Global| Aug 26 2019

Global| Aug 26 2019German IFO Is Weakest Since 2012

Summary

The IFO climate gauge weakened in August, dropping to -1.4 points in diffusion terms (up responses minus down responses) after logging a net 1.2 point diffusion score in July. Since January 2015, this is the lowest reading. But on a [...]

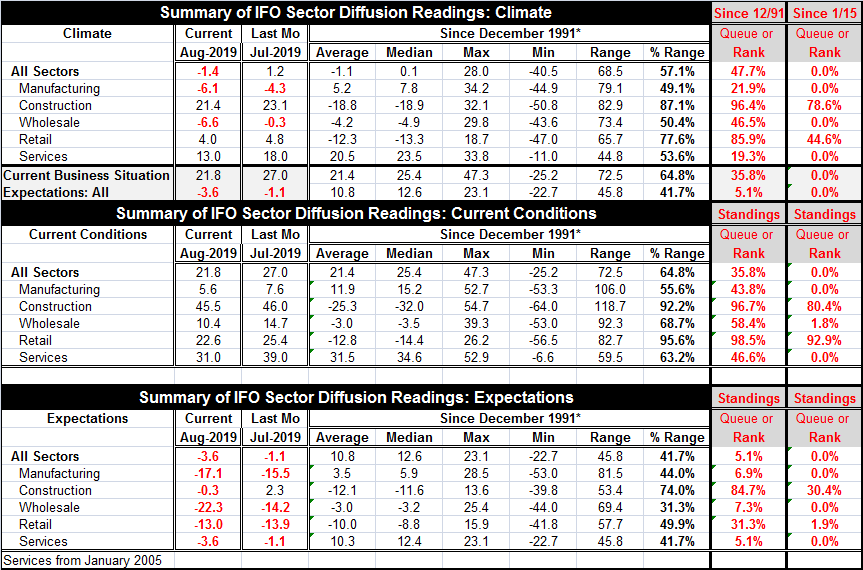

The IFO climate gauge weakened in August, dropping to -1.4 points in diffusion terms (up responses minus down responses) after logging a net 1.2 point diffusion score in July. Since January 2015, this is the lowest reading. But on a broader comparison back to 1991, the overall reading earns a rank of 47.7% which is ‘better' but still sits slightly below its median (the median occurs at a rank of 50%).

The IFO climate gauge weakened in August, dropping to -1.4 points in diffusion terms (up responses minus down responses) after logging a net 1.2 point diffusion score in July. Since January 2015, this is the lowest reading. But on a broader comparison back to 1991, the overall reading earns a rank of 47.7% which is ‘better' but still sits slightly below its median (the median occurs at a rank of 50%).

Manufacturing logs negative readings in each of the last two months. It also is on its weakest reading since January 2015 and has a weak 21st percentile standing even on a broader view comparing this month's reading to data back to 1991.

Construction continues to be a bright spot with a diffusion reading of 21.4 in August although that is slippage from 23.1 in July. The sector has a 78th percentile standing on data since January 2015 and a very strong 96th percentile standing when viewed over data since 1991.

Wholesaling fell sharply in August. Its -6.6 net reading is substantially weaker than July's -0.3 net reading. Wholesaling has deteriorated sharply in just one month's time. This is now the weakest wholesaling reading since January 2015 and it is also a slightly below median reading on a broader comparison back to 1991 (46.5%).

The climate reading for services fell to a +13 reading in August from +18 in July, a sizeable five-diffusion-point one-month drop. Out of the last 176 monthly changes in the services sector, this month's drop has been larger only six other times. It is a sharp one-month drop for services in August. And while there has been weakness in manufacturing for some time, the evidence is now that the services sector is having a hard time holding its own in the face of goods sector weakness. The net services reading of +13 is its weakest since January 2015 and it has a 19th percentile standing since January 2005 when the series begins.

Current situation

The current business situation fell to 21.8 in August from 27.0 in July, another sharp monthly fall. That drop left the current reading at its low water mark since January 2015. And it is at a weak 35.8 percentile standing viewed more broadly over data since late-1991. On both of these rankings, the current reading is weak.

Expectations

Expectations declined again to -3.6 in August from a net position of -1.1 in July. Expectations now have negative readings for two months in a row. The standing is at its lowest since January 2015 and nearly the same at a 5.1 percentile standing when ranked more broadly on data back to 1991. Clearly, expectations are weak any way you slice them.

Detail by sector

The detailed sector data arrayed for current conditions and expectation show a consistently weak picture for expectations with only the construction sector as an exception on the expectations front. Current conditions show a lot more variation both within and between the two ranking periods. There is weakness over the shorter period except for quite strong readings for retail and construction. Over the longer period, the current reading comparisons show subnormal readings in manufacturing and services with a moderately firm reading in wholesaling and strong readings from construction and retail. But there is enough weakness overall to drag the overall current reading down well below its median even when scored against a longer stream of data back to 1991.

On balance, the IFO is a disturbing report. It is disturbing for the way the services sector is following manufacturing lower. It is disturbing because expectations on any period show a depth and breadth of weakness. In 2016, when the U.S. economy slowed and German manufacturing also slowed, the German services sector was unfazed and pressed ahead. The services sector's demise right now is a bit delayed when compared to its reaction in the 2018 recession, but after holding firm services are now unraveling apace. There are good reasons to be concerned about growth in Europe and in Germany; the cracks are spreading and as we all know: crack kills…

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief