. In the U.S., some teachers do not want to teach until they and their students have been vaccinated. Other people are ready to defy lockdowns and engage in the economy today. All this makes it very difficult to handicap the future. For now the expectations readings in the IFO are not all that encouraging. They are positive, improving, but doing so slowly, and still very weak.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief