Global| Sep 24 2015

Global| Sep 24 2015German Ifo Moves Higher, Bucking Some Contrary Trends

Summary

The German Ifo index showed improvement in September in three of its four sector indices. Current conditions eroded, but expectations improved. The index had been expected to weaken in the month. Instead, the Ifo index rose. The [...]

The German Ifo index showed improvement in September in three of its four sector indices. Current conditions eroded, but expectations improved. The index had been expected to weaken in the month. Instead, the Ifo index rose. The consumer outlook index from GfK for October has receded. The ZEW current index, previously reported, had moved slightly higher while its outlook index had plunged. There are mixed signals for Germany but not many in this report.

The German Ifo index showed improvement in September in three of its four sector indices. Current conditions eroded, but expectations improved. The index had been expected to weaken in the month. Instead, the Ifo index rose. The consumer outlook index from GfK for October has receded. The ZEW current index, previously reported, had moved slightly higher while its outlook index had plunged. There are mixed signals for Germany but not many in this report.

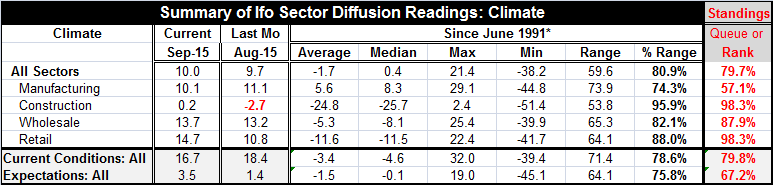

The all-sector Ifo index rose to 10.0 in September from 9.7 in August. The construction sector moved to a positive reading at 0.2 this month from -2.7 in August. Wholesaling moved up to 13.7 in September from 13.2. The retail reading jumped to 14.7 in September from 10.8, a large jump. The two-month gain in the retail sector index is the 11th largest two-month gain in the last 11 years. Manufacturing, already weak, eroded further.

Sector indices in Germany have consistent strong readings with one exception, manufacturing. The all-sector index has the 79.7 percentile standing. It is dragged down by the 57.1 percentile standing in manufacturing. Construction and retailing have the 98th percentile standings. Wholesaling has the 87th percentile standing.

The current conditions index is at the 79th percentile standing. Expectations have the 67th percentile standing.

Ifo Outperforms ZEW in September

The Ifo gauges outperformed expectations for them in September. The earlier ZEW index had showed a sharp drop in expectations with a small bump up in current conditions. The Ifo has improved in leaps and bounds over the ZEW index in September. But in the forward-looking GfK index for German consumer climate is seen slipping for the second month in a row as it has gone four months without posting an increase in value.

German Consumer Climate

The lagging economic confidence component in the GfK reading fell sharply in September to 6.4 from 16.6. That index now stands in the 52nd percentile of its historic queue of data- a much weaker standing than any of the metrics in the Ifo survey (except for manufacturing). Consumers and businesses have very different views of economic performance. However, when consumers assess their income expectations and the environment for buying, they give them standings in the 90th percentile or higher in their historic queues of responses, more like the assessments we get in the Ifo survey this month.

On balance, Germany is feeling some pressure. The manufacturing sector is bearing the brunt of the distress. In another month or so, we will see how hard the Volkswagen scandal hits Germans. The newest news on VW is that it also cheated on its diesel emissions tests in Europe as well. In the U.S., there has been talk of an $8 billion fine. VW has put aside 6 billion euros. But now there will also likely be fines in Europe. The auto sector is a big employer in Germany so the notion that there could be substantial repercussions from the VW scandal is not to be ignored.

German businesses seem to have relatively bright sense of the functioning of the German economy even if consumers are more wary. Of course, the manufacturing sector is being left behind. And it is an extremely important sector in the German economy. In Europe, Mario Draghi said today he is watching to see if any further stimulus is needed. We are seeing evidence of spreading weakness abroad as Taiwan cut its interest rates today for the first time since February 2009. Brazil's consumer confidence is continuing to make new historic lows in its index. The global economy is struggling and Germany is an export-oriented economy.

Generally when growth is picking up, the business expectations index is moving up faster than the other components. When that index does not do that, the economy tends to slide into a period of weaker growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief